In 2014, a startup with zero history as a company set out to sell investors on its promise to revolutionize the real estate industry by guzzling cash and going on a buying spree of houses. Unsurprisingly, it struggled in the early days to even get a bank despite its roster of starry investors.

Plenty of established lenders shut the door on Opendoor—except one: Silicon Valley Bank. And it had the last laugh.

In September, Opendoor agreed to go public via a merger with early Facebook executive Chamath Palihapitiya’s Social Capital Hedosophia II, a special purpose acquisition company or SPAC formed for the sole purpose of buying other businesses, at a valuation of about $4.8 billion. In the usual Twitter rounds of investors applauding one another for a successful exit, storied venture investor Keith Rabois, who cofounded Opendoor, gave praise to the company that rarely makes it into the headlines, even if it is ubiquitous as the bank of the startup world: “Silicon Valley Bank also deserves credit for Opendoor,” Rabois wrote in September. “Without their support in the beginning, it would have been nearly impossible to prove we could value homes successfully via a model.”

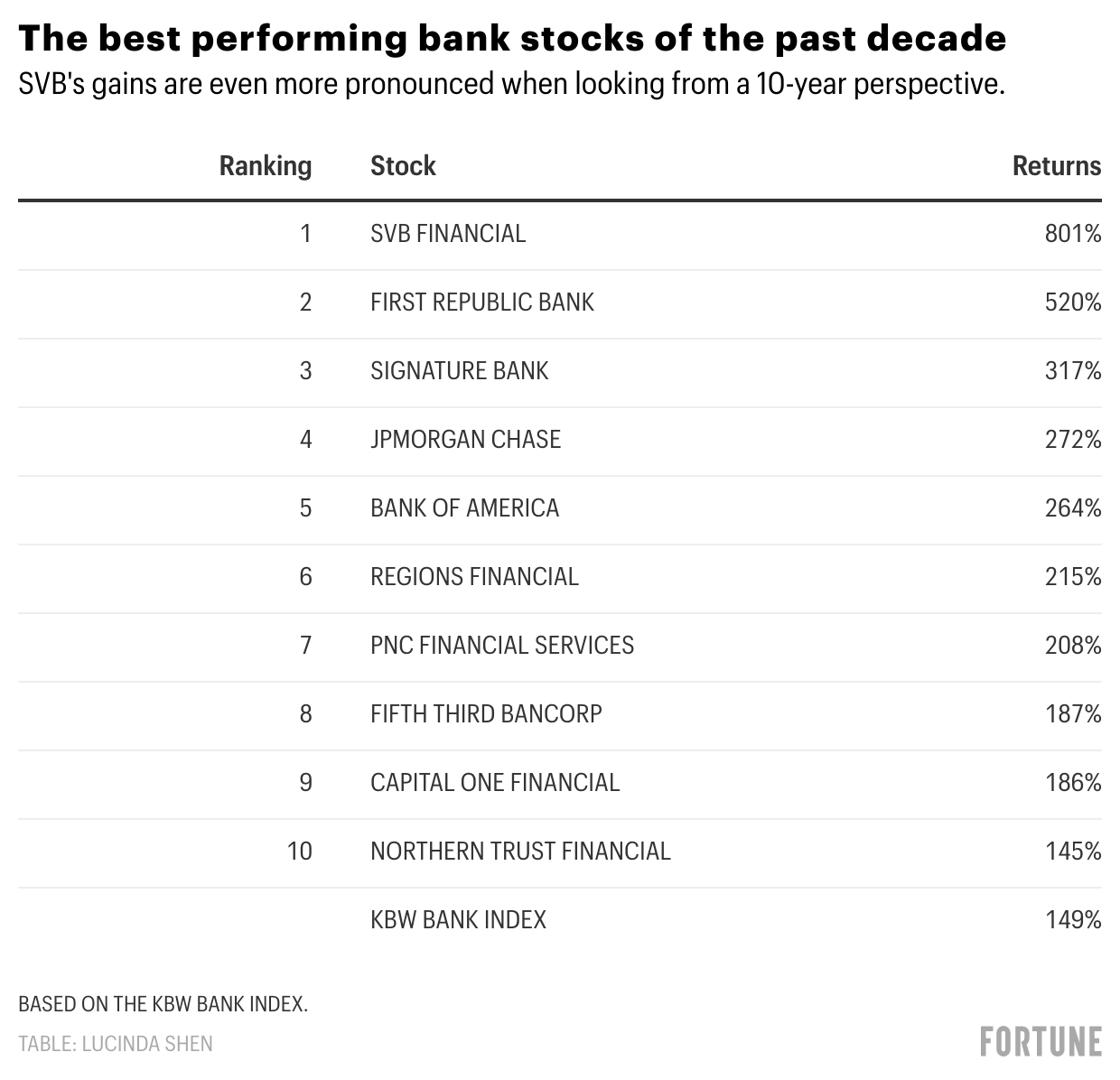

It’s this dynamic, multiplied over, and over, and over again, that has catapulted what was once a small regional bank into the stratosphere. For the average investor, it’s not easy accessing private market companies before they go public. So investors banking on the rise of tech and private markets have looked to the publicly traded Silicon Valley Bank as a proxy, pouring into the company’s stock in the past year. Under ticker symbol SIVB, the bank has emerged as one of the best performing stocks on the S&P 500 in the past year, handily beating all other banks with a 166% gain. So pronounced were its gains that investors who missed out on pandemic winners such as the Zoom and Shopify rallies that began in March 2020 would have been better off pivoting to Silicon Valley Bank by the summer (Zoom rose 51% in that period, while Shopify grew 42%).

“Sure there are going to be tech booms and busts, but Silicon Valley Bank is sitting in the middle like a tollbooth,” says John Loesch, a bank-focused research analyst at Diamond Hill, which has held shares in Silicon Valley Bank since 2016, explaining his bullishness around the stock. “And what would you want to bet on in 10 or 20 years? Human ingenuity.”

Founded in California in 1983 by former Wells Fargo banker Bill Biggerstaff and Stanford professor Robert Medearis, Silicon Valley Bank from the beginning was a bit of a crazy idea: It sought to bank what were then considered unbankable (or at the very least, very hard to bank): startups. Without a long operating history, lending to venture-backed startups was a practice underwriters considered too risky, bordering on idiotic. But even back then, there were early signs of a burgeoning industry on the rise. Companies such as Intel and Fairchild Semiconductor were beginning to gain traction, yet they lacked banks that would work with them. Meanwhile, Apple had gone public about three years earlier, while a change in regulation in 1978 had pension funds pouring into venture capital. Silicon Valley Bank would in 1984 become Cisco’s first bank.

