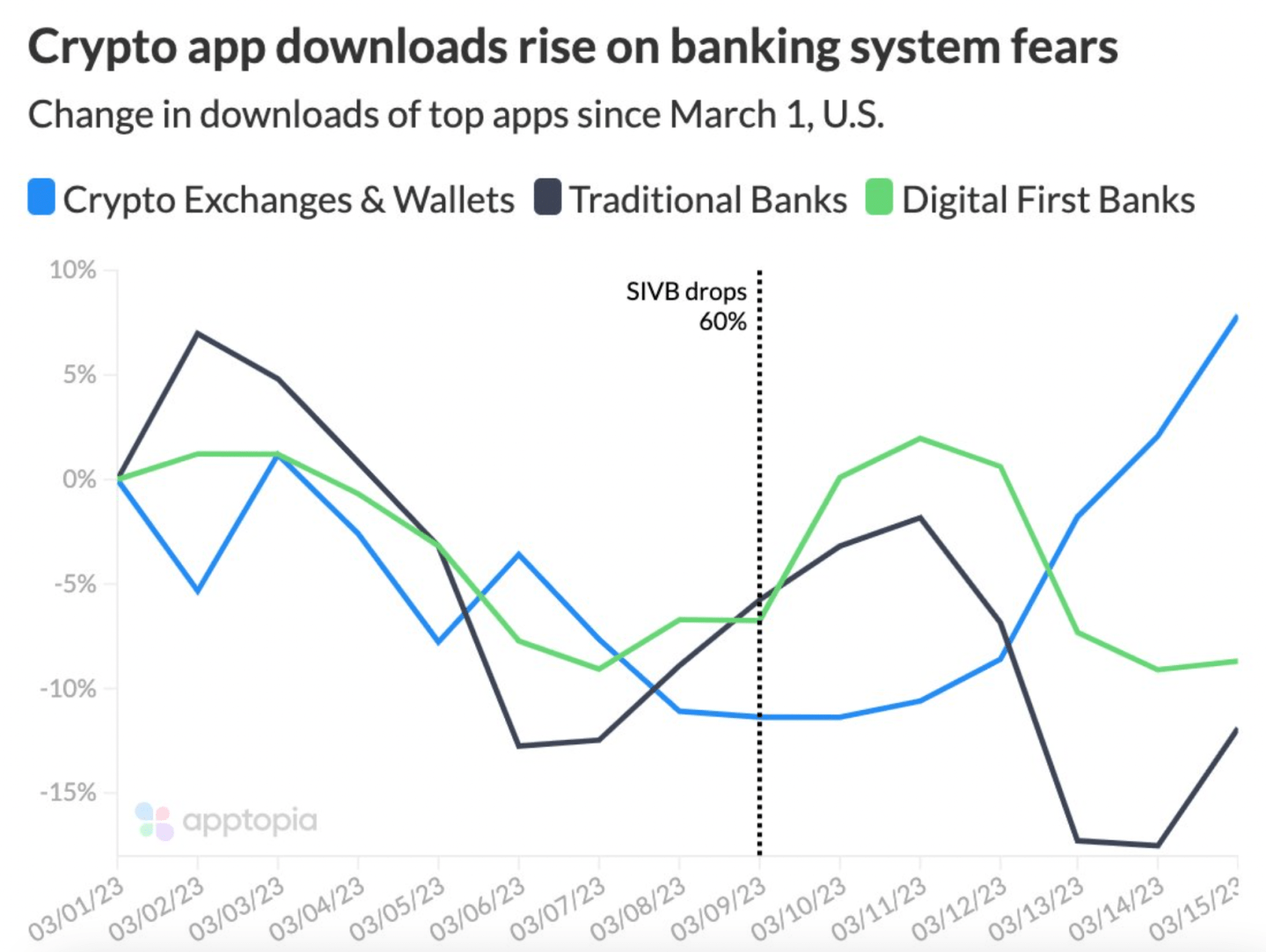

The collapse this month of Silicon Valley Bank and other banks catering to crypto clients felt like yet another instance of bad news for a crypto industry that’s seen more than its fair share in the last six months. But the banking crisis has come with a silver lining: According to data from Apptopia, downloads of crypto apps have jumped more than 15% while those of banking apps have fallen around 5% during the same time.

This suggests a decline of confidence in the banking sector, especially among younger people who are more likely to use financial apps in the first place. This may give you pause about the health of the financial sector (or perhaps about the health of the world in general), but it is certainly good news for crypto companies that have been seeing months of waning interest in their services.

Meanwhile, the spike in app downloads has coincided with a surge in overall crypto prices. Bitcoin is currently trading over $28,000, which is up around 7% in the last week and nearly double where it was trading at the start of the year. Most other cryptocurrencies have experienced double-digit surges as well. This will deliver a welcome boost in trading revenue for the likes of pure crypto companies like Coinbase and Binance, but also for Robinhood, PayPal, and a growing list of other traditional firms that now offer crypto trading.

If you’re unfamiliar, the economics of crypto platforms is pretty simple: Firms take a cut of each trade, either as a commission or through the buy-sell spread, and so higher prices mean higher profits. There’s more money to be made brokering a trade when Bitcoin is at $28,000 than when it’s at $16,000.

All of this is still a far cry from the giddy days of 2021 when Bitcoin was pushing $60,000 and everyone and their dog was vying to get into crypto. But these recent developments will deliver a nice fillip to quarterly earnings, and provide some breathing room to crypto companies as they try to figure out an economic path forward. Given the events of the last six months, they will be happy to take that.

Jeff John Roberts

jeff.roberts@fortune.com

@jeffjohnroberts

DECENTRALIZED NEWS

WorldCoin, the well-funded hardware project that encourages people to scan their irises in return for crypto, is making the case that it can prove "humanness" while preserving privacy. (Fortune)

FTX bankruptcy managers are suing the company's Bahamas affiliate in a bid to quell attempts to transfer company assets to the island nation. (WSJ)

A crypto company goes before the Supreme Court for the first time on Tuesday as Coinbase seeks to overturn a California ruling that rejected its forced arbitration policies. (SCOTUSblog)

Hong Kong's bid to position itself as a hub for the digital asset industry has led to interest from more than 80 companies and institutions. (Bloomberg)

GOP presidential hopeful and Florida Gov. Ron DeSantis proposed a law banning CBDCs though it's unlikely the state has constitutional authority to do so. (Coindesk)

MEME O’ THE MOMENT

This is the web version of Fortune Crypto, a daily newsletter. Sign up here to get it delivered free to your inbox.