In the original Star Wars movie, the Force is described by Jedi Master Obi-Wan Kenobi as an “energy field created by all living things. It surrounds us, penetrates us, and binds the galaxy together.”

Another characteristic of the Force: It seems to pry open parental wallets.

Star Wars: The Force Awakens, the latest installment of the megafranchise, premieres Dec. 18, right in the heart of holiday toy-buying season—and long after Star Wars merchandise hits the stores. The resulting shopping bonanza is expected to generate more than $375 million in sales this year alone for Hasbro, the toy giant with rights to most of the Star Wars products now invading shelf space like, well, Imperial Stormtroopers.

The Jedi holiday jolt, in turn, will cap what’s likely to be the toy industry’s best year in over a decade, according to Juli Lennett, senior vice president at research shop NPD Group’s U.S. toys division. NPD forecasts 6.2% growth this year over last, with U.S. sales nearing $20 billion. Among the big sales gainers through the first half of the year: games and puzzles (up 13%), action figures (8%), and dolls (8%). “It’s not just a strong year. It’s a great year,” says Lennett.

Still, many investors remain leery of the toy industry, and justifiably so. Publicly traded, pure-play toy companies are relatively few and relatively small—and since kids are famously fickle in deciding the next big thing in the school yard, toymakers’ revenue and stock prices can be volatile. That said, some analysts and money managers think this year’s toy-sales surge will continue—and that the stocks of some of the big names in the industry have more room to rise.

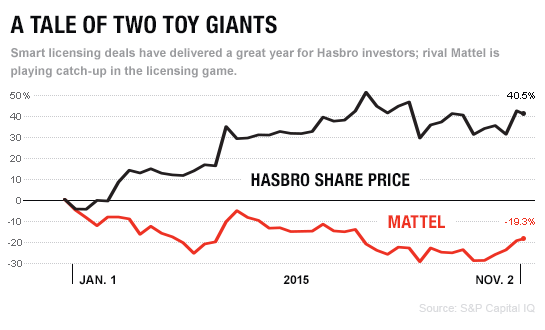

One of the prime beneficiaries of this year’s boom, of course, is Hasbro (HAS), whose stock has already risen significantly thanks to Star Wars fever (see chart). Years ago, Hasbro bet that a “content driven” business model—selling more toys under licensing agreements with popular movie and TV franchises, from Jurassic World to Marvel’s Spider-Man—would bear the most fruit, says Stephanie Wissink, a managing director at Piper Jaffray.

Now that bet is paying off. “Hasbro has been beating [earnings forecasts], capturing licenses away from Mattel, and getting in deeper with Disney,” says Wissink. “They just have huge velocity right now.” Wall Street expects that momentum to carry into 2016, producing earnings of about $4 per share, up 16% from 2015, according to consensus analyst estimates.

Hasbro’s story line has contrasted sharply with that of Mattel (MAT), the other industry behemoth, whose stock investors have beaten like a tomato can in recent years. The stock is down 19% this year, as Mattel’s stodgy reliance on fading franchises like Barbie and Hot Wheels has stung its sales. Still, Mattel retains considerable size and clout: Its revenue, expected to be $5.6 billion this year, is about 30% greater than Hasbro’s. And a recent strategy pivot that has freshened its product line, including a limited run of dolls in the image of pop star and Disney Channel regular Zendaya, has some investors seeing Mattel as an intriguing recovery candidate.

Linda Bolton Weiser, a research analyst at investment bank B. Riley & Co., upgraded Mattel to a buy after it named Christopher Sinclair permanent CEO in April. She anticipates a strong rebound next year, driven by lines like DC Super Hero Girls action figures (a venture with DC Comics) and a new license for Teenage Mutant Ninja Turtles merchandise. Her price target for the stock: $31, up more than 20% from current levels. Weiser also likes Mattel’s dividend, currently 6.1%, which the company has increased in recent years; she says Mattel has the cash flow to support the payout even if sales ebb. “For income investors like retirees, the stock is looking very attractive,” she says.

Another potential play for investors willing to take a risk on a small-cap: Jakks Pacific (JAKK), a Japanese toymaker that trades on the Nasdaq. A hefty 70% of its sales derive from licenses—industrywide, that figure is about 30%, according to NPD—with partners including Nickelodeon, DC Comics, and Saban’s Power Rangers. That heavy reliance on licenses, which can eventually expire or be transferred, means the stock carries greater long-term risk than those of competitors. The upside: Jakks trades at roughly a 50% discount to its peers.

The bumpy rides associated with smallish toy companies and their stocks may be more than some investors can tolerate. Those who want the smoother journey associated with megacap companies could play the toy market by investing in a company that collects royalties from many other toymakers’ licenses—namely, the almighty Disney (DIS). (For a closer look at the pros and cons of investing in Disney, see the next article.)

Ultimately, any investment in toys is an expression of faith in the first law of parental dynamics: People will continue to have babies, those babies will grow into toddlers, and those toddlers will throw tantrums to acquire the latest shiny thing they spot on store shelves. “There is an argument out there that kids are going to turn to mobile devices and never play with toys again,” says Piper Jaffray’s Wissink. “That is just not going to happen.”

A version of this article appears in the December 1, 2015 issue of Fortune with the headline “Toy Story.”