At the center of Silicon Valley

Now Silicon Valley Bank is reaping the rewards of a 38-year-old strategy. In return for servicing businesses that other banks traditionally would have turned away, SVB also at times receives warrants early in a company’s lifetime that gives the bank the right to buy shares. While SVB does not say exactly whom it has banked, recent initial public offering filings from companies going public have revealed SVB as a surprising beneficiary.

SVB for instance serviced Coinbase, starting around 2012 when cryptocurrency was still heavily associated with the dark web, at the urging of well-respected venture capitalist Fred Wilson, per my former colleague Jeff John Roberts’s book, Kings of Crypto. While SVB later broke relations with Coinbase when cofounder Fred Ehrsam made a presentation depicting how countries could use Bitcoin to dodge sanctions, that relationship still gave SVB a stake in Coinbase when it went public in April. SVB for its part says the presentation was not the reason for the relationship’s breakdown, but declined to elaborate further. Regardless, the bank’s holding in Coinbase was worth $115.8 million in the first quarter.

SVB also had similar agreements with e-commerce startup BigCommerce, which debuted last summer to a $4.5 billion valuation; cybersecurity company CrowdStrike; cloud company Snowflake; as well as insurance company Root, which now is trading at about $2.4 billion. While Silicon Valley Bank did not receive warrants in every single startup it banked, SVB estimates that about 68% of companies with IPOs in 2020 had some relationship with the firm at the time of their listing.

In total, despite struggles early in the pandemic with low interest rates (which lowers the amount banks earn from lending), in the 12 months ended March 31, SVB grew revenue by nearly 50% to $4.5 billion and net income by 35% to $1.6 billion, not only because of its warrants, but also because of the bank’s other lines of business that explicitly focus on the venture capital and private equity world. Gains on sales of investments and securities meanwhile grew 250% in the period compared to the same one a year earlier, reaching $987.5 million.

“So much of banking is commoditized; it’s based on how much you’re going to pay for deposits and how much you are going to charge on a loan,” says Loesch. “There are few truly unique franchises that have a distinct competitive advantage like SVB.”

