Additional reporting by Scott DeCarlo

In a year full of the usual uncertainty and surprises in the stock market, one particularly unusual trend stands out. The stocks with the highest concentrations of hedge fund ownership have become some of the market’s biggest losers. That underperformance has a lot to do with the kinds of companies that hedge funds prefer to own (think fast-growing, but volatile). You can read more about them in Fortune’s feature, “When Hedge Funds Are Toxic for Stocks.”

But the trend also points to an opportunity for individual investors. The stocks least owned by hedge funds just turned in their strongest six-month returns since 2008. More important, these stocks have some features in common that long-term investors cherish. They tend to be larger companies by market value, and compared to the hedge-fund favorites, they have less debt, grow earnings more slowly but consistently, and pay bigger dividends. Here, we found six stocks that fit that mold, and should be worth owning regardless of what the “hedge-fund hotels” do down the line.

1 / Oracle

With the second-lowest hedge fund ownership in the S&P 500 (0.6% of its shares, just behind CMS Energy (CMS)), Oracle (ORCL) has been ignored by the activists and their ilk—and several top money managers would just as soon have it stay that way. Oracle is trading at 14 times its next 12 months of earnings—a fraction of the valuation of many of its Silicon Valley peers. (The S&P 500 Information Technology Sector Index has a forward P/E of 16.) Investors have worried that Oracle will have a hard time catching up with Salesforce’s (CRM) cloud business, says Bob Olstein, whose Olstein Funds manage about $900 million. Yet Oracle’s cloud revenue has grown 41% annually for the past five years, almost twice as fast as rival Salesforce’s cloud (and total) revenue has grown.

Oracle’s sales skipped a beat last year as it more aggressively transitioned from selling licenses of its database software to selling subscriptions to its Internet-based cloud product. But that changes later this year, says Dan Davidowitz, who oversees $9 billion as the chief investment officer of Polen Capital: As Oracle’s cloud business begins to hit its stride, its earnings will grow at least 10% annually over the next five years, he predicts. Oracle’s Fortune 500 business customers tend to stick with what they’ve got for a while: “Nobody leaves Oracle, ever,” Davidowitz says. While Amazon (AMZN) launched a competing service earlier this year, Oracle’s corporate offerings are more robust, says Olstein: “Amazon is basically a storage company up in the cloud. [Oracle] is solving your problems.” Oh, and Oracle offers something Amazon doesn’t: a dividend, yielding 1.5%.

2 / UnitedHealth Group

Though it’s the biggest U.S. health insurer, UnitedHealth’s (UNH) insurance business isn’t what excites investors about the stock (investors other than hedge fund managers, who own about 1%). The company’s short foray into the Affordable Care Act’s public marketplace was largely a mistake; UnitedHealth says it will drop most of its Obamacare plans, which have cost it millions in losses. But investors are treating United’s cutting bait as a victory: Those 800,000 customers represented less than 2% of the insurer’s 47.7 million members, and while the company may lose revenue, it will reap an extra 5% to 6% in earnings growth “just by pulling back,” says Laton Spahr, manager of the $2 billion Oppenheimer Value Fund. Overall, Wall Street estimates that UnitedHealth’s earnings will grow 33% this year, nearly five times what it expects for the S&P 500.

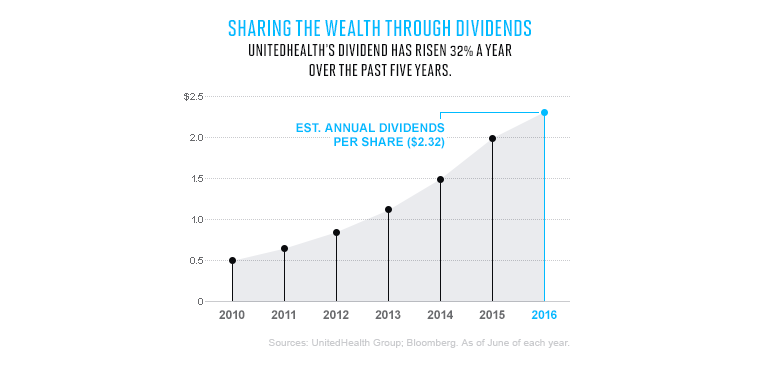

But the “jewel within the company,” according to Mark Henneman, manager of the top-performing Mairs & Power Growth Fund, is its health care analytics unit, Optum. With Optum’s database of medical treatments, prices, and success metrics, UnitedHealth is using the unit internally to reduce costs and also selling its services to other companies and organizations. Optum enjoys higher margins than insurance too: Its consulting unit, OptumInsight, makes up less than 4% of the company’s overall revenue but about 12% of its operating profits. Five to seven years from now, Spahr believes, UnitedHealth will be more a technology company than an insurance company. In the meantime, investors can collect its dividend, which has grown an average of 32% annually for the past five years.

