World authorities from President Barack Obama to International Monetary Fund head Christine Lagarde all warned the U.K. of economic disaster if it chose to leave the EU. But the first hard statistics coming in since the fateful “Brexit” vote suggest that the sky isn’t falling in … yet.

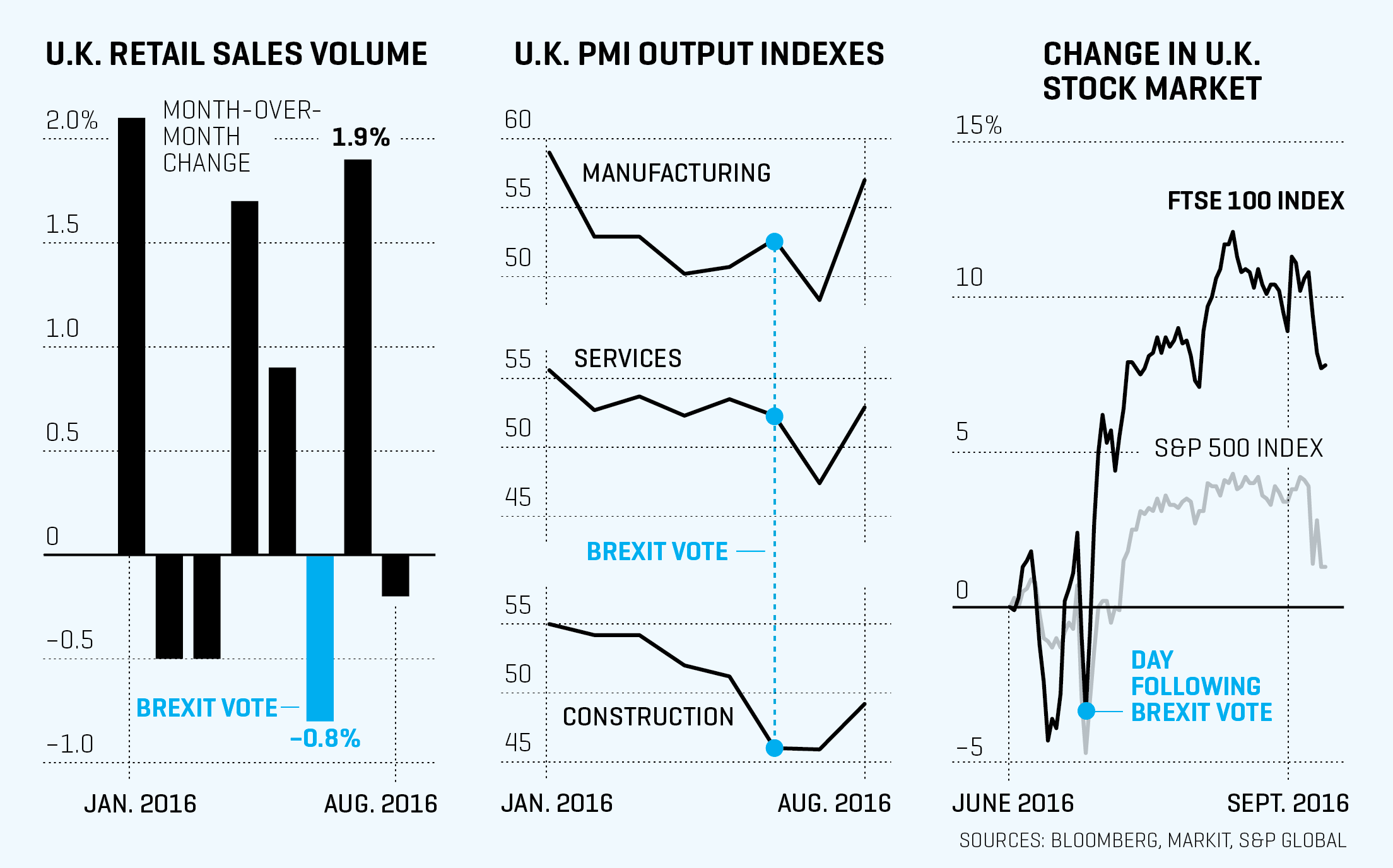

According to the Confederation of British Industry, exporters’ order books hit their highest level in two years in July, and most expect them to keep rising in coming months. Meanwhile, retail sales actually came back in style in July, while a clear majority of firms surveyed expected output volumes to rise over the next three months. Overall, FTSE 100 companies recouped their post-Brexit stock losses and then some.

On Main Street, the sunny picture is similar: retail sales rose a chunky 1.4% from June, leaving sales up 5.4% year-on-year (after excluding volatile seasonal elements). No-one forecast that after seeing the biggest drop in 26 years in GfK’s consumer confidence index immediately after the vote.

So were the doomsayers wrong? Not necessarily.

They may, as every disappointed stock-picker laments, have been “right too early.” In the short run, the Bank of England’s first interest rate cut since 2009 (and the 11% drop in sterling that anticipated it) has acted as a shock absorber just as the economics textbooks describe. The government’s hints that it will ditch its ambition to balance the budget by 2020 have also dispelled the fear that austerity could make things worse.

Brexit still has the real potential to do real harm to both the U.K. and EU economy, through the erection of barriers to new trade, choking of capital inflows, and diminished free movement of labor and talent. But it’s worth appreciating the good news while we can: the first major obstacle—the risk of a self-fulfilling spiral of fear and recession—has failed to materialize.

A version of this article appears in the October 1, 2016 issue of Fortune with the headline “The Brexit Crisis That Wasn’t.”