A rare inside look at family-controlled global construction giant Bechtel.

Fourteen stories below Saudi Arabia’s Capital, Riyadh, a 1,000-ton monster is carving a hole. The tunnel-boring machine, or TBM, is longer than a Boeing 747 and weighs five times as much. It grinds through the Arabian Desert sandstone 24/7, chewing through the pink-hued rock with its tungsten blades to sculpt a circle 33.6 feet in diameter. The massive device has been given the name Mneefah, for the legendary stallion that carried the kingdom’s first ruler to victory.

This modern Mneefah, however, grinds along rather than gallops. On a recent visit, the tunnel behind the machine’s cutting head is bathed in an eerie fluorescent light. Suddenly, in a cycle that repeats every hour, the blades stop whirring, and a robotic arm swoops down and uses its powerful suction shoe to slowly pick up eight curved six-ton concrete panels one at a time and place them on the newly carved wall in a clockwise pattern. Piece by piece, Mneefah is helping lay the backbone for the largest urban mass transit system ever built from scratch.

[fortune-brightcove videoid=4897960282001 autostart=true]

The Riyadh Metro is just the kind of epic, technically mind-boggling undertaking that makes its lead contractor, Bechtel, perhaps the world’s leading builder of one-of-a-kind megaprojects. A Bechtel-led team is installing 39 miles of tunnels, viaducts, deep-underground stations, and soaring terminals, all in the heart of a city that has never seen a bit of commuter track. (Other contractors are building additional metro lines, but Bechtel is doing the most difficult work in Riyadh’s center and using four of the seven TBMs assigned to the project.)

At $10.1 billion, the Riyadh job is the biggest lump-sum civil engineering project ever awarded to a single team, and it’s being done for a fixed price. The consortium headed by Bechtel—its partners are contractors CCC of Greece and Almabani of Saudi Arabia, as well as Siemens of Germany, which is supplying the trains—is shouldering all the financial risk. Bechtel has guaranteed that by October 2018, the colossal jumble of parts will be united into a seamless network, with futuristic, self-driving trains running end to end.

“For size and complexity, this is the biggest civil engineering job we’ve ever done,” says Amjad Bangash, the Bechtel SVP who’s overseeing the project.

That’s no small claim. Over its 118-year history, Bechtel has arguably changed the face of the physical world more than any other company, anywhere. Here’s a short list of its signature projects: the Hoover Dam (completed in 1936), the Trans-Arabian Pipeline (1950), the Bay Area Rapid Transit system (1976), NASA’s Space Launch Complex 40 (1992), the Channel Tunnel (1994), and the Athens Metro (2004), not to mention Jubail in Saudi Arabia, where Bechtel has been overseeing the construction of one of the world’s largest industrial cities for over 40 years. It recently completed the Hamad International Airport in Qatar, which is built to eventually handle more than 50 million passengers a year (matching the traffic at New York’s J.F.K.). And with BrightSource Energy, it constructed the Ivanpah solar electric complex, a landscape of 350,000 heat-generating mirrors in California’s Mojave Desert that’s the largest solar-thermal plant on the planet.

Bechtel is currently overseeing a major portion of Crossrail, the largest infrastructure installation in Europe—a network of tunnels and rail links in London that will connect the city to the outer suburbs. And the company has developed the first liquefied natural gas (LNG) export terminal in the continental United States.

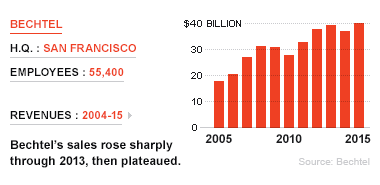

The parade of projects has made Bechtel one of the half-dozen largest privately held companies in the U.S., with $40 billion in 2015 revenue, outranking the likes of chocolate giant Mars and grocery chain Publix. Because of both its size and the crucial nature of the infrastructure it builds, this year Bechtel ranks No. 7 on Fortune’s inaugural list of the 25 Most Important Private Companies.

Bechtel is also the quintessential family business: It has been led, with a brief exception, by a succession of four family CEOs since cattle farmer Warren Bechtel founded the firm in 1898 to help build railroad lines. It has defied the maxim that family businesses inevitably decline after a couple of generations or thrive only by switching to professional management. Perhaps no major U.S. business has succeeded as brilliantly under dynastic leadership for as long as Bechtel (pronounced BECK-tel).

