Our mission to help you navigate the new normal is fueled by subscribers. To enjoy unlimited access to our journalism, subscribe today.

Ask Catherine Monson what she wants most from the election, and her first words aren’t about issues like tax rates, trade, or regulation, at least not directly. She’s CEO of Fastsigns, a franchisor of stores that make custom signs and graphics products, with about 700 franchisees worldwide, so all those issues affect her business. But what does she want most? “What helps us is certainty, the ability to plan,” she says. “Every presidential election now, you don’t know what’s going to happen. We don’t want regulatory or policy whiplash. We want predictability.”

As America’s business leaders think about what they need in the postelection world, they keep coming back to the same words—stability, predictability, certainty. They’ve also got specific policy wish lists. But while the policies vary by industry, business leaders across the economy acknowledge the same overarching desire for a more temperate political climate. “The business community is a small-c conservative group,” says Douglas Holtz-Eakin, former director of the Congressional Budget Office and now president of American Action Forum, a center-right think tank. “They don’t like rapid and radical change.”

That’s understandable; many companies grow by making large investment decisions that may take years to pay off. Yet as ardently as businesspeople want this election to produce greater policy stability, they’re unlikely to get it. The more probable outcome is that business will have to adapt to a disorienting new rule book in Washington and in government at all levels nationwide.

This is a crossroads election for business and the U.S. economy, which is why we’re examining what’s at stake for a wide range of industries, from Wall Street to Silicon Valley, and for many workers. (To see the full package of stories, you can go here.) Business leaders are uncertain of Vice President Joe Biden as President. They’re wondering if he’d be the moderate Joe of his Senate years, working across the aisle, or if he’d push the priorities of the Democrats’ left wing, whose support he needs. And the business community is grateful that Trump kept his two main promises to them—lowering taxes and reducing regulation—during his first year in office. But managers on the whole don’t like escalating trade wars, anti-immigrant policies, and chronic policy flip-flopping, which were at the core of Fortune’s argument last fall that Trump had become bad for business. His bellicose performance in the first presidential debate probably didn’t comfort businesspeople hoping for more orderly policymaking.

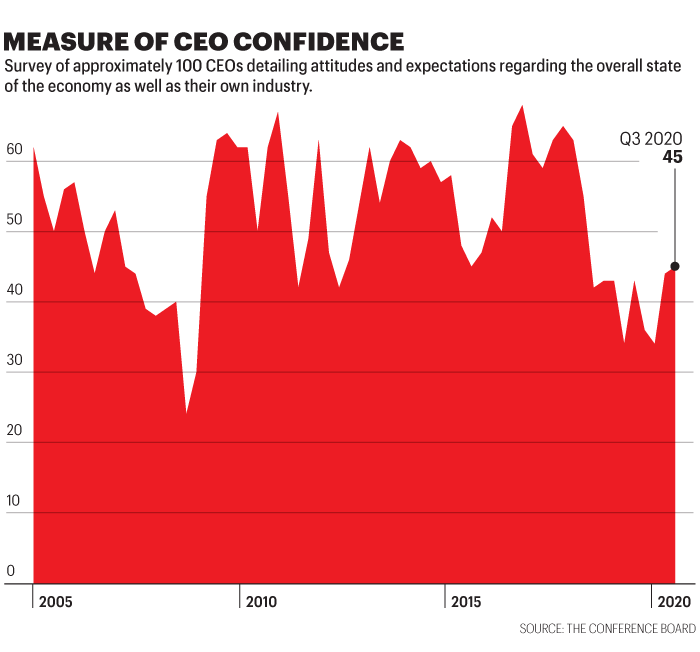

The Conference Board’s measure of CEO confidence reflects the change of mood. While CEOs are more confident than they were last spring, in the darkest days of the pandemic’s arrival, they’re still nowhere near as confident as they felt in Trump’s first year.

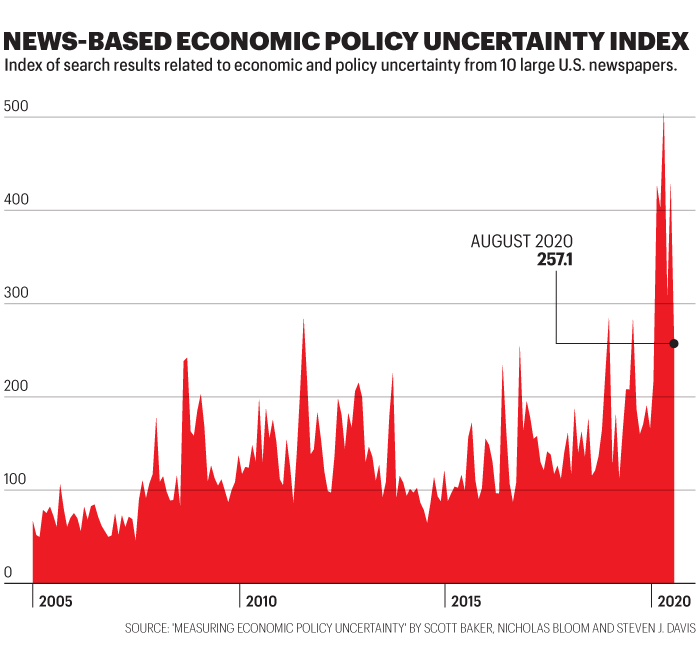

On the broad issue of uncertainty, it’s tempting to accuse business leaders of whining. After all, life is uncertain. Wasn’t it ever thus? Actually it wasn’t. Researchers from the University of Chicago, Stanford, and Northwestern University created a policy uncertainty index based on computer analysis of news reports going back to 1985. It shows that policy uncertainty has recently been higher than ever, by a hefty margin.

