For all the ongoing tumult of the pandemic and its aftermath, the stock market once again had a banner year in 2021. By August, the S&P 500 had doubled from its pandemic low in March 2020; since then, it has continued a protracted climb to record high after record high.

The year ahead, however, is likely to be less sunny for stock investors. “There are really three key issues to think about for 2022,” says Saira Malik, head of global equities at Nuveen, “and those are growth, inflation, and ‘What’s the Fed going to do?’ ”

Inflation is arguably the biggest threat to share prices of the three—but the others could also weigh on the market. The Federal Reserve’s low-rate policies, which have been a boon to stock investors since COVID struck, are turning more contractionary—with the Fed beginning to taper bond purchases and eyeing rate hikes as soon as next year. Earnings growth, meanwhile, has been remarkably high in 2021—factoring in a comparison to a pandemic-racked 2020—with S&P 500 earnings per share up nearly 40% year over year in the third quarter, according to FactSet, as companies rebound from lockdowns. But Malik sees earnings growth decelerating to, at best, high-single-digit rates in 2022, the kind of slowdown that can make investors skittish.

“Not every business model is built to handle those kinds of challenges,” says Eric Schoenstein, a managing director and portfolio manager at Jensen Investment Management. The bottom line: Investors will need to be more picky when positioning their portfolios for 2022, looking for companies that have more resiliency.

With that in mind, Fortune asked portfolio managers which companies could keep growing their earnings and satisfying their shareholders even if the wild bull market grows tamer. They all had price increases on their minds, but they weren’t all buying companies that directly benefit from inflation and rising rates. (For more about that strategy, see “Inflation could end tech stocks’ winning streak in 2022—and pump up these stocks instead.”)

Instead, many of our experts’ picks had one key ingredient in common: pricing power. Those companies who have it will be likely winners if inflation remains higher than it was in the pre-pandemic era. And all 11 stocks to follow have the kinds of advantages that could provide investors with a security blanket if markets grow chillier.

Growing strong

High-priced growth stocks have largely led the recent charge in stocks. As we discuss elsewhere in this package, some analysts think pricey valuations today will eventually mean meager returns for Big Tech stocks. But portfolio managers expect these tech names to keep delivering steady growth.

The virtues of Amazon for investors are many, from its core e-commerce business to its powerhouse web services unit. It’s “a business that continues to get better as it gets bigger,” says Matt Benkendorf, chief investment officer of asset manager Vontobel’s Quality Growth Boutique. Though Amazon recently warned of labor, wage, and supply-chain issues impacting its business, he notes that it’s “a giant of scale versus competitors, and in a higher inflationary environment that scale will be a benefit to them if it’s causing others to hurt.” Even if consumers shift their purchasing behavior in search of less expensive goods, Amazon “fortunately sells a whole lot of everything,” he adds. Benkendorf also points to how Amazon has been investing in distribution and logistics capabilities, all while its e-commerce business has been booming during the pandemic. “You’re going to start to see them bear the fruits of that massive investment.” The Street expects Amazon to grow revenues by nearly 18% next year, though the stock, at a price-to-forward-earnings ratio of 92, is not cheap.