Now a new generation is poised to take charge—at an absolutely pivotal moment, when the global construction industry is undergoing sudden, wrenching change. By the start of 2018, and probably sooner, Warren Bechtel’s great-great-grandson Brendan Bechtel is expected to ascend from president to CEO.

At 35, he is facing challenges that would test the most seasoned veteran. The global collapse in commodities prices has forced oil and mining companies to cancel plans for aluminum smelters, copper mines, and new LNG projects. Oil-rich states in the Middle East that had planned gigantic new transit systems are putting projects on hold. Oman, for example, just delayed a multibillion-dollar rail project. At the same time, Chinese contractors that operate on an entirely new model—exporting thousands of their own low-cost workers to foreign job sites, for example—are starting to compete in the markets where Bechtel is strongest.

In conversations with Fortune—the first major interviews any Bechtel top executive has granted in over three decades—Brendan Bechtel argued that his company will fare far better in this tough market than its rivals, largely because of what he sees as its big advantages as a private, family-led enterprise. “We don’t have to please Wall Street by increasing sales every quarter,” he says confidently. “Our competitors are already taking on risky jobs where they’ll lose money, just to generate sales. Unlike them, we won’t lose dumb.” His company, he asserts, will stay patient and plan long term.

And he is embarking on one of Bechtel’s biggest renovation projects ever: a transformation of the company’s tarnished public image.

Bechtel has long been a magnet for controversy. Its reputation took a beating for the company’s role as a chief consultant on Boston’s infamous Central Artery project, better known as the Big Dig. When the Big Dig finally reached completion in 2007, it was more than a decade behind schedule and, adjusted for inflation, $8 billion over budget. To resolve lawsuits filed by the city, Bechtel and its joint venture partner paid a settlement of $458 million. Since 2000, Bechtel has been building a plant in Hanford, Wash., to treat radioactive waste from the Manhattan Project and the Cold War. The company has drawn heat from environmental groups claiming Bechtel’s processes are unsafe and from officials blasting it for big cost overruns. Bechtel says the plant is safe and attributes the delays and extra spending to numerous design changes mandated by the government to tighten safety standards.

Most biting of all, critics have branded Bechtel as the archetype for a big business that feeds from government contracts—about half its sales flow from state-sponsored projects—and cultivates cozy ties with officials to gain an unfair edge.

That view of Bechtel was given new currency this year by the publication in March of The Profiteers, a Bechtel exposé by veteran investigative reporter Sally Denton. The book bashes the contractor for operating a revolving door for powerful government officials, hiring them for millions of dollars a year, then allegedly exploiting the connections to win business when they return to the highest echelons of government. She claims that George Shultz and Caspar Weinberger, who held top jobs at Bechtel in the 1970s and 1980s, promoted policies that aided their alma mater when they served as secretary of state and defense, respectively, in Ronald Reagan’s administration. According to Denton, Bechtel’s “wielding of unelected power is a cautionary tale of Wild West capitalism,” and the company is led by “a politically reactionary and authoritarian family” that “navigated if not designed the profitable symbiosis between government and industry.”

For decades, Bechtel hasn’t responded to such attacks. It’s been one of the world’s most secretive major enterprises, divulging little about its finances. But late last year, the Bechtel family and top managers decided to tell their story to Fortune by granting extensive interviews for an in-depth corporate profile—the first time the company has ever lifted the veil.

Why is Bechtel breaking its long silence now? One major reason, acknowledges Brendan Bechtel, is the war for talent. In an increasingly competitive environment, the company needs to be able to attract the best engineers and managers to thrive. Today those elite recruits demand to understand the values of the companies that are wooing them. “Ours is a people business that depends on fielding the most capable project teams in the world,” he says. Like many other major private companies, Bechtel’s leaders feels they can no longer afford to hide behind its closely held status and let others control the narrative about its business.

—Brendan Bechtel, President, 35, Great-great-grandson of founder

In that new spirit of openness, Bechtel unveiled its strategy and inner workings to Fortune as never before. The result is a rare inside look at the intense but highly lucrative partnership culture that drives the company.

It’s hardly a surprise that a Bechtel family member is moving back into the chief executive job. But the Brendan Bechtel era at the company is beginning earlier than expected because of unforeseen circumstances. In late 2013 his father, Riley Bechtel, who had served for 24 years as CEO, retired four years early at 61 after being diagnosed with Parkinson’s disease. Since then, Bill Dudley, a 35-year veteran of Bechtel, has been CEO. Dudley, 64, is scheduled to retire no later than the end of 2017 and could step down sooner.

