Last year was all about staying afloat for Elizabeth Blount McCormick.

As the president and owner of Ohio-based travel management company Uniglobe Travel Designers, Blount McCormick found herself at the helm of a 40-year-old business that had the misfortune of operating in one of the hardest-hit industries in 2020.

“When the pandemic hit, everything kind of came to a screeching halt,” Blount McCormick recounts to Fortune.

She says revenues at Uniglobe dropped roughly 70% last year, from $37 million in 2019 to $10 million, and the approximately 35-employee company became unprofitable. But Blount McCormick also says her business actually added 24 new clients during the pandemic. “What I thought was, I’ve got to hold on, and then I’ve just got to tread water a little bit and not drown, because people see our value,” she recalls.

Since the rollout of vaccines, Blount McCormick feels like things are looking up. “I’m optimistic,” she says. “I just have to hold on a little bit longer. And I’m seeing an increase in the demand” for travel, as individuals are itching for vacations and corporations are lifting their travel bans.

Other Black small business owners are feeling more positive, too. According to a recent Reimagine Main Street survey of over 1,300 small business owners in partnership with organizations including the U.S. Black Chambers, 83% of Black business owners are optimistic about the future of their business, versus 70% of white business owners surveyed from April 28 to May 12. Black owners were also more confident than white business owners and business owners who belong to other minorities about the trajectory of the broader economy, boosted by optimism around vaccines.

To be sure, many businesses aren’t out of the woods yet. But across the general small business landscape, 65% of small business owners were optimistic that the worst of the pandemic was over, while 44% felt “hopeful” about their reopening or operating plan, according to a new U.S. Chamber of Commerce and MetLife Small Business Index survey released on June 15.

Trevor McKenzie is feeling mostly positive about his restaurant, Jerkin Chicken. McKenzie recounts that at one point, “We contemplated, should we shut our doors? Because it was virtually a ghost town” in Jersey City, where his restaurant is located. “But we hung in there because our business was primarily takeout,” he says. McKenzie tells Fortune his business, which includes food trucks and currently has five staff on payroll, was able to maintain “similar” revenues to 2019, having also received two government loans.

And with New Jersey reopening, “I think things are moving in the right direction,” says McKenzie, “once I’m able to find the proper staff.”

An uneven recovery

Despite their optimism, Black small business owners were less confident than white business owners about their revenues recovering in the near term. According to the Reimagine Main Street survey, 67% of Black owners believed it would be at least another six months before their revenue would return to pre-pandemic levels, versus 59% for their white counterparts.

According to the Federal Reserve Bank of New York’s 2021 Report on Firms Owned by People of Color, based on surveys conducted last fall, owners at Black-owned firms were the most likely to use personal funds to mitigate their financial issues, while 92% said they had experienced financial hardship in the prior 12 months, compared to 79% of those at white-owned firms.

Everett Sands, the founder and CEO of Lendistry, a Black-owned fintech and community development financial institution, says “across a kind of broad spectrum, we are anticipating that it’s going to take a little while to get back to normal” for the businesses Lendistry services.

Indeed, Black small businesses have taken a greater hit from the pandemic, bearing the brunt of closures early in the crisis. Per research from the Federal Reserve Bank of New York last year, there was a 41% drop in the number of active Black business owners from February through April in 2020, versus a 22% drop in the number of business owners overall and a 14% drop in white business owners. And a February survey by Facebook and the Small Business Roundtable found that 27% of minority-owned businesses were closed at that time, compared to 18% of other businesses.

Against that backdrop, even as the economy is now recovering, Black business groups, lenders, and owners continue to highlight many of the systemic problems Black businesses face—the same that helped the pandemic cause such devastation in the first place.

The capital problem

Ron Busby, the president and CEO of the U.S. Black Chambers (USBC), tells Fortune that by his estimate, access to capital is “always going to be a number one, top concern for Black-owned businesses.”

Uniglobe’s Blount McCormick, for one, would agree. “I think for most Black- and women-owned and minority-owned businesses, [the challenge is] just access to capital without all the hassle,” she says.

Blount McCormick was able to get two Paycheck Protection Program loans and an Economic Injury Disaster loan. But despite having a regular bank relationship, she went with a private lender for the PPP loans. She says that “when I talked to my banker initially, they told me to max out my credit cards to make it through. I’m like, what?” she recounts. “Banking while Black is very difficult, and that happens and it’s not surprising, unfortunately. So I found a private lender,” she said.

Indeed, Black-owned small businesses often face more hurdles in getting capital due to a variety of factors including the racial wealth gap, lack of collateral for loans, and often fewer banking relationships.