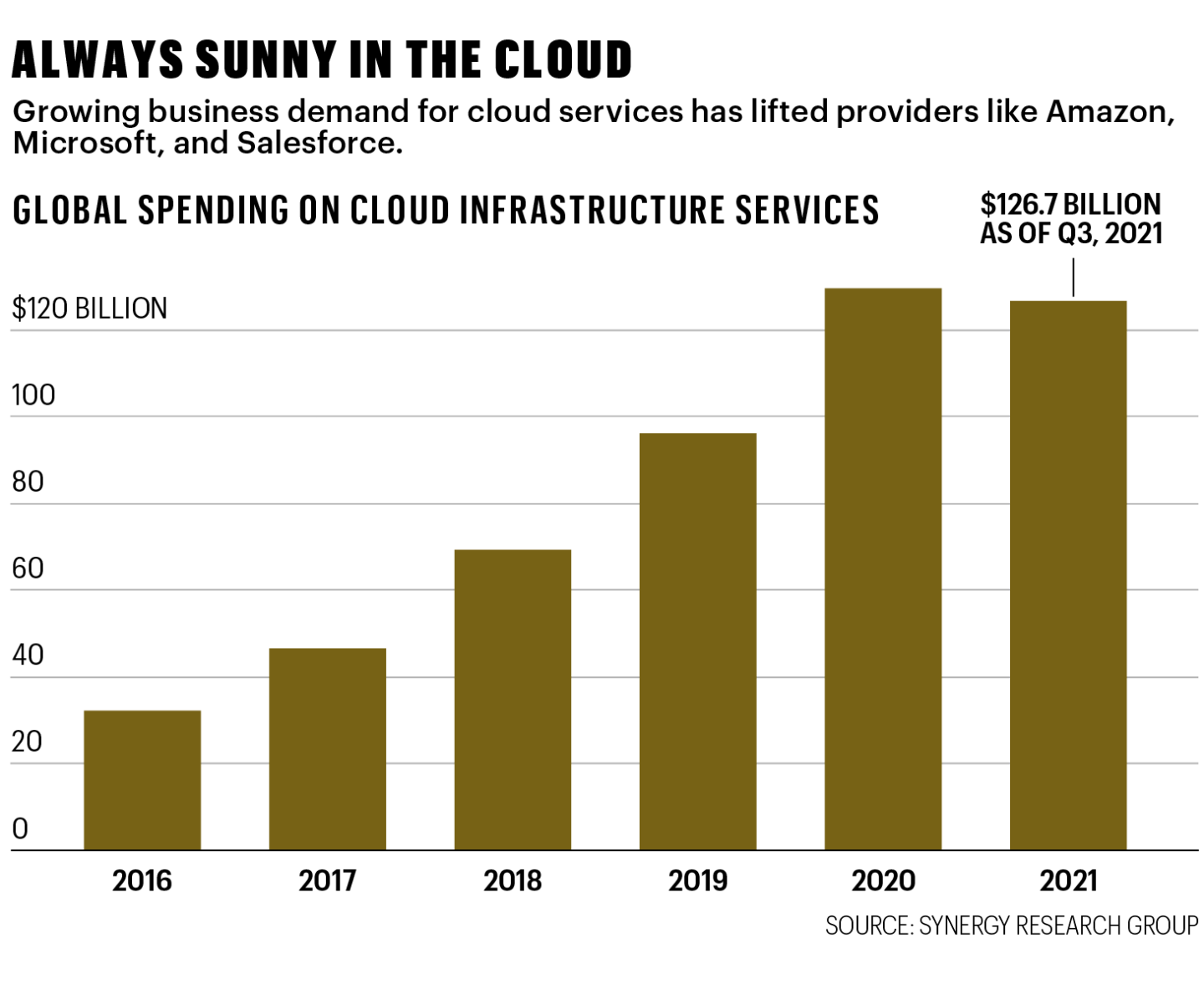

Some tech companies that saw a big spike in demand during the pandemic could face a steep drop next year. Jensen’s Schoenstein thinks that’s unlikely for steady-growing Microsoft. Microsoft’s cloud business is a particular bright spot, he notes, booking a 31% increase in revenues in the most recent quarter, while the high costs of switching away from the company’s cloud and Windows platforms should give Microsoft prized pricing power. Schoenstein highlights Microsoft’s free cash flow, which should fund investments that fuel future growth. Despite Microsoft’s membership in the $2 trillion market-cap club, the stock doesn’t trade at nosebleed levels, at roughly 36 times forward earnings, and analysts believe Microsoft can grow revenues by over 16% in its current fiscal year (ending in June 2022).

The end of stimulus checks and the higher cost of goods may prompt some consumers to alter their spending habits, but that’s unlikely to hurt PayPal. Since PayPal earns most of its revenue by collecting a percentage of the value of each transaction, says Benkendorf, “pricing levels going up shouldn’t be bad for them.” He likes PayPal’s migration into financial services, “providing a bunch of other services for these new generations of consumers” who are weaning themselves from brick-and-mortar banks. A recent disappointing revenue forecast sent the stock down; it now trades around 35% off its 52-week high. But Benkendorf believes PayPal’s superapp ambitions and partnerships (like a recently announced Venmo-Amazon tie-up) help to keep it well positioned.

