The Commerce Department recently revised its estimate of U.S. economic growth, announcing that the economy actually shrank at a 2.9% annualized rate in the first quarter of this year.

This news comes in stark contrast to what most economic forecasters were predicting, including the Federal Reserve, which had expected the economy to grow at 3% rate for the year. Now, the Fed is forecasting growth between 2.1% and 2.3%.

Of course, the Fed has consistently overestimated U.S. economic growth since the end of the financial crisis, and four years after the end of the recession, we have yet to achieve the sort of above-trend “catch-up” growth that economies tend to experience following a contraction.

So, why exactly should we expect the economy to now kick into higher gear? Earlier today, I offered the case for why the economy really is about to turn around, but that’s not the whole story. Here are four reasons why we shouldn’t be so optimistic:

1. The plight of young America: America’s 23-year-olds constitute the nation’s largest single age group. This should be great news for the economy, as young folks just entering the workforce could serve as a great engine for economic growth going forward. The only problem is that this age group is saddled with unprecedented educational debt and a job market offering fewer opportunities than were presented to preceding generations.

While it might be true that the six-figure debt often discussed in the media is quite rare, and that the student loan problem isn’t a bubble like housing, the exploding cost of education is going be a drain on the economy in some way, shape, or form.

This debt is likely showing itself in the fact that first-time homebuyers are making up a historically low number of all home purchases. And if students aren’t indebted, that’s only because their parents are sacrificing purchases they would have made in order to finance their children’s education. In other words, somebody has to pay the piper when it comes to skyrocketing education costs.

2. Household formation has stopped short: The exploding cost and lack of funding for education is also likely affecting the pace of household formation. A household is formed, for instance, when a child moves out on his own for the first time and rents an apartment or buys a home. This sort of activity is very important for economic growth because a new person or family striking out on his or its own leads to all sorts of subsequent activity, like home building and the purchase of furniture or appliances.

Household formation completely fell off a cliff during the crisis, and there’s no sign of a coming recovery.

3. Our cities can’t grow: Household formation may be sluggish because young people can’t afford to move to the most economically vibrant parts of the country, the kinds of spots where there are high-paying jobs with room for growth. Jed Kolko, chief economist at Trulia, recently compiled a list of the fastest growing cities for Millennials, and only two of those cities (Oakland and Honolulu) are also ranked among the 10 metro areas offering the highest pay.

This was not the case for most of American history. It used to be that the fastest growing cities were also the most economically vibrant, but the growth of exclusionary zoning laws starting in the 1970s in America’s biggest cities and surrounding suburbs has stopped the growth of those regions, and has likely held back economic growth as a result.

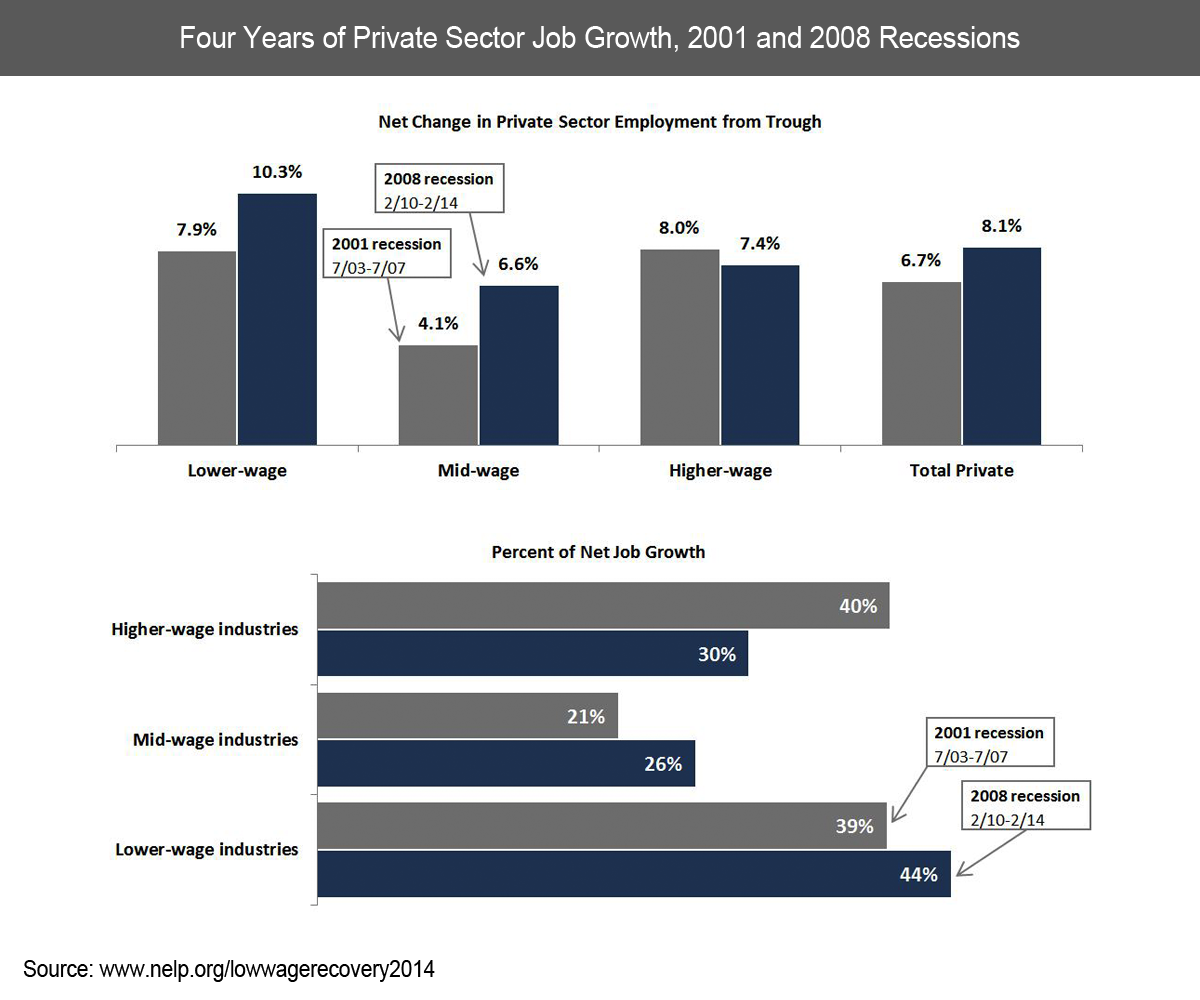

4. The jobs we’re creating aren’t any good: Though the unemployment rate has come down and even median pay has begun to increase slightly, we’ve replaced a lot of middle-income jobs with low-paying ones. The U.S. economic recovery has been fueled by low-paying sectors like retail and food services. If this trend continues, there will be little reason to expect a sustained increase in median pay. And if the average person can’t afford to spend more, there’s little hope for a significant period of above-trend economic growth: