Deutsche Bank AG (DB) is paying a heavy price for its refusal to realize how much the 2008 crisis had changed its world. The only question is whether the price ($2.52 billion) is high enough.

It’s not the fact that Deutsche allegedly rigged the world’s most important benchmark interest rates (LIBOR and Euribor) that catches the eye Thursday. That’s a familiar narrative from the five other banks that have been brought to book since 2012. It’s not even the ineptitude of the bank’s internal controls, born of a basic inability to accept that what its employees were doing was wrong (see this from the DoJ’s summary):

No, what stands out is the staggering scale of the deceit and obfuscation by Germany’s largest and most prestigious bank as regulators tried to get to the bottom of the scandal.

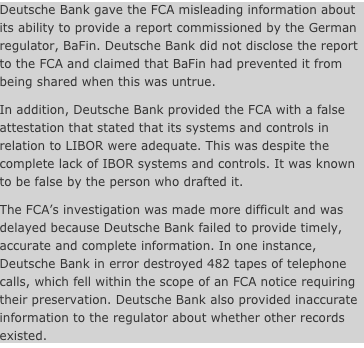

Consider this from the U.K.’s Financial Conduct Authority. Count, if you please, the repeated attempts to deceive and obstruct the regulator in its duty, and note that this relates to a period between February 2011 and July 2014, well after even the most defiant bankers had started to admit that rigging the world’s most important interest rates might have been a little bit naughty:

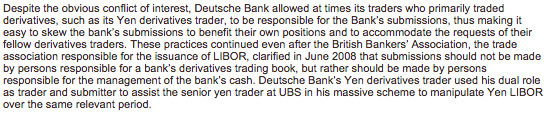

Or consider this, from the Commodities and Futures Trading Commission:

That’s right: from 2008, when the body responsible for the calculation of London Interbank Offered Rates started to address the most egregious conflicts of interest, right through to mid-2011, Deutsche was, to say the least, slow to acknowledge that cheating its customers was wrong, or that regulators had a right to know how bad it had been.

The comparison is instructive: U.K.-based Barclays Plc (BCS) having seen which way the wind was blowing, cooperated, settled early and received a relatively light $450 million fine. But it cost the head of both Bob Diamond, the bank’s chief executive, and Marcus Agius, its chairman.

By contrast, Deutsche is paying more than five times Barclays’ fine, but there’s no certainty of consequences for top management.

Deutsche was at pains to point out in a statement Thursday that: “No current or former member of the Management Board was found to have been involved in or aware of the trader misconduct.” (The same is true for the other alleged Libor riggers — there are no criminal charges outstanding against anyone above middle management level.)

Co-CEOs Anshu Jain (head of Global Markets while the worst of the manipulation was said to be going on) and Jürgen Fitschen (who is already facing criminal charges for obstructing justice in a separate case) said they “deeply regret this matter but are pleased to have resolved it.”

The fact that the CFTC started to find Deutsche more cooperative from mid-2011, immediately after Jain and Fitschen became co-CEOs, speaks in their favor, but any credit they take damns their predecessor, Josef Ackermann, by implication. Either this was in the power of CEOs to influence or it wasn’t. In any case, the FCA’s complaints refer to a period between February 2011 and May 2014 (a spokeswoman declined to be more precise). And the suspicion remains that they only changed tack when the risk of being ratted out by others in the conspiracy, such as Barclays, became material.

Libor is almost certainly the biggest of the 180 regulatory investigations that Deutsche’s CFO Stefan Krause said the bank was facing a year ago. Assuming Jain and Fitschen ride out any storm at the annual shareholder meeting next month, they’re likely to get the chance to tackle the next big challenge: deciding what kind of bank Deutsche is going to be in future.

[fortune-brightcove videoid=4082776937001]

A strategy document unveiled in March laid out three options: to stay a universal bank in the style of JP Morgan Chase (JPM), or to spin off either part or all of the retail banking operations. The Wall Street Journal reported last week that it’s inclined to take the middle way, spinning off Deutsche Postbank, a dull but largely scandal-free German retail bank that provided some welcome balance sheet ballast during the crisis, but which dented overall profitability.

The bank’s regulators might wish that the Deutsche that survives can become as boringly clean as Postbank. Certainly, having a DoJ monitor installed in the U.S. office for the next three years should help ease some of the Fed’s concerns about its governance. But the findings of the Libor probe still leave plenty of room for doubt about the bank’s willingness and ability to change the culture that brought it to where it is today.