A LOOK AHEAD

Good morning, Term Sheet readers. In today’s guest column, Upfront Ventures managing partner Mark Suster takes stock of how limited partners are feeling about the state of VC investing.

Every year Upfront Ventures surveys limited partners (LPs), the main source of capital in venture capital funds, and thus the main source of capital that goes to startups, to get an early-warning sense of the year ahead. (Leaving aside any black swans, of course.)

The results are in and a few things are clear (you can read the full deck here):

—Limited partners are at their most optimistic phase about venture since the great recession of 2007–2009.

—LPs believe that the venture markets have permanently changed and that there are now three distinct buckets in venture: seed, A/B, and growth stages.

—LPs have moved beyond their strict belief that there is “the best and the rest” and now acknowledge that some of the best performers in the past decade have been what, a decade ago, were emerging managers or non-existent. Among them: First Round Capital, Union Square Ventures, Lowercase Capital, Foundry Group, Spark Capital, IA Ventures, Founder Collective. All of these names were not started in Silicon Valley. LPs are now looking for a combination of “established top tier” and “new managers with differentiation.”

—LPs now view co-investment opportunities much more favorably than they did a decade ago. Almost half of all LPs are quite active in them and one-third say it’s one of the primary reasons they’re in venture.

—LPs we surveyed anonymously, ahead of the recent Presidential Inauguration, were overwhelmingly anti-Trump. Zero respondents said he was “the right leader” for our country; however, in equal numbers, LPs didn't believe that a Trump presidency is likely to have negative consequences for the venture capital and startup industry.

Here are some details. (Many thanks to Chang Xu for her help to prepare and analyze this data.)

If you met with LPs to raise a fund in between 2009 and 2012, the most common refrain was, “We have too many managers and too many dollars in venture. We’re trying to limit our exposure.” That has changed dramatically in the past five years. At the tail end of this period, when demand was picking up for the industry, there was still a belief in venture that it only mattered to be among the top 10 funds in Silicon Valley.

There is no doubt LPs still want access to the most elite funds. But increasingly LPs have acknowledged that the industry has changed. Some of the best performing managers have come from new firms, and many are outside of Silicon Valley. LPs, it seems, are more open to “new names.”

As our industry’s riches have grown, and startups have stayed private for longer periods of time (and raised significantly more private capital than they did in the past), an increasing number of LPs have sought to do “co-investments” with the funds that they back, giving them more exposure to what they hope will be the better-performing portfolio companies.