Secret sauce

Even as giants like J.P. Morgan are now banking early-stage startups, analysts note, Silicon Valley Bank became a hard-to-shake institution. Ask a founder, and many will say that SVB has a reputation for understanding startups in ways that few other banks do. After all, it’s an industry where an estimated anywhere between 60 to 90% of companies fail, and countless others face turbulent and hard-to-predict changes in their early lives. Twitter for instance had its start in a podcasting company. SVB meanwhile has been known to be forgiving when it comes to loan terms. In 2018, photo-app company Chatbooks thought it was in danger of breaking its loan covenants. Chief operating officer Dan Jimenez gave the bank a heads-up, and SVB amended the terms to give the company more time to reach Ebitda profitability, he says.

“All banking is relationships,” says Sean Gourley, the CEO of Primer AI, who went to Silicon Valley Bank with his first check, before his company had any revenue. “As a founder you have a network of other founders with whom you trade which HR software, credit cards, or office deals to get. And the one with the strongest polling among your friends that have started companies is who you will bank with.”

The bank understands that this kind of network effect is key: Startup founders who have joined as clients note that the bank has introduced them to potential investors, employees, and customers—even becoming a customer itself of the folks it services, says Visier CEO Ryan Wong. In late June, the Canadian human resources data startup raised $125 million in funding from Goldman Sachs Asset Management. Still, Visier remains a client with SVB. “They made introductions to customers, and I jokingly say [SVB is a] very good software buyer,” Wong says.

But here’s the $30 billion question: How do you lend safely to an industry where an estimated 60% of your customers fail?

The bank is certainly not handing out its services indiscriminately. It knows most of those warrants on startups will be worthless, analysts say. Part of its job then is finding the startups that won’t necessarily win, but will at least make good on their loans. The bank collects the typical interest and fees on loans and services, with the warrants acting like an extra bulwark if they are above water. In some ways, the bank’s underwriting team thinks like a venture capitalist, evaluating a company based on the founding team’s work history (worked at Stripe? You might be a shoo-in!), regulatory environment, the competition, the investors, and growth potential. Startups have been known to be turned away, as Coinbase was, owing to issues including regulatory concerns.

“There are so many different factors. You can’t just look at one thing,” says SVB president and CEO Greg Becker of the underwriting process. “There’s pattern recognition. I’ve been at the bank for 28 years, and this is pretty much my entire career.”

In fact, in many pre-revenue startups, founders who have been through SVB’s underwriting machine described the process as not of one that underwrote the company, but of the exact partner who made an equity investment—with SVB keeping track of the venture capitalists who brought them deals that paid them back and those that did not. David Spreng, CEO of venture-debt–focused Runway Growth Capital, recalls being told he was on the bank’s “good side” when he was the managing partner at Crescendo Ventures. Though a top investor is not always correlated with a good loan, as an SVB spokesperson noted in a follow-up email: “We expect to take losses on a portion of our early-stage loans, including from companies backed by top-performing VCs. Just as not all investments will make a return, not all loans will be repaid in full.”

While Silicon Valley Bank is known for banking tech startups, the secret to its most recent growth is actually even less mainstream. It’s a product known as a capital call line—or lending to private equity firms and venture capital investors. As dealmaking in the private markets hit all-time highs amid low interest rates, the so-called Global Fund Banking group, whose main product is the capital call line, has become SVB’s fastest-growing segment within lending, says CEO Becker.

The reasoning behind the growth of the segment is twofold: First, even if a venture capital firm has on paper a $1 billion fund, it takes time to draw the funding from its own investors—the limited partners—to actually put say $100 million to work in a company. In the fast-moving dealmaking world, that lost time can mean a lost deal. So private market investors may keep a capital call line to deploy investments faster. Second, firms can also use the line of credit to boost their internal rate of return (IRR) by effectively buying on margin or, more problematically, using the line to manipulate the IRR, the all-important benchmark upon which their performance is judged. IRR is calculated in large part based on the timing of the capital call. The later the capital call, the higher the return. By using the credit line, investors can delay the point at which they call for capital from their limited partners.

But with blistering growth in the space, Silicon Valley Bank has also made missteps: A principal at JES Global Capital, a private equity firm in Wellington, Fla., allegedly lied about having investors like hedge fund manager Steven Cohen, and based on that, drew $95 million from a $150 million credit line—$80 million of which has yet to be repaid. SVB sued the principal, but questions over whether the bank did enough due diligence persist.

SVB declined to comment on the issue, saying it does not comment on the details of individual third-party matters or pending litigation.