The tumultuous policies that have wearied so many businesspeople are highly correlated with President Trump’s mercurial nature. He has reset the plans of multibillion-dollar industries with a single tweet. Last December, for example, he tweeted, “effective immediately, I will restore the Tariffs on all Steel & Aluminum that is shipped into the U.S. from [Brazil and Argentina].” The Dow plunged 326 points on the news. Eighteen days later he took it all back. No tariffs. Trump, who has said his unpredictability gives him a competitive advantage, has made several such reversals.

In addition, while business has generally applauded Trump’s broad regulatory rollbacks, some companies have found them too impulsive. When he said he’d all but eliminate an Obama regulation reducing auto emissions, California said it would continue enforcing the existing rule. Four major carmakers—Ford, Volkswagen of America, BMW, and Honda—negotiated with California to adopt a new, slightly weakened rule that the manufacturers would apply to all their vehicles nationally. In a joint statement, they said the deal gave them “much-needed regulatory certainty.”

Craving compromise

But it isn’t just Trump. Lurching policy swings are inevitable as partisanship, tribalism, and extremism increase broadly in U.S. politics and society. Trump’s Tax Cuts and Jobs Act was enacted in 2017 with zero Democratic votes. President Obama’s Affordable Care Act was enacted in 2010 with zero Republican votes. Businesspeople now must struggle to make plans knowing that epochal legislation could be repealed the moment the other party gets a majority, as it someday will.

In that environment, some business leaders want this election to produce divided government. “They want more stability,” says a former Capitol Hill staffer who now advises major corporations, “and the most stable outcome would be a Biden win but a Republican Senate.” Divided government forces the two parties to engage and compromise in order to enact legislation. It has been the norm for most of America’s post–World War II history, and research has shown that it’s better than unified government for the economy and the stock market. But while divided government could continue, businesspeople shouldn’t get their hopes up.

Vote-splitting is in steep decline. In the 2016 election, for the first time since the direct election of senators began in 1914, every state that went for the Democratic candidate (Hillary Clinton in this case) and was also electing a senator chose a Democratic senator, while every state that went for the GOP candidate (Trump) and was also electing a senator chose a Republican.

The trend continued in the 2018 midterms. Elections analyst Geoffrey Skelley at FiveThirtyEight studied states that were electing both a governor and a senator. His conclusion: “Split-ticket voting hit a new low.” As Americans increasingly identify themselves as members of warring tribes, they’re less likely to see virtue in any candidate from the other side and far more likely to vote a straight ticket.

This year many business leaders have a particular reason for fearing that Democrats will win the White House and Senate while holding control of the House. One of the great moderating forces in federal legislation is the Senate filibuster rule, which requires 60 votes to end debate and advance an item to a floor vote. But Senate Democrats eliminated it for executive office appointees and judicial nominees below the Supreme Court in 2013, and Senate Republicans eliminated it for Supreme Court nominees in 2017 and 2018.

The filibuster remains in effect for legislation. But President Obama, Senate Minority Leader Chuck Schumer, and former Senate Majority Leader Harry Reid have all urged Democrats to consider ending the filibuster entirely if they gain control of the Senate. With control of the House and White House as well, the party could in theory enact any part of its agenda quickly and easily with simple majorities. Republicans could do the same if they eventually win the Washington trifecta.

That scenario badly worries business. “Change of some kind is likely no matter the political outcome,” says Steve Caldeira, CEO of the Household and Commercial Products Association, “but it just shouldn’t be radical change, especially during these volatile times.”

While voters generally think Trump would manage the economy better than Biden would, some prominent economists disagree. Recent number crunching by Moody’s Analytics forecasts that a Democratic sweep of the presidency, House, and Senate would produce much higher economic growth, more jobs, and higher real disposable income over the next decade than would a Republican sweep or divided government under either candidate as President. Goldman Sachs economists conclude that Biden’s policies “would likely result in a similar level of medium-term S&P 500 profits as our baseline forecast that assumes no major policy changes.” (For a detailed breakdown of where both candidates stand on eight major economic issues, see the table at the bottom of this article.)