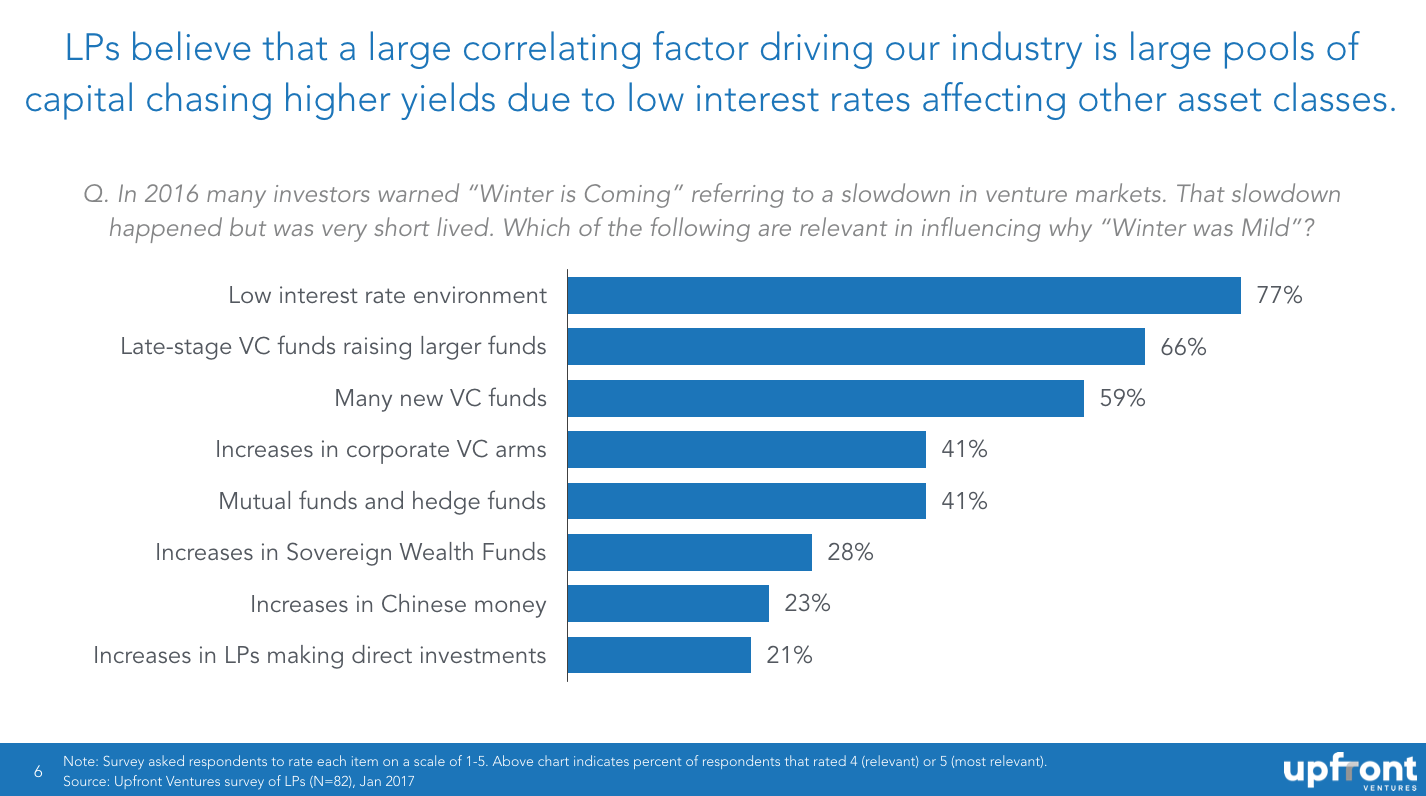

Want to understand why LPs are so active in venture today? The most obvious reason is that technology startups have paid off handsomely for many LPs. (A more nuanced answer would include the phrase “relative to other asset classes.”) This is key. In a permanently low-interest-rate environment, parking large pools of capital in assets that benefit from interest is not possible, so LPs seek “higher yield.” I know most startups (or even VCs) tend not to think about this. But when you ask LPs, the data is clear.

Another trend we’ve noticed among limited partners involves seed funds. When people like Michael Kim at Cendana or Hans Swildens at Industry Ventures a decade ago started focused on “Micro VCs,” we heard many LPs saying, “I’m not sure if seed fund investing is really a smart strategy. Will it last? Will they get squeezed? Will they have enough capital?” We never hear that any more. Seed-fund investing is believed to be a permanent force in our industry, with too many great funds to list. (Aside from those I listed previously, there is obviously Felicis, Softtech, Floodgate, K9, Forerunner, Cowboy—and so, so many more that I’m already in trouble for not naming another 20, I suspect.)

Late stage/growth venture capital sucks up the most amount of capital in aggregate in our industry. There was a movement by some of the larger VCs to say that traditional VCs would “get squeezed,” but LPs don’t buy it. More LPs said that traditional A/B VC funds were the “best fit” for them than any other kind. But the reality is that most LPs wanted a “healthy mix” of seed, A/B, and growth.

As for President Trump: Not a single limited partner surveyed said Trump was the right leader for the United States. A clear 71% said they disliked Trump, were anti-Trump, or were “deeply offended” by Trump.

Questions? Comments? Want more information? Follow me on Twitter or check out my blog. —Mark Suster

THE LATEST FROM FORTUNE...

• Neiman Marcus is struggling.

• Inside Deutsche Bank’s strategic overhaul.

• We might be getting a Facebook “dislike” button after all.

• The VCs who passed on Snapchat.

• We’re thinking about weight loss all wrong.

• When the IoT goes too far: introducing the smart condom.