For investors angling to get in on the trend of companies transitioning onto the cloud, Nuveen’s Malik favors Salesforce, the software provider that helps businesses with front-office functions including marketing and customer service. The pandemic, Malik notes, has only accelerated businesses’ reliance on front-office software, and Salesforce is a top player in that space. The firm’s customer contracts have “annual pricing power baked in, which helps in the short term,” she adds. Salesforce stock trades at roughly 77 times forward earnings, but the company is expected to grow revenues by over 20% next year.

Paying dividends

If leaner times do come for the stock market, experts recommend having a few dividend-paying stocks in your back pocket to bolster your portfolio and provide some security. “Dividends don’t seem very sexy,” notes Schoenstein. “And yet if the market’s not going up … guess what? You’re making a 3% or 4% return while everybody else is maybe not making much at all.”

Schoenstein likes food and beverage giant PepsiCo for its 2.6% dividend yield and its breadth of popular products, including snacks like Doritos, Aquafina bottled water, and, of course, sodas. Pepsi recently raised its revenue forecast for the full year of 2021 on the back of higher third-quarter earnings, and Schoenstein believes it has “built an incredible brand” by investing in new products and advertising. Even amid industry- and companywide supply-chain issues, Schoenstein suggests that “because of their market share … they can push through subtle price increases, or they can alter package design or sizes, and frankly, consumers are willing to continue to pay.” Pepsi trades right around the consumer staples sector average, with a reasonable P/E ratio of 25 times the next 12 months’ earnings.

Schoenstein also favors pharma giant Johnson & Johnson. He likes J&J’s sizable 2.6% dividend yield and argues that the stock’s longtime catalysts remain in place. “Health care is a consumer need and something we all are willing to pay for to live healthier lives,” he notes, pointing to the driving factor of an aging population in need of ever more health care. Big changes are coming to the conglomerate: In November, J&J announced that it will be separating its consumer businesses from its pharmaceutical and medical-device businesses. The first category includes brands like pain medication Tylenol, while the second includes J&J’s COVID-19 vaccine and drugs focused on autoimmune diseases. The split is a positive move, according to some money managers. By hiving off the consumer business, J&J “will be able to more directly focus its efforts and investments on higher margin, faster growth opportunities in pharmaceutical research and medical devices,” argues fellow Jensen portfolio manager Allen Bond. (Current J&J shareholders will likely retain shares in both companies.) Trading at roughly 16 times forward earnings, the stock is on the cheaper end (the forward P/E for the S&P 500 is 23), and J&J recently raised its full-year earnings forecast.

Benkendorf likes Comcast with its 1.9% yield, because after more than a year of working and studying from their dining rooms, investors “understand the importance of high-speed broadband at home.” Even in a higher-inflation environment, he adds, “broadband has pricing power.” Comcast trades at around 15 times forward earnings, and Benkendorf believes the stock is “pretty reasonably priced for a nice runway of growth” with “very nice margins.” Comcast is also getting a cyclical boost from its Universal theme parks as the economy continues opening up, Benkendorf notes, even though wage increases are raising its costs at the parks.

Thinking globally

Inflation is a global issue, with supply-chain kinks hampering countries around the world. But Malik thinks “international markets could be more interesting [as] U.S. growth is slowing.” Some flagship companies outside the U.S. are poised to capitalize on current trends regardless of the short-term economic backdrop.

Canada-based Shopify is becoming a formidable player in the global e-commerce space and a winner for investors, with its share price up over 420% since mid-March 2020. Despite the run-up, Gary Robinson, a portfolio manager at asset manager Baillie Gifford’s U.S. Equity Growth Fund, is bullish on Shopify’s long-term story. “The size of Shopify’s business has been completely transformed through the pandemic,” he says. Though Shopify missed Street estimates in its most recent earnings, analysts wager it can continue to grow sales by nearly 34% next year. The company is “starting to become the partner of choice when other platforms are looking to integrate e-commerce,” says Robinson, citing Shopify’s partnerships with heavy hitters like Walmart, Instagram and Facebook shops, and TikTok. As with PayPal, part of Shopify’s revenue comes from fees based on a percentage of the value of goods sold. If inflation keeps ticking up, Robinson argues, “Shopify revenues are going to march up with the rise in prices.” You’ll pay a pretty penny for that growth and inflation protection: The stock trades at over 260 times forward earnings.