Early rounds of the government’s massive small business loan program, the PPP, initially left out many Black-owned businesses from receiving the forgivable loans. The program favored firms with established banking relationships, and it also proved difficult to access for many sole proprietors, which constitute the vast majority of Black businesses. In 2021, the reboot of the PPP (which ended on May 31) incorporated new changes intended to help smaller and Black-owned businesses receive loans, including $1 billion set aside for sole proprietors and a 14-day head start for smaller businesses to apply.

“It did better in the later stages than the beginning stages,” says Lendistry’s Sands.

But the problems Black business owners often deal with—including accessing capital, credit, and financial services broadly—still persist.

According to the Federal Reserve’s Small Business Credit Survey in 2021, conducted in September and October of last year, 30% of Black-owned firms listed credit availability as the primary concern moving forward as a result of the pandemic, the highest among any racial and ethnic group. At the time only 13% of Black-owned firms reported receiving all the financing they sought, versus 40% of white-owned firms. That’s despite Black-owned firms on average completing more applications for financing than white-owned firms, per the Federal Reserve Bank of New York’s minority firms report.

According to Sands, “It starts at the top. Are there minority deployers of capital? I mean, that’s where you have to start. You have to build rapport with the customer.”

Starting up (or over)

For many Americans, the pandemic presented the opportunity to create a job for themselves.

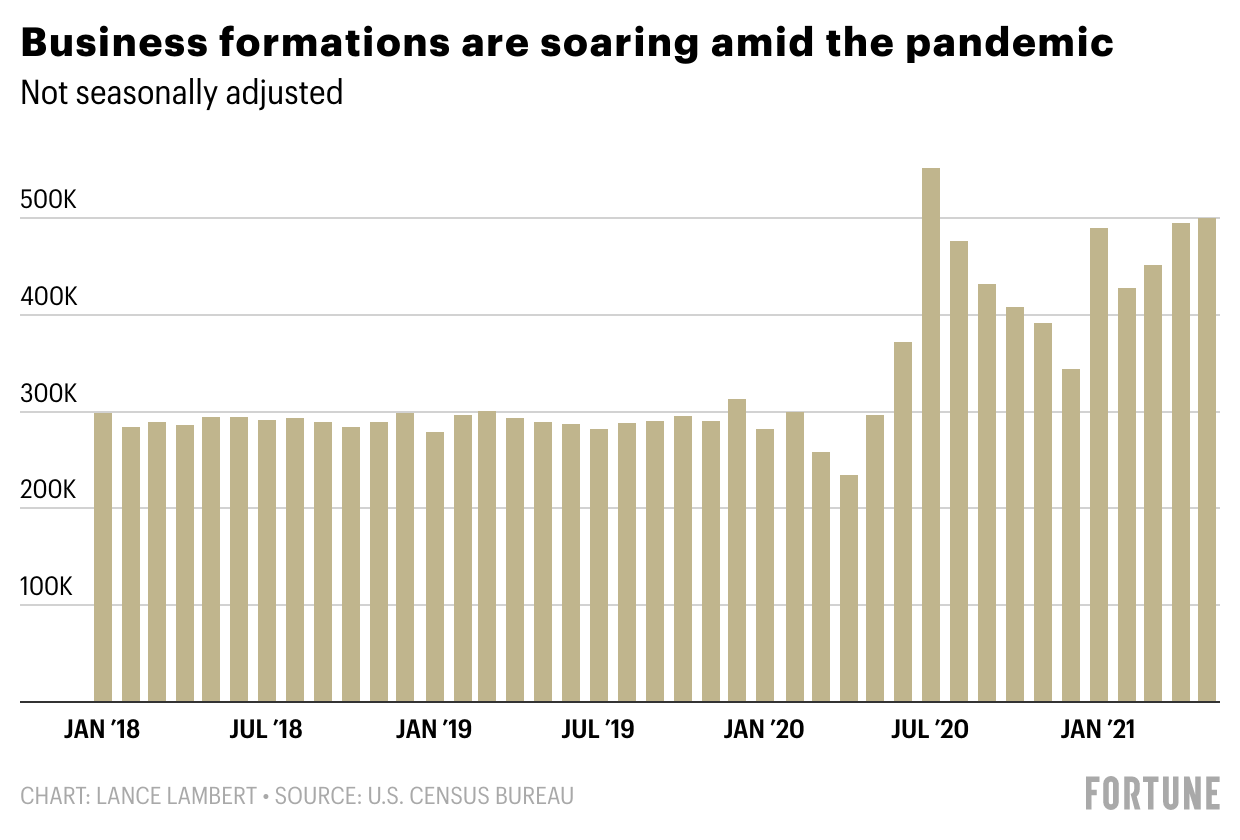

Since mid-2020, new business applications have been rising, up nearly 70% year-over-year in May 2021, per the latest U.S. Census Bureau data.