During two long conversations at Bechtel’s San Francisco headquarters, Brendan Bechtel addressed his apprenticeship under the supervision of independent directors and his strategy for navigating the most treacherous market in over a decade. Attired in a blue blazer and open-collared shirt, blond and stocky, he comes across as an earnest listener and conservative strategist. “Over the past few years, the value proposition has been time to market,” he says. “Customers wanted to get their projects finished quickly to benefit from high energy prices. That justified paying more for faster delivery.”

Now, he says, it’s all about price. “The oil and gas companies are slashing their budgets. They want 20% to 25% reductions in the prices they pay for LNG or gas-fired plants,” Bechtel says. “We’re also seeing fewer new-build projects and lots of competitors bidding for them. The competition for each slice of the pie is getting fiercer. We’re preparing for a tough market.”

Private ownership and the patience that it allows, he emphasizes repeatedly, is a major competitive advantage in such an environment.

As for the way the company is described in The Profiteers, he says he doesn’t recognize the Bechtel portrayed in the book. “It’s disappointing when your work is part of the public discourse,” he says. “We do lots of work for the Department of Energy, and all of those projects are competitively bid. We follow the uniform public procurement process. The notion that we can influence that process instead of operating on a level playing field is wrong. I reject the premise of cronyism.”

Interviews with industry experts, analysts, and competitors support that view. At least in today’s fiercely competitive market for global contractors, Bechtel must win on competence, not contacts. It’s all about a company’s ability to deliver a job on schedule and on budget, at the lowest cost. Industry experts generally acknowledge that Bechtel and its smaller, publicly traded U.S. rival Fluor (2015 sales: $18.1 billion) are the best in the business on those criteria. “For the largest, most complicated capital projects in oil, gas, mining, and infrastructure, it’s really Bechtel and Fluor,” says Yuri Lynk, an analyst with Canadian capital markets firm Canaccord Genuity. “They stand head and shoulders above the rest of the industry.”

Brendan Bechtel, the eldest of three children, has been carefully groomed to maintain that reputation. After graduating from Middlebury College with a major in geography in 2003, he spent a couple of years working for the Conservation Fund, a nonprofit that helps fund land and water conservation projects. (His brother, Darren Bechtel, is a venture capitalist in San Francisco, and his sister, Katherine Bechtel, works as a cost and schedule planner for Bechtel.) But Brendan Bechtel decided that the family company was his future and went back to school to get an MBA and a master’s in engineering at Stanford.

In 2010 he embarked on a series of jobs at Bechtel designed to test his mettle as a potential CEO. His career path was orchestrated by the board’s senior management and development committee, or “Smecdec.” Its five members include Riley Bechtel and his father, 91-year-old Steve Bechtel Jr., as well as a group of heavyweight outside directors: David O’Reilly, a former CEO of Chevron (CVX); Nick Moore, a former chairman of PwC; and Leigh Clifford, a former CEO of Anglo-Australian mining giant Rio Tinto. “Both he and the company needed to know if he could succeed at difficult assignments,” says Riley Bechtel. “After four generations of family leadership, we knew that at one point we could be without a family successor, and we were prepared for that.”

Brendan Bechtel’s first major test came in early 2012, when he was dispatched to help oversee the construction of a $10 billion LNG plant on Curtis Island, a remote, rugged outpost off Australia’s northeast coast. For 18 months, Bechtel—who arrived a month after his wedding and lived part-time in a sprawling workers’ camp—kept the gigantic project on time and on budget.

By late 2013 he had reached the next rung: leading Bechtel’s biggest business, oil and gas. Suddenly, his carefully planned career march turned into a sprint. It had been expected that Riley Bechtel would serve as CEO until the end of 2017, the year of his 65th birthday, and that Brendan Bechtel would keep running individual businesses for two or three years before becoming president around 2016. The board followed its succession plan by naming Dudley, then president, to replace Riley Bechtel, who remains chairman. Brendan Bechtel advanced to president and COO in August of 2014.

When he officially takes the reins as CEO, Brendan will be starting with two major advantages in facing today’s rocky markets. The first is Bechtel’s strong owner-

manager structure. The second is the broad array of businesses that cushions Bechtel against big drops in one or two sectors, such as the recent declines in mining and oil. Even with those strengths, the company’s continued success is far from assured. He will be forced to take on riskier projects than Bechtel has delivered in the past few years.

