“Only when the tide goes out do you discover who’s been swimming naked.”

In today’s frenetic debt market, Warren Buffett might want to add a corollary to his oft-repeated comment on the trouble that befalls weak companies when recessions come.

That is, there are a lot more companies swimming naked today.

Thanks to razor-thin interest rates over the past decade, U.S. companies have doubled their borrowing since 2008 to around $10 trillion, with much of the new debt in the form of high-yield bonds given to weak companies, known as junk bonds.

So far, this gorging on debt has led to relatively few defaults, which happens when debt issuers can’t pay the bond’s interest or the principal as it comes due. But once the next recession rolls in—or when the tide goes out, in the Oracle of Omaha’s words—the riskiest junk bonds likely will be in trouble.

And this time around, the danger to investors doesn’t end with junk. Today, two other tentacles of post-crisis corporate finance are making the debt threat worse: “lev loans” and looser debt-issuing rules.

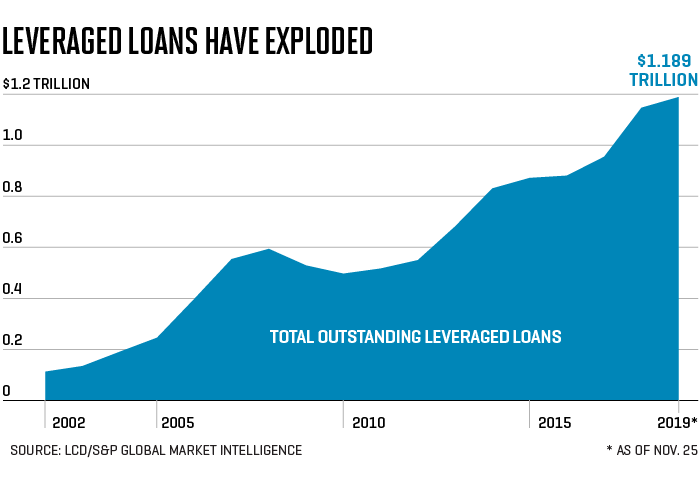

In the first instance, there has also been a surge in bank loans to high-debt companies, called leveraged loans, or “lev loans” in Wall Street parlance. These loans are the doppelgänger of junk bonds. For companies, the loans are attractive because they’re cheaper than bonds, which charge higher interest. The amount of lev loans has quadrupled in size since before the financial crisis, to over $1 trillion, according to the S&P/LSTA Leveraged Loan Index. More of them means they are at greater risk if the economy goes south.

And in the second, the rules that protect both lenders and bond investors, called covenants, are a lot looser today that they were in the past, a kind of weak protection known as “cov-lite.” Corporate executives enjoy cov-lite, of course, because they don’t have to worry about following pesky requirements, like maintaining high cash flow levels, and the eased restrictions have smoothed the path for a flood of new junk bonds and leveraged loans from companies that probably wouldn’t have been able to take on the debt in the past.

Corporate America’s overweening debt and weak covenants are an accident waiting to happen, according to fixed-income impresario Jeffrey Gundlach, CEO of asset manager DoubleLine. He warns that the problem’s size means that cleaning up the eventual imbroglio, once everything goes wrong, will be daunting. “When you have the recession, there won’t be an ability to fix it,” he said during a London speech in September.

How bad could the next mess be? Right now, the load of U.S. junk bonds outstanding is valued at $1.5 trillion. Leveraged loans are almost as high, around $1.2 trillion. Adding them together, you near the size of the mortgage-backed securities that imploded during the 2008 crisis—and crippled the world economy. And that’s not all. Some 80% of junk issues and lev loans are cov-lite, giving issuers too much leeway, to the detriment of investors.

Leveraged loans lift off

In the world of mergers and acquisitions, loans have been a key financing tool since the 1980s leveraged buyout days. To banks, they are a great way to provide more fee-producing capital to the private equity industry.

Here’s the appeal for corporate borrowers: Lev loans charge around 0.75 point less in interest than junk bonds. The reason: In a bankruptcy, loans rank higher than bonds on the credit spectrum, so lenders get paid back more of what they’re owed than do bondholders. Hence, loans are seen as less risky for banks, relatively speaking.