3 / 3M

It’s not hard to surmise why hedge funds have largely ignored 3M (MMM): It’s the opposite of a momentum stock. It grows slowly, though steadily (averaging more than 6% earnings-per-share growth for the last decade), and has been managed so methodically from one CEO to the next that it has paid out a dividend every year for the past 99—and increased that dividend annually for the past 58. “It’s part of what we think makes up a quality business and therefore makes it so we can remain patient with them,” says Eric Schoenstein, manager of the $5 billion Jensen Quality Growth Fund, which invests only in companies that have returned at least 15% on equity every year for the past decade.

Hedge funds aren’t exactly known for their patience, which 3M has required a bit more of lately. Less than half of the company’s revenue—on everything from Post-its to odds and ends such as Ace bandages, road signs, and LCD touchscreens—comes from the U.S., and the strong dollar shaved 3% off its revenue in the first quarter alone. But 3M’s geographic and product diversification should work in its investors’ favor over the long term, and already the currency headwind is abating, Schoenstein says, adding, “You’re talking about a company that’s selling thousands of different products in about 200 countries.”

Though 3M’s stock has risen recently as investors have turned from momentum companies to less volatile stalwarts—it’s up 12% year to date—its P/E valuation is only slightly higher than the market average, and it has a nearly 3% dividend yield. Wall Street expects its earnings to grow 7% to 9% annually over the next few years.

4 / United Technologies

United Technologies’ (UTX) refusal in February to entertain Honeywell’s (HON) takeover proposal might seem like the kind of move to attract an activist hedge fund manager. But as Edward Jones’s Kate Warne points out, the aerospace manufacturer and defense contractor, less than 2% of which is owned by hedge funds, has already been doing things that hedge funds frequently recommend.

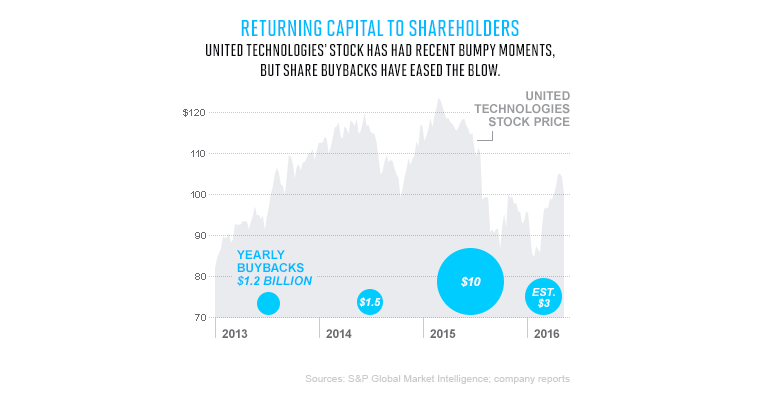

Last year the company sold its Sikorsky Aircraft helicopter business, which makes Black Hawk military choppers, for $9 billion in cash. It used the money to buy back stock, making up for the earnings hit it took by divesting the subsidiary. Still, the stock trades at about 15 times expected 2016 earnings, compared with 17 for the S&P 500. That’s why Honeywell came knocking, Warne believes, and why United Technologies rebuffed the offer as too low. The company has plenty of room to grow on its own, with brand-name products—including Otis elevators (the world’s tallest building, the Burj Khalifa in Dubai, has 57 of them) and Pratt & Whitney plane engines—as well as cameras and sensors for unmanned aircraft (a.k.a. drones). Warne expects United Technologies’ earnings to grow an average of 9% over the next few years, and it is aggressively returning capital to shareholders. It has a dividend yield of nearly 3%, and last October it announced a plan to buy back a total of $12 billion in shares by the end of 2017. Analysts expect the stock to return 10% to 20% in the next year, including dividends.

