Stuart Miller, the executive chairman of Lennar, was trying to invent the “Home of the Future.” It was the early 1990s, and as a young exec, he and his team spent months developing a futuristic mini-manse, filled with voice activation and other gadgets. The brainchild was splashily promoted in TV ads by Star Trek’s William Shatner, who intoned, “If you’re not living in Lennar’s Home of the Future, you’re living in the past.”

The venture was a total flop.

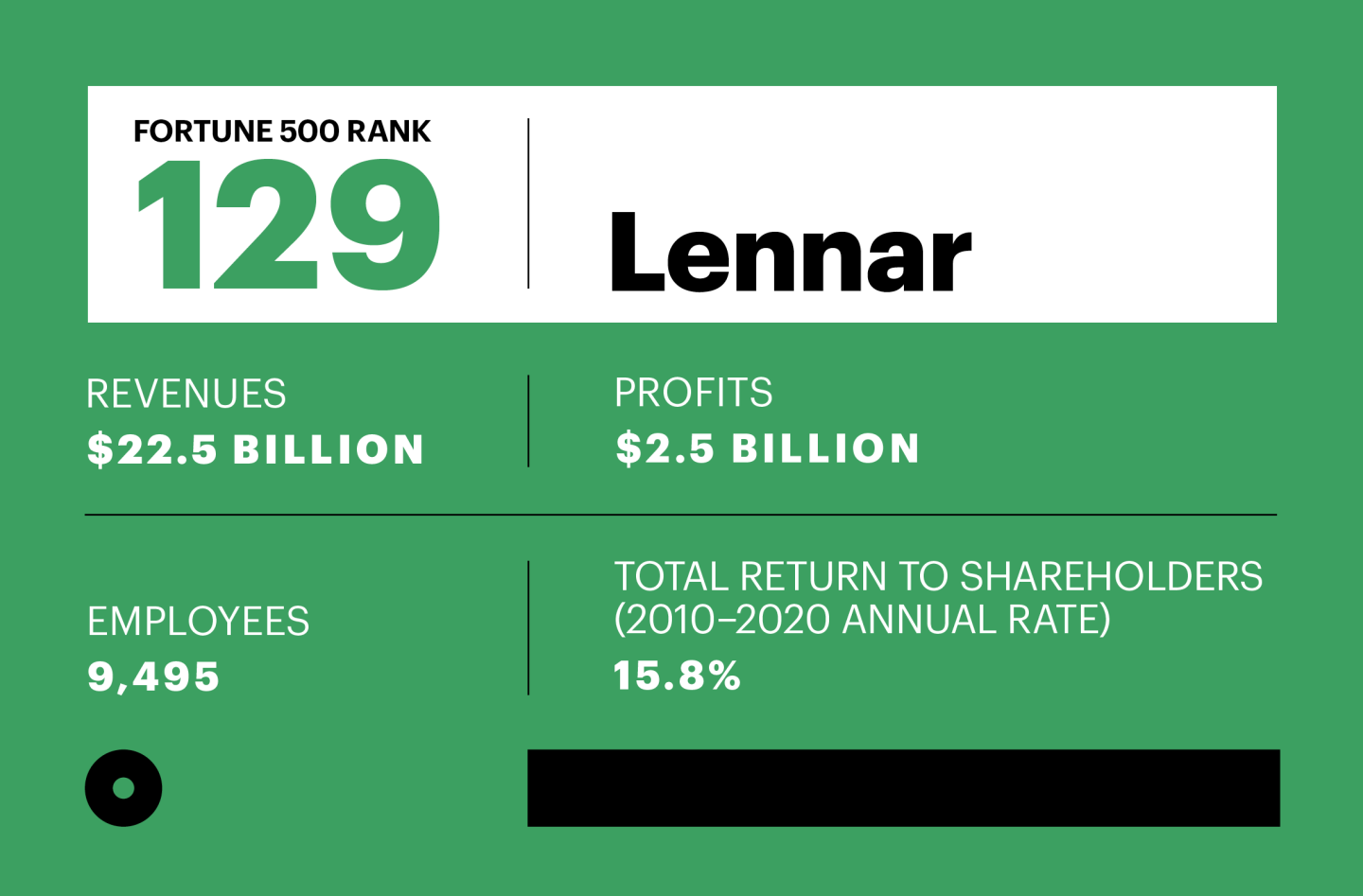

But now, nearly three decades later, America’s largest homebuilder—No. 129 on the Fortune 500 list, up 18 spots from last year—has its finger on the pulse of exactly what Americans want from the home of the future. “I went to the Lennar offices every day in a suit and tie, even in the sweltering Miami summers,” says Miller, who’s attired in a gray turtleneck. “I never used my office at home as a core part of my working life before.” Miller, a renaissance business figure who relishes bringing Silicon Valley–hatched technology to an old-line sector, spent his entire career building an enterprise cofounded by his father and rarely gives interviews. For him, as for tens of millions of Americans, the home of the future isn’t filled with futuristic gadgets, it’s a principal workplace, a gym, a homeschooling center, an entertainment hub, and refuge where everything from pandemic-ready leisure wardrobes to gourmet cuisine can be delivered to their doorstep while they spend quality time bonding instead of fighting traffic and roaming stores. “The pandemic’s rewired the way people think about their homes,” says Miller. “As a result, they’re rethinking the amount of their paycheck to spend on housing. We have a front-row seat seeing in real time the enthusiasm for the home growing.”

