The good news: The Federal Reserve has the instruments necessary to rein in runaway inflation. The bad news: Those instruments are, well, blunt, and will hit some sectors harder than others. Among the most vulnerable: the U.S. housing market.

Just look at history. The inflationary period that took off during the ’70s was quelled by the Federal Reserve. But that was only after the central bank pushed interest rates so high that mortgage rates topped out at over 18% by 1981. That saw home construction cut in half by 1982.

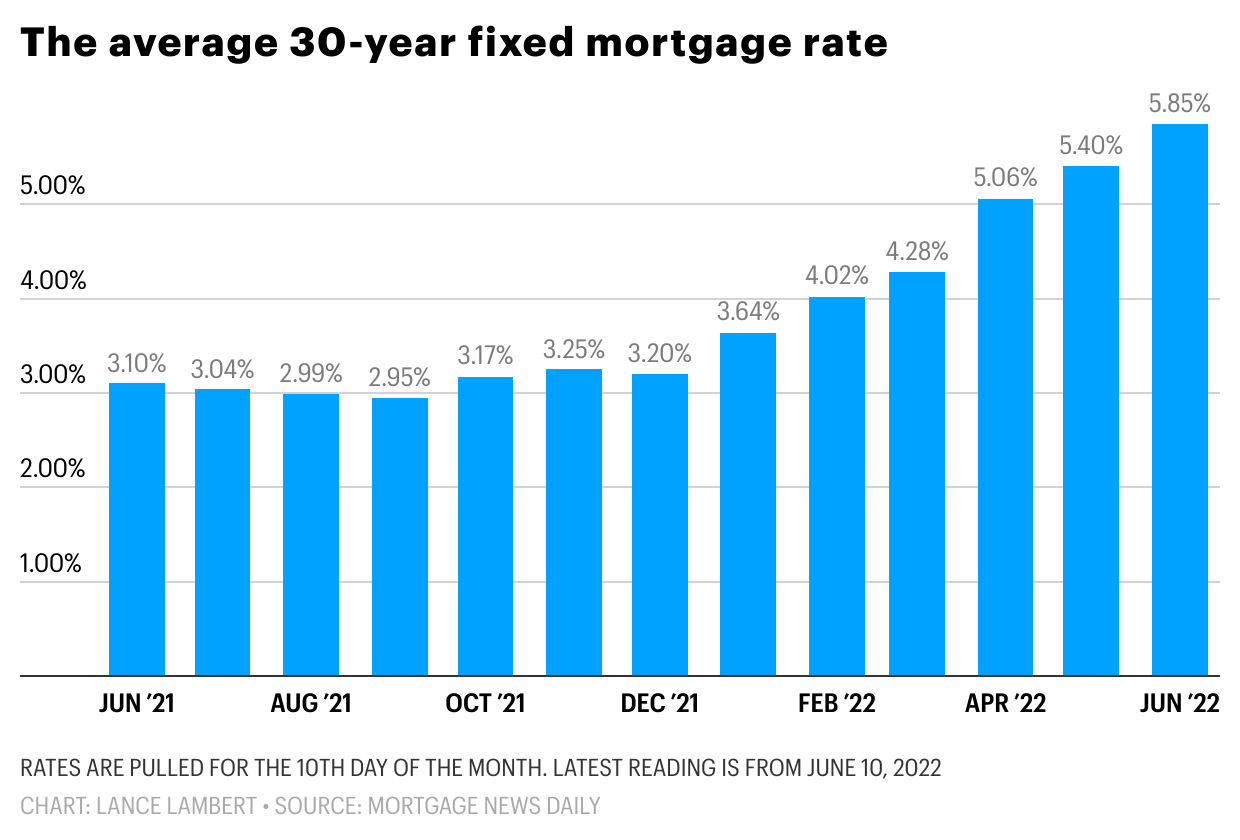

Fast forward to 2022, and the Fed has once again shifted into inflation-fighting mode. Right away, financial markets began pushing mortgage rates higher. Indeed, between December and April, the average 30-year fixed mortgage rate rose from 3.2% to 5.1%.

However, over the past month that mortgage rate spike appeared to level off. It actually fell for a three-week period in May. Well, that was until Friday, when it began to accelerate again. The higher than expected Consumer Price Index reading, which hit a 40-year high of 8.6%, put financial markets in a jitter. By the end of the day on Friday, the average 30-year fixed mortgage rate was sitting at 5.85%.

“I don’t think we’ve seen the end of the rise in Treasury yields,” says Mark Zandi, chief economist at Moody’s Analytics. Historically speaking, mortgage rates follow the trajectory of the 10-year Treasury yield. If the 10-year does indeed go higher, Zandi tells Fortune that we could see mortgage rates top 6%.

A 2.75-percentage-point spike in mortgage rates over the past year—with most of it coming over the past six months—is historically rare. You’d have to go back to 1981 to find the last time mortgage rates moved up that fast.