5 / Ecolab

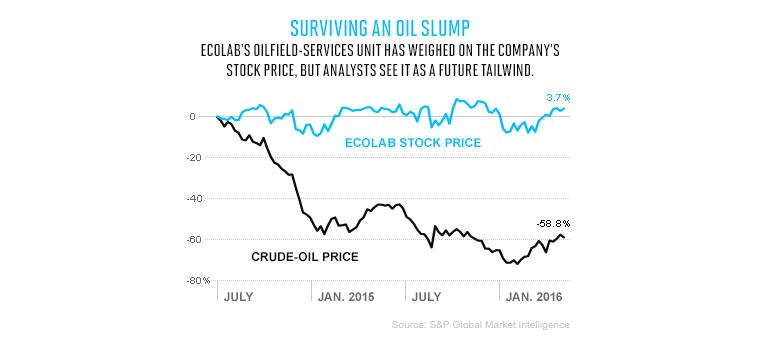

Trading at 26 times earnings, Ecolab (ECL) isn’t cheap, but the quality of its business, combined with the fact that the stock has been beaten up lately, has created a window to buy it when it’s poised to bounce back. Ecolab makes cleaning supplies and industrial chemicals for restaurants and hotels and also provides oilfield services—a business that has suffered recently because of low energy prices. But Ecolab’s chemistry technology, which allows customers to use less water and energy and recycle their waste better, has been especially attractive at a time when beleaguered oil and gas producers are looking to maximize efficiency any way they can. (It’s also easier on the environment.) “We think their oil and gas business will remain under pressure for a while, but it will be a tailwind too,” says Henneman.

Rather than cut back on its energy investments as its competitors have, Ecolab has used the industry’s distress as an opportunity to scoop up market share from rivals, including Halliburton (HAL) and Baker Hughes (BHI), which have been struggling even more, Henneman says. While Ecolab’s revenue is expected to decline slightly this year and its earnings are expected to inch up 2%, much of that is a result of currency headwinds: Excluding the foreign-exchange issues, Henneman expects its earnings to grow 11% to 12% over the next few years, as free cash flow increases and margins improve further. Plus, Ecolab has paid a dividend since 1978 and has increased it annually since 1993, averaging 17% growth for the past three years.

6 / ADP

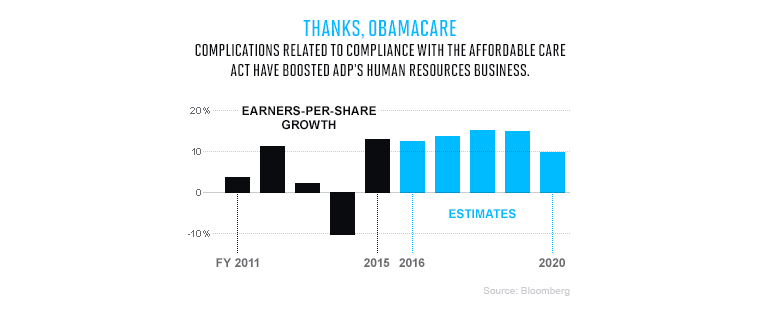

Polen Capital’s Davidowitz calls ADP (ADP) one of his “safeties,” but that doesn’t mean he’s sacrificing growth, he says: He expects ADP to grow its earnings per share (EPS) 10% to 13% annually over the next five years. Handling payroll and other human resources functions for employers, ADP is benefiting from the way the Affordable Care Act has complicated those tasks. As more employers decide that’s too big a job to handle internally, ADP is “constantly adding new customers and constantly adding more employees from their existing customers,” Davidowitz says.

ADP is another company making moves that hedge funds sometimes demand, without their being involved. (Hedge funds own 1% of ADP.) For example, the company spun out its slower-growing car-dealership-software business, CDK Global, in 2014, allowing ADP to better focus on its core businesses, Davidowitz says.

One of ADP’s biggest challenges in recent years may also be starting to abate: low interest rates. As ADP collects the taxes withheld from employees’ paychecks, it also ends up sitting on a substantial sum of money, which it invests, creating a second revenue stream for the company—similar to the way Warren Buffett invests insurance premiums collected by Berkshire Hathaway (BRK-A). But ADP, which invests the float in fixed-income securities, has made a relative pittance on it for the past several years. “Even with that headwind, they’ve managed double-digit earnings growth,” Davidowitz says; if and when rates rise, the stock could have an even stronger run.

More from the Fortune Midyear Investor’s Guide:

• When Hedge Funds Are Toxic for Stocks

• Why Starbucks Is a Hedge-Fund-Proof Stock

• 3 ‘Hedge-Fund Favorite’ Stocks to Avoid

A version of this article appears in the June 1, 2016 issue of Fortune with the headline “Seven Stocks to Buy Right Now.”