China’s stock market bubble–sorry, rally–is back in ‘greed’ mode again Monday after barely a week of ‘fear’, after the central bank cut official interest rates again at the weekend for the third time in six months.

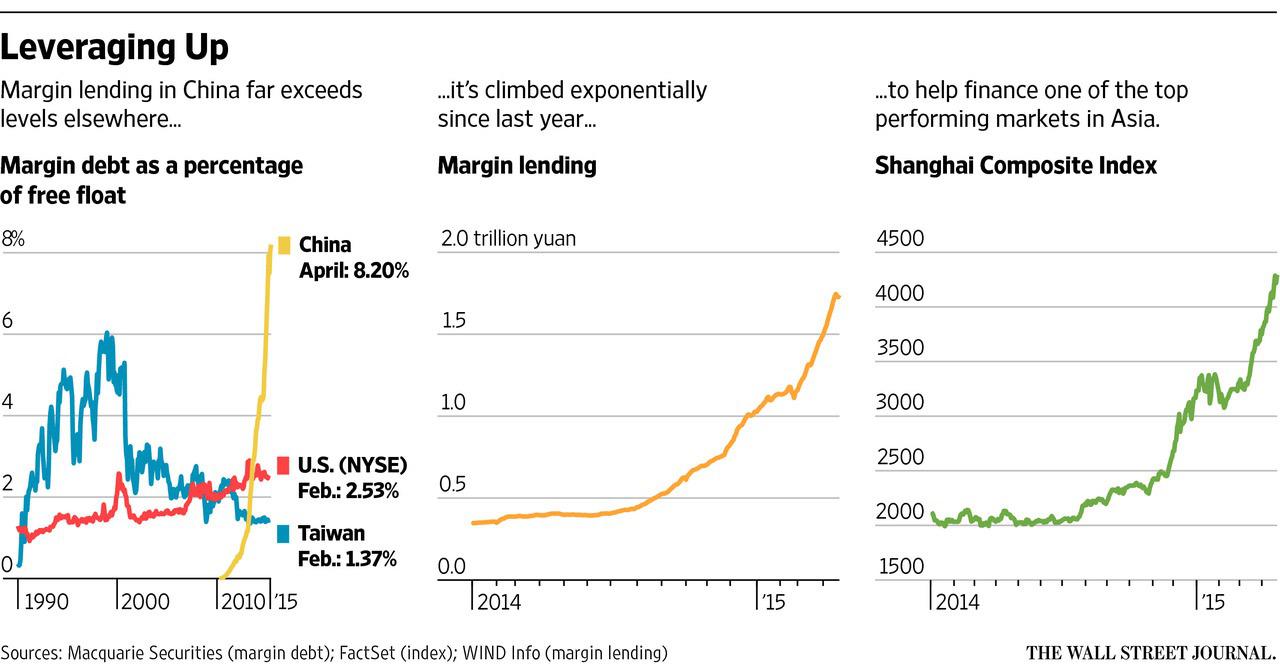

The Shanghai Composite index, closed up 0ver 3%, bringing its year-to-date gains to 34%. It has more than doubled in the last 10 months, with a big increase in hot money flows from retail investors and a parallel rise in buying financed by “margin loans,” through which brokerages lend stock buyers a multiple of their own capital. Macquarie Securities Group reckons that margin-based buying is over three times as high as it was on the New York Stock Exchange during either the tech or sub-prime bubbles.

The stock market has levered up as the authorities try to come to grips with a slowing economy, a deflating housing bubble and a mountain of local government debt (read more on the last of those here).

The People’s Bank of China’s move comes after data showing that manufacturing activity fell at its fastest rate in over a year in April, while deflation pressures show no signs of letting up: consumer price inflation at 1.5% was only half the targeted rate, while the producer price index (PPI) fell 4.6% on the year to March.

“The pace of monetary easing is accelerating, said HSBC analyst Simon Fang, noting that this announcement came only 20 days after the PBoC cut the reserve requirement by 1 percentage point April 20.

Analysts at ANZ Bank said they expect more easing to come, as growth is likely to fall below Beijing’s targeted rate of 7.0% in the second quarter.

The PBoC has many ways to cut funding costs for banks and businesses; the reserve requirement has traditionally been the most important, but official interest rates are starting to give more important and reliable signals now that the PBoC is liberalizing the rates that banks can set on loans and deposits. At the weekend, in addition to cutting its benchmark deposit and lending rates by 0.25% each, it said banks would now be allowed to charge up to 1.50% more on one-year deposits than its benchmark rate, up from a maximum of 1.30% previously.

Analysts point out that previous action by the PBoC has done less for the economy than it has for the stock market. If it really wants to help business, it’s going to have to up its game. Weighted average interest rates to business hardly fell in the first quarter, sticking at 6.56%. With an annual PPI of -4.6%, it’s getting harder, not easier, to service corporate debt.

One other effect of the PBoC’s move will be to incentivize banks to participate in a program aimed at reducing the debt burden of local governments, many of which have overstretched themselves in the pursuit of ambitious growth targets.

The central government in Beijing is offering banks the chance to swap up to 1 trillion yuan ($161 billion) of local government bonds and loans they hold for better-quality debt from the central government. However, the take-up has been slow due to the comparatively low returns offered by Beijing.