...AND ELSEWHERE

When your cat is ruining your credit score. Millennials and egg freezing. The “Uber of jets” extorting journalists for positive coverage. Time Inc's uncertain future. On losing and loss.

VENTURE DEALS

• Atom Bank, a U.K. provider of mobile-based banking services, raised £83 million ($102 million) in funding at a post-money valuation of £261 million ($320 million), according to TechCrunch. BBVA led the round.

• Brayola, an Israeli ecommerce bra brand, raised $5 million in funding, according to Globes. The Firstime fund led the round, and was joined by Gett founders Shahar Waiser and Roi More, along with other angel investors. Read more.

• Raken, a San Deigo, Calif. reporting, compliance, and project visibility SaaS application for the construction industry, raised $2 million in funding. Rincon Venture Partners led the round, and was joined by Eniac Ventures and Spider Capital.

HEALTH + LIFE SCIENCES DEALS

• InGeneron, a Houston regenerative medicine and cell therapy company, raised $20 million in Series D funding from Sanford Health.

PRIVATE EQUITY DEALS

• Pollen Street Capital and BC Partners have put forward a joint offer to acquire Shawbrook Group (LSE:SHAW) for £825 million ($1 billion), according to Reuters. Pollen Street Capital already owns 38.9% of the bank. Read more.

• TA Associates acquired a minority equity interest in Interswitch, a Lagos, Nigeria integrated digital payments and commerce company backed by Helios Investment Partners. Financial terms of the transaction were not disclosed.

• Subsea Global Solutions, a Lariat Partners portfolio company, acquired All-Sea Underwater Solutions, a Canadian provider of ship repair and maintenance services.

• Welsh, Carson, Anderson & Stowe invested in Consumer Safety Technology, a Des Moines provider of breathalyzers installed in vehicles to prevent ignition by intoxicated drivers.

• General Atlantic invested in General Information Services, a Chapin, S.C.-based provider of background screening services.

• J.C. Flowers & Co. agreed to acquire UK General Insurance Group, a U.K. provider of personal lines insurance products for service brokers. Terms weren’t disclosed.

• Wafra Investment Advisory Group, a New York investment manager, acquired a minority stake in TSG Consumer Partners, according to the WSJ. Read more.

• Norwest Equity Partners invested in Bailiwick, a Chaska, Minn. provider of IT services. Financial terms weren’t disclosed.

OTHER DEALS

• General Motors (NYSE:GM) agreed to sell its European division, which includes the brands Opel and Vauxhall, to PSA Group (ENXTPA:UG) for $2.33 billion. Read more at Fortune.

• Answers, the New York owner of websites including Answers.com and Multiply, filed for bankruptcy. The company was acquired by Apax Partners for around $900 million in 2014. Read more.

IPOS

• Silver Run Acquisition Corporation II, a Houston blank check company, filed to raise up to $400 million in an initial public offering. The company plans to trade on the Nasdaq under the symbol SRUNU. Citigroup, Credit Suisse (SWX:CSGN), and Deutsche Bank are the joint bookrunners on the deal. Pricing terms weren’t disclosed.

• Credit Suisse (SWX:CSGN) hired an investor relations manager as it moves to divest its minority stake in its domestic bank, according to Reuters. The company has said it plans to raise up to $4 billion via an IPO, although a sale is also possible. Read more.

EXITS

• SFW Capital Partners agreed to sell Essen BioScience, an Ann Arbor, Mich.-based provider of instruments used for drug discovery and basic research applications, to Sartorius for $320 million in cash.

FIRMS + FUNDS

• KKR (NYSE:KKR) raised $13.9 billion for KKR Americas XII, a fund focused on investments in private equity-related transactions in the U.S., Canada, and Mexico.

• Actis, a London-based private equity and venture firm, raised $2.75 billion for its latest energy fund, which will make investments in Latin America, Africa, and Asia.

• Quad-C, a Charlottesville, Va.-based private equity firm, raised $1.1 billion for its latest fund, Quad-C Partners IX.

SHARE TODAY'S TERM SHEET

Term Sheet is produced by Laura Entis. Submit deal items here. View this email in your browser.

{kind=link}

{kind=link}

{kind=link}

{kind=link}