In that sense, Brendan’s campaign to polish Bechtel’s public image is as much about retaining the company’s best talent as it is about recruiting employees. He wants its workforce of 55,400 people to feel pride in their employer. “We’re basically a service business,” he says. “Our people are our assets. Rivals are trying to poach our people more than ever before, and we can’t afford to lose them.”

One time-honored strategy that Bechtel uses to keep its people happy: money. It awards extremely generous bonuses that can reach 50% of salary for mid-level employees. The profits-based part of those bonuses wax and wane not on the performance of the executive’s division but of the overall company’s. “We don’t want people in mining to suffer because of a big downturn and folks in oil and gas to make more because the market is great,” he says.

A full career at Bechtel can bring rich rewards. When a manager is named senior vice president, he or she gains the right to purchase Bechtel shares and becomes a partner. Bechtel doesn’t provide loans to buy stock, so the partners must secure financing from a bank or other sources. All employees must retire at the end of the year after their 65th birthday and, upon leaving, sell their shares back.

The partnership is limited to 50 shareholders—about 35 executives who aren’t on the board; nine executive directors, including Brendan Bechtel; and seven outside directors, including Riley Bechtel and Steve Bechtel Jr. Today the three Bechtels own 40% of the shares, and the managers and outside directors hold 60%. Most of the rules apply uniformly to the Bechtels and their partners. The family-owned shares, for example, carry no special voting rights. But the Bechtel family enjoys one important privilege: While nonfamily partners must sell their shares back on retirement, Bechtel family members may leave their shares to family trusts.

Bechtel declines to disclose its profits, but its CFO, Peter Dawson, says that its return on sales is a low-single-digit number, comparable to a big retailer like Target (TGT) or Safeway (SWY). So let’s do some math. We’ll be conservative and estimate that in a decent year Bechtel earns 2% on its sales of $40 billion, or $800 million after tax (but before bonuses to nonshareholders).

As a service provider, Bechtel doesn’t need to keep a big portion of its profits. “We retain a nominal small percentage of earnings that adds to capital each year,” says Dudley. Let’s assume Bechtel adds 20% of its profits each year to its capital and earmarks an additional 30% to pay bonuses and invest in special projects. In a decent year, it would pay around $400 million in dividends to its shareholders. That amounts to about $5 million—and some years a lot more—for each nonfamily-member partner.

The senior outside directors are partners alongside the Bechtels and act like owners. “We have far more skin in the game than outside directors at public companies,” says former PwC chief Moore. “The fact we’re shareholders comes through loud and clear.”

Bechtel’s business stands on four legs: mining, nuclear and government, oil and gas, and infrastructure. Those businesses run the gamut from tepid to fast growing. Mining spiked from 2009 to 2013, for instance, almost matching oil and gas as Bechtel’s largest division. Since then it’s tanked—along with prices for copper, aluminum, and iron ore. The more consistent government sector helps offset that volatility.

Though its balance provides an essential cushion, Bechtel is nevertheless being battered by stormy markets. From 2004 to 2015, its revenue jumped from $17.4 billion to $40 billion, or about 8% a year—a remarkably rapid pace for the mature construction industry. (Bechtel discloses its annual sales and bookings but not other financials.) Now growth has stalled, and Bechtel’s revenues are essentially stuck at 2013 levels; in 2014, the last year it reported new bookings, it added just $18.4 billion in fresh contracts, short of the $27 billion average since 2004.

A mounting threat to Bechtel and other global builders is coming from the Chinese. Companies like China Communications Construction boomed over the past two decades as they built up China’’s infrastructure. But with growth at home slowing, they’re moving aggressively into new markets. “We used to see the Chinese contractors mainly in Africa,” says Dudley, Bechtel’s CEO. “But they’re trying to become more and more like we are and competing on sophisticated projects in the Middle East.”

Bechtel, meanwhile, is finding growth in some surprising niches. In an era of big deficits and budget-squeezing sequestration, for example, Bechtel has managed to grow its government business by helping weapons facilities save money. And the contracts lock in long-term sales. Bechtel has been building the Hanford plant for the disposal of nuclear waste since 2000, for example, and the first phase isn’t scheduled for completion until 2022.

Then there’s the lucrative business of facilities management. Bechtel is booking $4 billion a year in revenues from a relatively new venture: helping the U.S. government run departments more efficiently. In 2011, Bechtel won a lead contract to manage the nation’s two Navy research facilities for nuclear propulsion. Five years earlier it secured a similar role at the Los Alamos and Lawrence Livermore nuclear weapons and national security labs. At the four facilities, Bechtel oversees about 16,000 employees who run IT, procurement, human relations, and all other management services. The government reimburses all of Bechtel’s costs of about $4 billion and pays a fee of as much as 3%, or a maximum of around $120 million.