Banking on tech

Here’s the other thing about startups: Work with them long enough, and they will find some way to disrupt you. There’s an ex-Googler looking to build an ad-free Google; a venture-capital–backed startup looking to fix bottled water. Heck, there are startups disrupting the disruptive venture capital disrupters with new financing models based on subscription revenue.

At 38 years old, Silicon Valley Bank is no exception. Startup founders have labeled its user-facing app lackluster, with one founder throwing down a scathing comparison that is the ultimate denunciation in the tech world: It’s like a government website, says Tandem’s Rajiv Ayyangar (though he adds, government websites “provide a valuable service and are often low on funds!”). Frustrations with SVB’s tech have spawned startups like Mercury, a San Francisco–based banking company with top-tier investor Andreessen Horowitz and even Silicon Valley Bank’s founding CEO Roger Smith on its cap table. Signaling its surging popularity, Mercury is said to have raised funds at a $1.6 billion valuation recently via Coatue Management, The Information reported earlier this month.

And in the hallowed halls of Y Combinator—the much-watched trendsetting “Ivy League” of startup accelerators that has spawned successes such as Stripe, Airbnb, and Coinbase—Silicon Valley Bank once dominated as one of the financial services that offered discounts to young companies, though others like First Republic also populated the list. In recent years, Mercury has popped up in the listings, as have credit card startups Brex and Ramp.

The upside for SVB is such companies are still young and don’t offer a major plus—venture debt—and, therefore, can lose customers as their businesses get older and need more financing. That, though, is a short-lived moat if they later grow to encompass such offerings. Moreover, as it is a great time for tech companies, even the traditional banking competition is fierce. While Chatbooks’ Jimenez had no complaints against SVB, he later switched over to another regional bank, Bridge Bank, because it offered better interest rates and even friendlier terms on the loans.

SVB certainly isn’t resting on its laurels—even if Becker unfurls the company’s road map in such amiable terms that it almost makes one forget his and the bank’s enormous ambitions in a highly competitive and cutthroat environment. The bank is rolling out a new online banking interface as a result of negative feedback it heard from some founders. And in fact, even as startups look to disrupt it, the bank is going after even larger targets in the form of the Morgan Stanleys, Goldman Sachses, and J.P. Morgans of the world. In previous years, SVB often lost pieces of the startup business as the companies grew older and needed more robust banking services to internationalize or to go public, says J.P. Morgan analyst Steven Alexopoulos, thus ceding territory to the bulge-bracket banking giants.

“We want to be a partner in every way: We want to be their company partner, we want to be their personal partner, we want to be their investment banking partner, and we want to be investing alongside them,” says Becker. In short, SVB wants to be the primary, if not the sole, bank for the extremely lucrative tech niche that it has found. “We’re also not kidding ourselves. It’s not going to be easy,” he adds.

If Becker’s words aren’t enough, SVB’s recent large acquisitions certainly point to the scale of the bank’s desire to keep maturing startups in its wheelhouse: In a bid to keep startup employees and founders in-network for their personal banking needs, SVB acquired wealth management company Boston Private for $900 million. In a sign that SVB is also after the highly competitive dealmaking and IPO market, it acquired Leerink Holdings in 2018, which has been aggressively poaching dealmakers from the likes of Citi, Bank of America, and UBS under the name of SVB Leerink.

As banks in general act as a kind of barometer of health for the overall economy, SVB’s stock is a gauge of the private markets as well. When the good times are good, as they are now, the stock looks incredibly attractive to investors. But when the waters get choppy, so too will the lines that demarcate SIVB’s performance on the S&P 500. In fact, just as this article has highlighted how the bank has benefited from the recent boom in tech companies going public, a 2015 Wall Street Journal article highlighted the struggles the bank endured after the then lackluster IPOs of Square and Jet.com. As an investment, that can make the stock quite volatile, notes J.P. Morgan’s Alexopoulos.

“When the market is robust and companies are almost all successful, it seems really easy. But it’s really when there are bumps along the way—and there always are—you have to know how to support these companies and work through the good times and the bad times,” says Becker. “I think that’s where the real secret sauce is, that you realize it is a long journey.”

More must-read finance coverage from Fortune:

- What is the “inflation trade,” and how can you play it in your portfolio?

- Everything to know about Cathie Wood’s new Bitcoin ETF

- Support for making Bitcoin legal tender grows in Latin America

- What will be the next big meme stock? Chatter on Reddit’s WallStreetBets offers hints

- Chinese tech IPOs fuel Hong Kong stock exchange’s best first half ever

Subscribe to Fortune Daily to get essential business stories straight to your inbox each morning.