Beach reading for Todd Ahlsten this summer will once again be The Black Swan—same as always. The chief investment officer of Parnassus Investments, which oversees $11.5 billion, doesn’t go on vacation without his well-read copy of Nassim Nicholas Taleb’s 2007 book, which warns that we can never predict world- changing (or market-crashing) events. “It drives my wife crazy,” says Ahlsten, 42. “If that makes me a pessimist, well, I guess I’m a realist.”

Ahlsten’s defense-first approach has worked spectacularly well over the long haul: His Parnassus Core Equity Fund has grown from $55 million in assets when he took over in 2001 to $9.3 billion. Though it lags the S&P 500 slightly over the past five bull-market years, the fund is No. 1 in its category in 10-year return, according to Morningstar, returning 10.3% annually, vs. 7.8% for the S&P 500. When Ahlsten commits to a stock, it’s often for the very long run. For instance, he still owns Energen and WD-40, both of which the fund bought in the ’90s when Ahlsten was a young analyst at San Francisco–based Parnassus. Fortune asked him where he’s finding value now. Edited excerpts:

Why do you focus so much on “black swan” scenarios—are you sure you’re not a pessimist?

I’m definitely not a pessimist. I’m not making a macro call that I think something’s imminent; I just don’t like to forget those issues. We spend a lot of time looking at the downside, stress-testing companies for being in a recession. When we talk to management, we like to ask them about 2008 and 2009, what they learned—just to make sure they haven’t forgotten about letting more risk creep into their businesses.

We talk about it every day, think about it, meditate about it on a yoga mat. The key is to get comfortable with the downside and really have a portfolio with defensive characteristics. My personal equity exposure is 99% in my fund, plus I own a small amount of Berkshire Hathaway so I can go to the annual meeting. I think of myself as a client. We can still participate in bull markets, though we may not be a top 10% performer.

You didn’t buy or sell anything in the first quarter of 2014. Why?

The first quarter was unusual; we don’t normally see 0% turnover. But the stock market was only up slightly, and valuations just didn’t change on our watch list. If stocks weren’t ready to be in the portfolio in fourth quarter 2013, they weren’t ready in first quarter 2014. But we were, and are, still looking at new ideas as aggressively as ever. I’ve flown over a million miles to talk to management teams, and a lot of those visits I’ve had hardhats and goggles on or a fire suit. I like to see the offices, and not just the C-suite, but what’s the vibe of the receptionist? When the CEO is walking down the hallway with a cup of coffee, do people say “Hi” to him?

So which companies do you find most intriguing now?

I recently had breakfast with the CEO of Praxair, one position we increased last quarter. They’re in the industrial gas business, which is a real megatrend: Industrial gases are used in making solar panels, health care, and other things that really help our environmental footprint go down. We also added to our position in Patterson Cos., a dental-equipment provider. When I was getting my teeth cleaned last week—no cavities—I asked my dentist, “What’s the new technology?”

Do you ask questions like that everywhere you go?

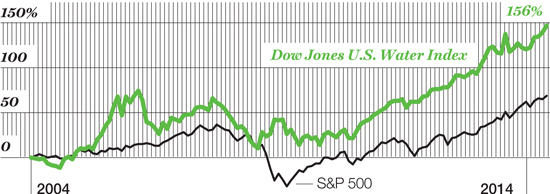

Sure. I’m also spending a lot of time at water conventions and conferences, learning a lot about the water system and the technology that goes into dealing with wastewater. We think water is a huge trend long-term. Not only is it scarce and we need to upgrade water supply, but also old pumps use a tremendous amount of electricity. Two of our top holdings are Pentair and Xylem. These companies treat, transport, filter, store, monitor, and distribute water for municipal and industrial applications. Their pumps, valves, and sensors make companies better at using water, recycling it, and putting it back into the aquifers. Xylem has been replacing old pumps in China, for example, with ones that are twice as energy efficient. You can see the enormity of the issue. If you’re a Big Pharma company or, say, PepsiCo, which we also own, you are going to have to invest more in water. Pepsi has been doing a lot of pretty progressive stuff in India to put water back into supply.

Rising Tide: As the value of water increases, stocks of water-services companies are rising.

One of your top holdings is Allergan, which you bought just a few months before Valeant and activist hedge fund manager Bill Ackman announced their takeover bid for the pharmaceutical company. What’s your take on it?

There’s only so much I can say about Allergan. We did an encyclopedic amount of work on it and started buying the stock in late fall 2013. We’ve been down to the headquarters at least twice. Between its dermatology business, with Botox, and the eye business, Allergan has great long-term demographics, and we really like the relevancy of the products; the moat is great. When we started buying stock in the $90 range, the risk/return profile was fantastic. Now fast-forward: Other people realized it was fantastic [it traded around $170 recently], and Valeant has publicly talked about aggressive cuts and taking the tax base down abroad. [For more on tax inversions, read here.] Fundamentally, though, we think Allergan is a very, very valuable company.

This story is from the July 21, 2014 issue of Fortune.