The multi-trillion dollar question, literally, for investors these days is, “How poorly is the Chinese economy performing?”

The globe’s second largest economy has been a driving factor in the weak performance of U.S. stock markets lately, as investors fear a so-called hard landing in China could drag the rest of the world into recession.

But the official Chinese economic data is notoriously unreliable. Even if we trust the numbers, we’re faced with the problem of how to interpret them. What’s more, there has never been an economy as important to the globe as China’s that has had a government so willing to use its extraordinary power to prop up economic growth.

In other words, understanding how the Chinese economy will affect the West requires that we correctly predict how the Chinese government will behave in the weeks and months ahead. To that end Deutsche Bank analysts Zhiwei Zhang and Li Zeng recently published a report called “Understanding the Tail Risks in China,” which looked at the regional policy response of the Chinese government to a slowing economy.

Zhang and Zeng isolate data from China’s northeast, a region that’s likely already in a deep recession. That segment of the country’s nominal GDP grew just 1% (factoring in inflation it would have been negative) in 2015, according to Deutsche Bank estimates. At the same time, fixed asset investment fell 11.6%, compared with an average growth of 25.5% in the ten years before. The region is dominated by state-owned enterprises involved in traditional heavy industries, or commodity and energy production, sectors that have come under particular stress in recent years.

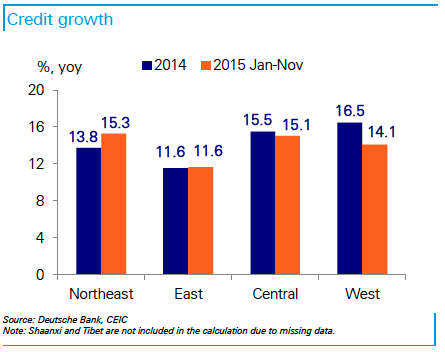

Despite this sharp drop off in economic activity, the growth in consumer spending and income did not fall anywhere near as much. Furthermore, northeast China was the only region in the country that saw credit growth, i.e., banks making more loans in 2015 than they did the year before.

In economies not dominated by the Chinese Communist Party, stuff like this doesn’t happen. As Zhang and Zeng argue that the discrepancy between the huge drop off in business activity and consumer behavior is likely the result of direct central government support, but also “indirect support,” from the folks in Beijing. They write:

The sharp contrast between weak economic activities and strong credit growth shows that banks in the northeast likely supported, through renewed lending, the weak corporate sector regardless of economic viability, which helped to avoid unemployment and bankruptcy. In this case, it is the government’s priority of maintaining social stability that overrode profitability considerations.

Such government support, however, can only be a short-term remedy rather than long-term solution to the structural challenges facing the northeastern region, and it comes with dear efficiency costs. The central government started to talk openly about addressing the risk of “zombie companies” in late 2015. This is regarded as a key part of the “supply side reforms.” One way to judge how serious the government is about the “supply side reforms” is perhaps to see if such credit support to the northeastern region will be contained in 2016.

This is another reason why western observers seem so confused by what they’re seeing out of China. Because the government there has so much more ability and willingness to stimulate the economy than governments in the West do, it’s that much more difficult to predict China’s future performance.

But until China addresses the fundamental flaws in its economy, i.e. it’s over reliance on investment, exports, and debt, it will have to continue to rely on government stimulus to avoid a collapse in employment and the social unrest that would likely be the result. And the longer it does that, the greater the growing imbalances in its economy will get.