Though the Census Bureau told Fortune that demographic data, including the portion of applications coming from Black entrepreneurs, is not available, recent studies show that it’s Black women who are among the most active entrepreneurs.

Per a recent study conducted by Babson College and the Global Entrepreneurship Monitor, a global survey of entrepreneurship rates, 17% of Black women in the U.S. are starting new businesses or have started them in recent years, versus 10% of white women and 15% of white men. Rates of entrepreneurship are also high among Black men, with 23% of those surveyed starting or having started a business in recent years.

Yet Black women were also among the hardest-hit by unemployment during the pandemic. In February, while many unemployed groups were beginning to recover, employment for Black women was still 9.7% lower than pre-pandemic, compared to 5% and 5.9% for white and Black men, respectively. Now, it hovers at 7%, trailing the employment recovery for men. (Joblessness stands at around 4% for Black and white men.)

According to Angela Randolph, one of the co-authors of the Babson/GEM study and an assistant professor of entrepreneurship at Babson College, “It plays heavily into the unemployment dynamic,” she tells Fortune. “Black women (and Black men, and women in general) got laid off at higher rates, which meant that in some ways … you have more time, but you also have to figure out how you’re going to pay for things, so there’s a lot of necessity entrepreneurship,” she says. (One of the study’s other co-authors, Donna Kelley, told Fortune via email that for data collected in 2020, “there was a higher level of necessity-driven entrepreneurship” overall with 50% of new business founders citing “job scarcity as the reason for starting in 2020, [versus] 41% in 2019.”)

On top of that, the pandemic uncovered many problems consumers and businesses were facing, and “anytime you have problems to solve, you have entrepreneurs start to try and solve the problems,” Randolph notes.

But per the Babson/GEM research, only 3% of Black women are running mature businesses (those older than three and a half years). There are a variety of possible factors at play in that drop off, suggests Randolph, including problems with accessing capital and resources and the reliance on savings to support the business in the early stages.

To sustain those startups, Randolph argues “there needs to be more time and thought put into the biases of the people making the decision” when it comes to “credit decisions for banks or equity decisions or … funding decisions from equity funds.”

‘Going down the right path’

In the wake of the murder of George Floyd and the Black Lives Matter movement in 2020, a slew of corporations pledged money to fight racial inequity and fund Black businesses and communities. However, since then, results of those commitments have been mixed—and less than impressive.

According to a recent study by the Creative Investments Group, U.S. companies promised some $50 billion toward racial equity after the murder of Floyd last year. But the study at the time found that only $250 million had actually been allocated.

Those like USBC’s Busby argue “the commitment was there, but the follow-up has not been.” Many Black business owners “are saying, ‘We want access to capital, access to contracts, and access to technical assistance’,” Busby says. “It’s one thing to provide the funds, but I think it’s equally as important to provide the technical assistance that all business owners need”—ranging from legal assistance to accounting.

Yet there continue to be efforts to support Black businesses and entrepreneurs, including Amazon’s announcement this week of its Black Business Accelerator, a $150 million commitment over four years to provide financial support and mentorship. Wall Street titan Goldman Sachs also committed $10 billion in direct investment for Black women’s education, small business, and employment over the next 10 years with its One Million Black Women initiative.

And the Biden administration recently made a sweeping commitment to help address racial inequity and the wealth gap, announced in conjunction with the 100th anniversary of the Tulsa massacre. That commitment includes actions designed to eliminate racism in the housing market (a key input when it comes to using collateral to secure loans) and to award more federal contracts to disadvantaged and minority-owned firms.

Those like USBC’s Busby believe that “as proposals are being discussed, Black people feel good about it,” he says. “But we want to make sure that there’s some rubber that will also hit the road.”

“I think we’re going down the right path,” adds Busby. “I just think we can’t allow this moment and the future to forget what has happened over the last 400 years.”

Like many of their fellow business owners, Blount McCormick and McKenzie are now feeling a bit more confident about their situations as the recovery takes shape.

Blount McCormick says she’s expecting 2022 to be a big year for Uniglobe. But in the meantime, she says she still needs “a cash injection, honestly, to help us get through” the next few months, adding that she’s “scouring the internet” for additional grants.

“Just a few more months,” says Blount McCormick, “and then I’ll be okay.”