Jeffrey Bussgang is general partner at venture capital firm Flybridge Capital Partners.

Mary Meeker’s periodic review of the Internet industry is always a must-read presentation. This year was no exception – chock full of data, insights and thought-provoking charts.

There is a theme that Mary espoused that I have become a big fan of ever since I read Marc Andresseen’s article in the Wall Street Journal “Why software is eating the world“. She framed it as the “re-imagination of nearly everything”. The simple notion is that the confluence of broadband, mobile and globalization in combination with Moore’s Law have allowed the technology industry to innovate almost everything in existence. Facebook’s IPO brought their “hack” culture to the forefront of the world’s conscience. Well it turns out, technologists are hacking everything – from advertising to media, from retail to health care, from education to banking.

Ah, banking. This has not been a good few weeks for the banking industry. The surprise $2 billion trading loss at JP Morgan Chase has caused erstwhile superhero Jamie Dimon to appear fallable. Many are pointing out that the crisis at JP Morgan is an example of a banking sector that is increasingly concetrated in the hands of a few and results in a systemic risk because the top 5 banks are simply “too big to fail”.

I would argue, there is an even larger risk for the financial services industry, that in turn provides a larger opportunity. I think banks are now simply too big to innovate.

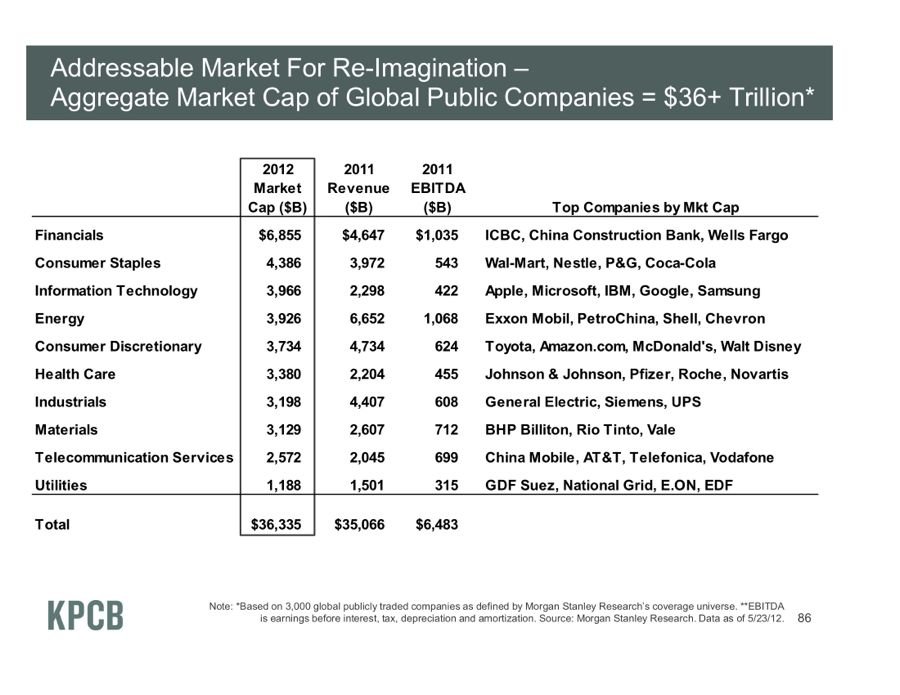

Let’s look at Meeker’s slide 86 below:

She lists the industries that are ripe for “re-invention” sorted by their 2012 market capitalization. Financials are on top at a leviathan-like $7 trillion. There are 200,000 employees at JP Morgan Chase and Bank of America each and 350,000 at Citigroup. Structurally speaking, these organizations are simpy too large to develop breakthrough, out-of-the-box, re-invent banking solutions. That opportunity is left to entrepreneurs.

As a result, there are a slew of start-ups “hacking” banking. We have invested in a number of them that are hacking away at pieces of the financial system. ZestCash is hacking consumer lending. SimpleTuition is hacking student loans and banking. Cartera Commerce is hacking credit card marketing. AccountNow is hacking checking accounts and debit cards. Plastiq will soon be hacking large ticket purchasing. There are hundreds, if not thousands, of others that other investors have backed as well.

So when I look at the innovative progress being made in payments, mobile banking and other major areas, it makes me smile. Because while the major titans in the industry are caught up in looking backwards, the entrepreneurs are re-inventing the future of finance. That’s an exciting prospect.