The company at the epicenter of the planet’s most seismic surges in demand right now is Taiwan Semiconductor Manufacturing Co. (TSMC, for short), the world’s dominant contract chipmaker. Semiconductors are “basically becoming ubiquitous—they’re used in everything from manufacturing plants, autos, 5G, to artificial intelligence,” notes Malik. And Schoenstein says that TSMC has been at the “forefront of building capacity” so it can play a leading role in resolving the worldwide chip shortage. Demand and capacity make the company a great hedge against inflation. While TSMC has been tight-lipped about whether it’s going to increase what it charges customers, “they have the pricing power,” notes Malik.

When it comes to the consumer staples sector, not every company can ride out a higher inflationary environment. It helps if they not only can pass along price increases to customers, but are “very well run from an efficiency standpoint,” notes Benkendorf. One name that fits the bill is Switzerland-based Nestlé, the titan whose brands include Cheerios, DiGiorno pizza, and Nescafé coffee. Benkendorf commends Nestlé’s chops with R&D and innovation too. The stock trades at 26 times forward earnings (the current consumer staples sector forward P/E is 21).

Inflation is far from the biggest challenge facing Chinese internet and gaming giant Tencent. The regulatory headwinds that have buffeted Chinese tech stocks in general have also hit Tencent—in particular, recent rules that ban minors in China from playing video games during weekdays and limit play on weekends. The majority of Tencent’s revenue comes from gaming, and its stock is down 13% so far this year. But Malik points out that players under 16 years old account for less than 3% of Tencent’s China gross gaming cash (according to the company’s 2021 interim report). Though she expects Tencent’s domestic gaming revenues to remain flat over the next few quarters, she’s “optimistic on overseas gaming growth.” The rest of the company, meanwhile, is seeing healthy expansion in a diverse range of other businesses, online payments, and cloud services—many of them complemented by Tencent’s WeChat communication tool, which is ubiquitous in China. Online advertising is a strong business for the company, although inflation and regulation have slowed its growth this year. Taking all that into consideration, Malik believes Tencent’s valuation—at 27 times forward earnings—is low enough to justify taking a flier on one of China’s most dominant tech companies.

Picks

Amazon (AMZN, $3,696)

Microsoft (MSFT, $341)

PayPal (PYPL, $201)

Salesforce (CRM, $303)

PepsiCo (PEP, $163)

Johnson & Johnson (JNJ, $162)

Comcast (CMCSA, $53)

Shopify (SHOP, $1,681)

Taiwan Semiconductor Manufacturing (TSM, $123)

Nestlé (OTC: NSRGY, $133)

Tencent (OTC: TCEHY, $62)

Prices as of 11/18/21

How Fortune did

In most years, a 15% return—the median performance of our 21 “Stocks for 2021”—would put a smile on investors’ faces. But the S&P 500 returned 31% over the same span, so we’ve got some explaining to do. Here’s a postmortem.—Matt Heimer

Reopening reality

We bet that the rollout of COVID-19 vaccines would boost industries like travel, entertainment, and retail. The lift came, but stock returns didn’t always follow, and the Delta variant impeded many companies’ comebacks. So while concert-and -event giant Live Nation Entertainment was one of our top performers (up 69%), airlines Southwest and JetBlue (up just 4% and 0.5%, respectively) helped to drag us down.

Tech, triumphant

Our biggest mistake was a sin of omission: We didn’t think the Big Tech stocks would repeat their torrid run of 2020. In fact, Microsoft and Alphabet crushed the broader market (and our picks), returning 58% and 67%, respectively. The silver lining: If you owned an S&P 500 index fund, you benefited anyway, since those two stocks alone account for more than 10% of that index’s market cap.

Bank on it

We predicted that banks with a consumer-heavy focus would cash in on a recovery. Our two picks, Wells Fargo (up 103%) and Bank of America (up 72%), paid off with interest, thanks in part to a huge increase in home mortgage issuance.

A version of this article appears in the December 2021/January 2022 issue of Fortune with the headline, “Stocks for smoother sailing.”

This story is part of Fortune's 2022 Investor's Guide.