The larger issue for business is the advent of a new model for dealing with government. For decades business has pursued its policy interests in a world where compromise and moderation usually prevailed, even after bare-knuckles combat. That’s what businesspeople yearn for after this election. “How do we get back to where we can disagree and be friends?” asks Monson. “The tribalism is terrifying. The balkanization is terrifying.” Yet virtually every trend is pointing toward greater division, not less.

4 big priorities

If the election’s winner can work with Congress, and Congress can stifle its internal warfare—big assumptions—here are four of the business community’s top priorities:

A substantial new pandemic relief bill.

“Measures to fully and quickly recover from the pandemic-induced recession” are the No. 1 priority for the U.S. Chamber of Commerce, Washington’s largest lobbying organization, says chief policy officer Neil Bradley. Many other major business associations feel similarly. It’s a sign of Washington’s debilitating partisanship that Congress can’t agree on a bill that any legislator ought to be happy to take home. “We’ve been surprised,” says Bradley. “Extending benefits is not just good policy, it’s good politics.”

Mostly open, low-tension trade agreements.

Business generally hates the trade war with China and hastily imposed tariffs on U.S. allies such as the European Union and Canada. For every industry protected by a tariff, several others are hurt by the increased cost of the tariffed item; for example, “End the trade war” is the No. 1 policy priority of the National Retail Federation, whose members rely on Chinese merchandise. Additional industries are hurt by tit-for-tat tariffs imposed by other countries.

Continued low taxes.

The Tax Cuts and Jobs Act of 2017 lets businesses expense certain capital investments, but that provision begins to phase out in 2023. In addition, the TCJA gives individuals several tax breaks—an increased child tax credit and standard deduction, for example—that are scheduled to expire at the end of 2025. Business wants those stimulus measures made permanent.

A major infrastructure bill, at last.

Congress’s failure to pass such a bill has become a running joke in Washington. Like the failure to pass a new pandemic relief bill, it’s puzzling. Seemingly since the dawn of time, legislators have loved sending federal money back to their districts. But in today’s hyper-partisan Washington, the two parties can no longer compromise on where the money will go, for what purpose, etc.

The business community wants large yet moderate economic action from Washington. But just trying to forestall rapid and radical policy change may no longer work. For business, come what may in November, it’s time to learn how to deal with it.

Where Biden and Trump stand on economic policy

Below is an overview of each candidate’s stated policy plans in eight key areas. Information for Biden comes largely from the Democratic Party Platform plus Biden’s speeches. Information for Trump comes from his campaign website and speeches; the Republican Party, for the first time in its 164-year history, did not issue a platform for this election.

| Biden | Trump | |

| Corporate taxes | Would raise the corporate tax rate from 21% to 28%; would offer tax incentive to companies that bring overseas operations to the U.S. and make certain green investments, among other things. | Would extend expensing of certain capital investments, currently set to phase out starting in 2023; would offer tax incentives to companies that bring overseas jobs to the U.S. |

| Individual income taxes | Would tax capital gains and dividends as ordinary income for high-income individuals, increase tax rates for high-income individuals, impose a 12.6% Social Security payroll tax on income over $400,000, limit tax benefit of itemized deductions. | Would prevent tax rate increases, an increased child tax credit, increased estate taxes, and other changes by extending tax code provisions set to expire at the end of 2025; would index capital gains to inflation. |

| Infrastructure spending | Would increase it by $2.4 trillion during his term. | Would increase it by an estimated $1 trillion. |

| Health care | Under the Affordable Care Act would establish a new public option available to all; low-income individuals could be automatically enrolled in no-premium coverage; Medicare could negotiate prescription drug prices; importing lower-cost drugs would be permitted. | Would reduce Medicare payments for graduate medical education, uncompensated care, and other uses; would impose self-sufficiency and work requirements for Medicaid recipients. |

| Workforce | Would mandate paid family and medical leave for up to 12 weeks. | Has advocated paid family leave but has not included it in his second-term agenda. |

| Trade | Would include standards for labor, human rights, and the environment in future trade agreements. | Would “enact fair trade deals that protect American jobs,” according to campaign website. |

| Regulation | Would raise the federal minimum wage to $15; pass the Protecting the Right to Organize (PRO) act and facilitate union organizing in other ways; create a public credit reporting agency and require its use by federal lending programs; would “reinvigorate” the Consumer Financial Protection Bureau; would eliminate forced arbitration clauses in employment and service contracts; would increase scrutiny of mergers and acquisitions. | Would continue to deregulate U.S. energy industry; would prohibit federal contracts for companies that outsource to China. |

| Immigration | Would increase protection for Dreamers; provide a roadmap to citizenship to undocumented immigrants; end workplace and community raids. | Would “prohibit American companies from replacing U.S. citizens with lower-cost foreign workers,” according to campaign website. |

More from Fortune‘s special report on what business needs from the 2020 election:

- What voters need from the 2020 election: Common ground

- What Wall Street needs from the 2020 election

- What unemployed Americans need from the 2020 election

- What small-business owners need from the 2020 election

- What unions need from the 2020 election

- What low-wage workers need from the 2020 election

- What working parents need from the 2020 election