The political press has spent the week dissecting every last speech and tweet made by Donald Trump or his surrogates during the Republican National Convention, in hopes of divining how the week-long event would help his chances of winning the presidency in November.

But what has not been said in these many thousands of articles and television appearances is that no matter what the Donald Trump campaign does, there are certain variables—related to the U.S. economy—that will directly affect his chances that Trump actually has no control over.

In past elections, when there are healthy and improving economic conditions in the quarters leading up to a presidential election that usually been good news for the incumbent party. That is, of course, bad news for Donald Trump, as nearly all the of the most important econometrics would suggest a Hillary Clinton victory this fall. Here are three charts that show why Donald Trump will lose in November:

Consumers are feeling perky

Macquarie Capital Markets Analyst David Doyle points out in a recent analyst note that preliminary GDP data from the Federal Reserve Bank of Atlanta show personal consumption expenditures will grow by an annualized 4.5% quarter-over-quarter, or the fastest since 2006. That’s a pretty good indicator of how people are feeling.

“Macro data continues to show that the global economy’s $13 trillion gorilla, the U.S. consumer, is getting even stronger,” he writes.

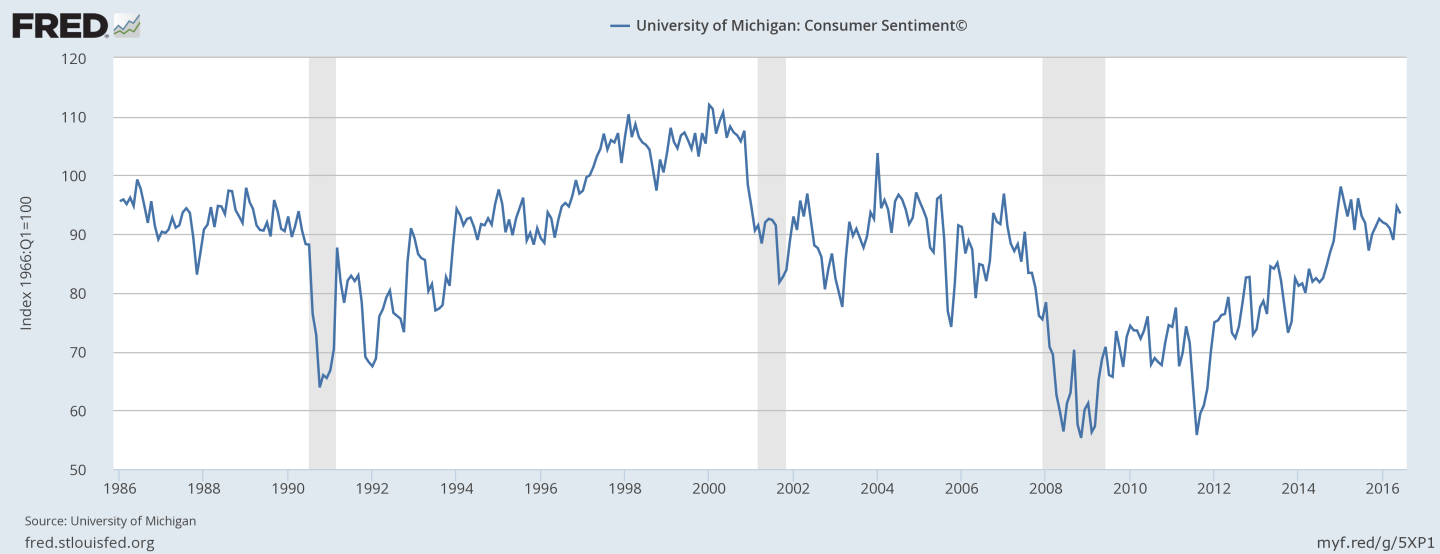

Meanwhile, consumer confidence data from the University of Michigan is showing similar results.

Although confidence isn’t quite as high as it was when George Bush, Clinton, or Reagan got elected, these numbers show that the American consumer is generally feeling good about the economy, and the current readings are much higher than when Barack Obama was reelected four years ago.

Manufacturing Looks Strong

Back in 2011, blogger and statistician Nate Silver published a study on which economic indicators correlate strongly with presidential election outcomes. His finding: The best predictor of whether or not an incumbent party would retain the White House was strength in the manufacturing sector, as measured by growth in the Institutes for Supply Management manufacturing index from January to September in that election year. Since January, the ISM has risen 5 points, which, if Silver’s model, is correct, translates into a health Clinton victory.

Job Growth Continues to Impress

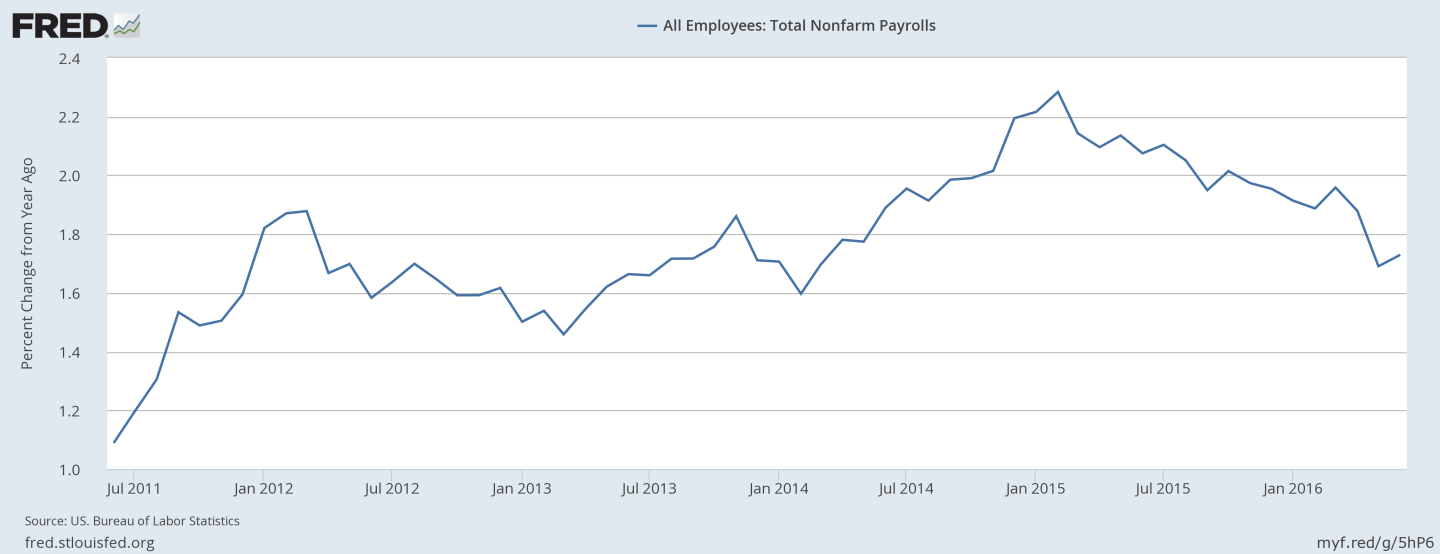

The second most important variable, according to Silver’s analysis, is annualized job growth from the first to third quarter in an election year. We don’t know what job growth will look like in third quarter just yet, but so far it looks strong, and we’ve seen annualized job growth of between 1.7% and 2.3% over the past year. If this trend continues that would be enough to give Clinton a slim margin of victory in the fall, according to this analysis.

There are, of course, other factors at play that will determine the winner of the fall election. But the economic data at least, continues to work in Clinton’s favor.