Even more appealing for borrowers, the loans are callable from day one, giving companies great flexibility to refinance on the spot if rates decline. Bonds, on the other hand, typically can’t be called for three to five years. That’s tough luck for lenders, who count on a nice yield for years to come from their lev loan, averaging around 5.25%, a level that’s much sweeter than a 10-year Treasury note paying just 1.8%.

For banks, another attraction of lev loans is that they don’t have to carry such loans on their books, constantly worrying that they might default. Lev loans instead are packaged into securities known as collateralized loan obligations, or CLOs, which are usually sold to institutions, like pension plans or university endowments.

Should the loans bundled together in CLOs blow up, the banks then are free and clear. Some two-thirds of lev loans have been collected into these syndication vehicles.

Right now, the default rate on leveraged loans is very low: a measly 1.42%. And the average historical default rate for these loans is 3.1%, while the rate for junk bonds (also called high-yield bonds) is a bit higher at 3.3%.

However, there is reason to believe that the default rate will regress to the norm—or even go much higher. The economy has been good in recent years, and in hard economic times the situation grows more dire for lev loans. In 2009, the last year of the Great Recession, defaults on lev loans soared to 11%, comparable to high-yield bonds.

The big danger of lev loans lies in the eerie similarity the CLOs bear to the mortgage securities instruments that imploded during the financial crisis. Housing boom mortgages were collected into bonds, which in turn were placed into CLO-like instruments, known as collateralized debt obligations or CDOs. When the mortgages went belly up, a lot of CDOs imploded, leaving investors with nothing, other than regret.

CLOs’ defenders say that they are a lot safer than the mortgage version that the housing boom spawned. In a report delivered in April, S&P Global Ratings insisted that “we now have more visibility on the performance” of CLOs, meaning more visibility on the loans.

For a top-rated CLO, the S&P report indicated, if two-thirds of its corporate loans defaulted now, investors would get back as much as 40% of their money. While that would be an improvement on the mortgage wipe-outs during the crisis, hapless investors still would be out a lot of dough. The real stress test for CLOs, however, will be the next recession. The report predicted that, owing to higher lev loan volume and the cov-lite growth, CLO investors could suffer more in a downturn than in the past.

Covenant-lite fright

Before the current debt binge, investor protection covenants used to be strict. A company, for instance, might be barred from taking on debt above a certain point, or perhaps be required to maintain a certain debt-to-cash-flow ratio. Once the issuer violated the covenants, then creditors could demand repayment of their principal immediately.

No more. Today, cov-lite, where the customary safeguards are minimal or nonexistent, is a bigger trend than plant-based meats, at least in the debt world. Currently, 80% of leveraged loans and junk bonds sport weak or no covenants, compared to 5% right before the financial crisis.

So why would anyone want to invest in a cov-lite issue, other than perhaps out of ignorance? The reason is money: cov-lite debts pay their investors higher interest rates, around 0.9 percentage points more than traditional covenant-bound debt, due to the higher risk.

The problem is, without adequate covenant safeguards, troubled companies can grow even sicker and lurch along, zombie-like, until they collapse, delivering still more pain to debt holders. “Aggressively financed transactions and weaker protections for investors is a problematical mix,” wrote Andrew Watt, lead analytical manager for corporate ratings, at S&P Global Ratings.

In light of dubious leveraged loans and threadbare covenant protection, in addition to teetering junk bonds, the credit markets and a lot of fixed-income investors should brace themselves for rough seas ahead.

More must-read stories from Fortune:

—2020 Crystal Ball: Predictions for the economy, politics, technology, etc.

—In scooter startups, landlords see a competitive edge and the city of the future

—Big tech companies avoided over $100 billion in taxes. What that means

—How blockchain will shake up the financial world

—What went wrong at Chime? How rapid growth became its own challenge

—Don’t miss the daily Term Sheet, Fortune’s newsletter on deals and dealmakers.