Bechtel may be more diversified than ever, but there’s no getting around the fact that wild swings in energy prices and the industry’s changing dynamics are a major challenge for the global builder—particularly when it comes to natural gas.

The company’s largest single business today is building plants that chill natural gas into a dense liquid that’s then loaded on tankers for China, Japan, and Spain. And its LNG contracts account for more than half the revenue of its biggest division: oil and gas.

Bechtel is the construction and engineering contractor on the first LNG export plant built in the U.S. outside Alaska—the Sabine Pass project in the Louisiana mud flats on the Gulf of Mexico. Cheniere Energy’s campaign to build Sabine Pass is the ultimate in roller-coaster rides. In 2005, with natural gas in short supply, Cheniere then-CEO Charif Souki hired Bechtel to erect a gigantic import facility. By the time the plant was complete in 2009, the fracking boom in the U.S. had suddenly created a giant glut of gas that sank the export scheme. “We were effectively bankrupt,” recalls Souki.

In 2013 he sought to rebuild Cheniere by transforming Sabine Pass into an export facility that could supply utilities in Europe. Again he turned to Bechtel.

The facility now encompasses five “factories” or “trains” consisting of seven-story rectangular “cold boxes” and towering pipe racks that stretch the length of three football fields and sit on a 1,000-acre site so wet that it had to be reinforced with pilings and soil mixed with concrete. Each train is essentially a giant refrigerator that cools natural gas to –260° F, creating a stable liquid that’s pumped into the holds of tankers docked at an adjacent port.

Until recently, LNG looked like a great growth market. The five trains in Sabine Pass and a sixth that Cheniere may build represent $11 billion in business for Bechtel. It is getting started on two additional trains for Cheniere in Corpus Christi. In December, Souki told Fortune that Cheniere planned a fleet of 13 to 15 trains across both locations at a total cost of about $25 billion.

Cheniere began exporting in late February, but the market is turning downward for LNG infrastructure, thanks to a capacity surplus and stubbornly low prices. And now Bechtel’s most expansionist, optimistic customer is no longer running Cheniere. In January, activist Carl Icahn forced Souki’s departure. Icahn has signaled that Cheniere should substantially shrink its plans for expansion.

So while Bechtel will keep booking big LNG revenues for a couple of years, it’s unlikely to secure any more gigantic new contracts. Brendan Bechtel acknowledges that a hiatus is at hand. “We won’t be adding more LNG plants at $4 billion a pop,” he says.

That doesn’t mean that Bechtel is backing away from energy. He sees a promising future in smaller LNG facilities that require more modest investment and don’t require buyers to sign big, risky contracts to purchase their output. Meanwhile, Bechtel is doing a brisk business in the U.S. building the gas-fired power plants that are rapidly replacing costly coal-burning dinosaurs.

Over the decades, Bechtel has had no better customer than Saudi Arabia. The construction giant built the Trans-Arabian Pipeline for the Saudis in the 1940s, and it has been supervising additions to the giant petrochemical complex of Jubail since 1976. The Riyadh Metro project was supposed to provide a template for a new generation of transit infrastructure across the Middle East, and potentially many billions of dollars in future business for Bechtel. But that building boom is largely on hold until oil prices rise again.

According to both Bechtel and its client, the Riyadh Development Authority, the metro isn’t endangered by looming budget cuts in the kingdom. “We’ve been asked to maintain the same pace, and that means funding must continue at the same pace,” says Bangash, the project manager. Among the challenges are surmounting delays from rerouting utility lines and creating special designs to overcome the desert conditions, specifically, the clouds of sand that can overwhelm the site without warning.

Down in the tunnel, meanwhile, the Mneefah continues to methodically chew its way through the sandstone, doing its part to keep the project on schedule for completion and testing in late 2018.

When the first train is ready to glide down the rails, it’s likely that Riley and Brendan Bechtel will join Saudi royalty at the opening ceremonies. Two dynasties, in business together for more than 70 years, will exchange congratulations on their latest triumph. The fifth generation of Bechtels is taking charge at a challenging time, when the next such coup may be far over the desert horizon.

A version of this article appears in the June 1, 2016 issue of Fortune with the headline “The Master of Megaprojects.”