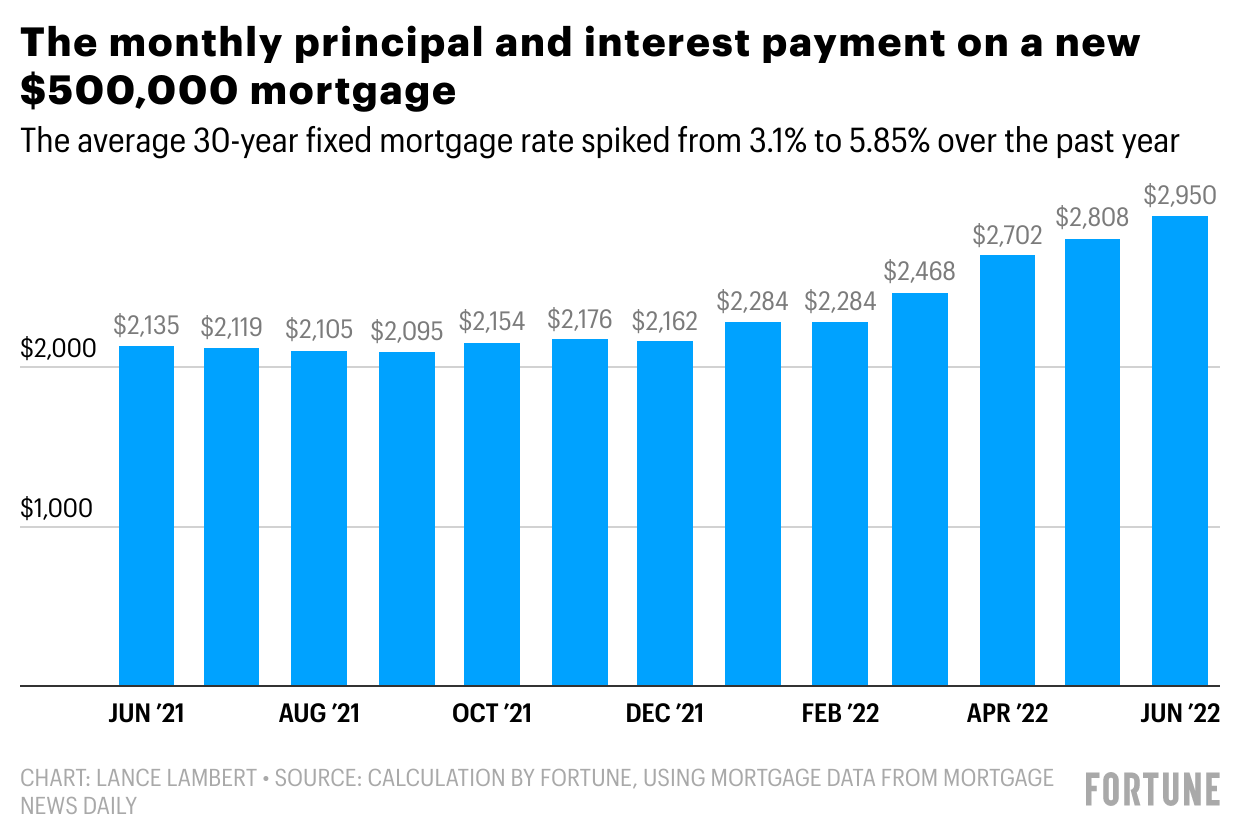

The swift jump in mortgage rates was both an economic shock to the housing market and a huge blow to home shoppers. If a borrower in June 2021 took out a $500,000 mortgage at a 3.1% fixed rate, they’d see a monthly principal and interest payment of $2,135. At a 5.85% rate, that monthly payment would be $2,950. That’s a 38% higher monthly payment. Over the course of the 30-year loan, it’s an additional $293,264 in total payments.

That’s also a bad example. Why? Over the past year, home prices have spiked a record 20.6%. Simply put: A borrower couldn’t get the same home for $500,000 now as they could a year ago. For that reason, let’s say that $500,000 mortgage climbed 20.6% to $603,000. At a 5.85% fixed rate, the monthly principal and interest payment on a $603,000 loan comes out to $3,557.

The swift move up in mortgage rates coupled with the historic jump in U.S. home prices—which have shot up 36.8% since the onset of the pandemic—is why the U.S. housing market is slowing. Many borrowers, who must meet lenders’ strict debt-to-income ratios, have lost their mortgage eligibility or simply refuse to shell out that much dough. Regardless, it has the U.S. housing market in what Zandi calls a “housing correction.”

Already, we’re seeing both existing home sales and new home sales fall—fast. On Thursday, Freddie Mac deputy chief economist Len Kiefer tweeted that the downward shift in mortgage applications means “the U.S. housing market is at the beginning stages of the most significant contraction in activity since 2006.”

We're also seeing the cooldown bring up inventory levels.

As the housing boom took off during the pandemic, inventory plummeted to four-decade lows. This March, nationwide inventory levels on Zillow were 64% below March 2019 levels. But as the housing market begins to shift into cool-down mode, inventory is rising again. Between March 26 and May 7, nationwide inventory levels rose 10%. That included an inventory increase of 54% in Coeur d’Alene, Ida., and 49.6% in Reno.

"The best part of the housing story in 2022 is the rise of inventory as this will put home sellers and builders in check. They had too much pricing power and they pushed prices way too high," says Logan Mohtashami, lead analyst at HousingWire.

Even as the housing market cools, Mohtashami says, there's still too little inventory on the market. Indeed, the vast majority of regional housing markets (see chart below) still have inventory levels that are more than 50% below their pre-pandemic level. If mortgage rates start to fall again, he says, the tight levels of inventory could see the frenzy come back.

Is it possible the housing market could shake off this slowdown and kick back into boom mode? Zandi doesn't think so. This housing cooldown is by design—the thinking of the Fed being if it can slow the housing boom, it can slow inflation. On that front, Zandi says the Fed is likely happy with the housing cooling that began in April.

Heading forward, Zandi expects national year-over-year home price growth to flatline to 0%, and significantly "overvalued" housing markets to see 5% to 10% home price dips. Of course, even a 5% to 10% price dip is hardly financial relief for homebuyers—at least not if mortgage rates do indeed jump over 6%.

If you’re hungry for more housing data, follow me on Twitter at @NewsLambert.

Sign up for the Fortune Features email list so you don’t miss our biggest features, exclusive interviews, and investigations.