The sudden rage to own is boosting the fortunes of America’s $400 billion single-family homebuilding industry more than at any time since the real estate boom that ended in the Great Recession. Put simply, it’s the pandemic lifestyle that has put the juice back into what has long been a slow-moving sector. The incredible, overnight resurgence stunned even such seasoned veterans as Miller. He recalls that for a few months in the depths of the lockdown, he and co-CEOs Jon Jaffe and Rick Beckwitt didn’t know what to make of the pandemic’s impact. Initially, Miller says, they couldn’t foresee “whether people would have enough money for a down payment.” He notes that states such as California, Washington, and New York mostly banned construction, and that even in the markets that remained open, Lennar slowed to a crawl, fearing the flashing yellow light might turn red.

Instead, the strong tailwinds from 2019 into early 2020 returned, and an entirely new force entered the market: the rise of the work-from-anywhere economy. That trend added a whole new layer of demand to the robust, pre-pandemic march already underway. The capsule summary is that Lennar’s and other homebuilders’ profits are booming: Although lumber, labor, and other costs are rising fast, sales prices and volumes are jumping far faster. And Lennar believes this boom has legs.

Lennar is a different breed from a basic, sticks-and-bricks homebuilder. The builder traces its origins back to the mid-1950s when 23-year-old Leonard Miller, who started in the business counting lumber, parlayed a $10,000 commission he had received as a broker into a 42-site subdivision that he merged with a small Miami homebuilder cofounded by entrepreneur Arnold Rosen. The name Lennar is a creative fusion of “Lenn” for Leonard and “ar” for Arnold. Stuart joined the enterprise at age 12 or 13. “I was too young to handle a lawn mower, so I was assigned to the raking crew,” he recalls. Young Miller graduated to teenage laborer, and later managed work sites.

In 1971, Lennar went public at a valuation of $8.7 million. Eleven years later, Stuart joined Lennar after graduating from Harvard and the University of Miami law school. He at first shunned homebuilding “to avoid being seen as the boss’s son,” and instead went “knocking on doors” to lease commercial buildings. But the double-digit mortgage rates that hammered the industry in the 1980s handed him a big opportunity. He found creative ways to build and market homes at extremely low costs, which kept them affordable. In 1997, Miller rose to CEO, a job he held until 2018. Among his coups was buying big swaths of land on the cheap during the financial crisis of 2007–08, often at prices lower than the cost of the streets and sidewalks. Miller attributes Lennar’s current success to the “group thinking process” of his top team. The crew regularly meets several hours a day, in the office and over lunches and dinners pre-pandemic, virtually during the crisis. Miller, Jaffe, Beckwitt, along with CFO Diane Bessette and LenX head Eric Feder, “duke it out” in fierce debates that, says Miller, meld into strong lines of strategy.

These days Miller oversees LenX, which amounts to a private equity arm within Lennar that makes investments in real estate tech. The Lennar-backed platform Opendoor—which uses A.I. to value and make almost instantaneous offers on any home—went public in December, bringing Lennar a $470 million gain in its first quarter. Other LenX startups provide fully digital insurance underwriting for most Lennar buyers; are developing a digital title insurance and escrow platform; and are honing technology that conserves water and channels the earth’s energy to heat and cool homes.

I went to the Lennar offices every day in a suit and tie, even in the sweltering Miami summers. I never used my home office as a core part of my working life before.

Stuart Miller, executive chairman, Lennar

Lennar already benefits from major scale in a fragmented industry in which the top 17 builders hold just 36% of the market. Its $22.5 billion in 2020 revenues narrowly edged D.R. Horton (No. 148 on the 500 this year), the mega-rival that was first mover at the entry level, and operates mainly in the low-priced tiers where Lennar is expanding. Lennar builds in the relatively expensive Northeast markets such as Pennsylvania and New Jersey, but its sweet spot is the Sunbelt. Its largest markets are Florida (28% of sales), Texas (18%), and California (15%), and it ranks first in 20 major metros, including Phoenix, Orlando, Miami, Riverside, Las Vegas, Charlotte, and Tampa, and rates second to Texas-based D.R. Horton in Dallas, Houston, and Austin.

Fast-expanding entry-level offerings now make up 35% of homes sold by Lennar, with prices ranging from $175,000 to $250,000 in Dallas/Fort Worth to the mid-$400,000s in the Denver area. The bulk of its production remains in first-time move-up models that in the Miami area start in the mid-$300,000s. In the Galiano Pointe development 20 miles southwest of Miami, a sleek stucco model at 2,403 square feet, featuring four bedrooms, three baths, and a two-car garage, goes for $584,000.

The first quarter of 2021 illustrates the phenomenal strength of the market: In Q1, homebuilding sales rose 18.5% over the same three months last year, to $4.9 billion.

The key is that Lennar has been able to supercharge pricing power and volumes—a crucial double boost because costs of both materials and labor are rising. In the past year, the cost of lumber, which along with framing accounts for 15% of a home’s construction price, has doubled, raising the cost of Lennar’s average home by about $24,000.

Yet Lennar’s gross margins—the difference between revenue collected and the basic costs of land and construction—have skyrocketed from $849 million to $1.22 billion, a gain of 44%. It now pockets $99,200 per house versus $82,200 last year. More pricing leverage is in the cards: The average price of newly ordered homes was $420,000 in the first quarter, compared with $404,000 last year. Indeed, in a twist few could have predicted, the pandemic powerfully transformed Lennar’s profitability.

The homebuilding business is all about lead times—and Lennar, whose stock has risen 137% to $95 since the start of 2019, is reaping the fruits of a big bet placed a few years back. Following the financial crisis of 2007–08, “the entry level shut down,” recalls Beckwitt. “Lenders tightened standards so that young people couldn’t get mortgages. Instead, they were renting apartments and moving in with their parents.” By contrast, banks were much more willing to lend to folks in their late thirties and forties who had higher incomes, more assets, and were potential customers for products from credit cards to brokerage accounts.

But Miller believed that millennials would eventually buy at the same rate as their parents. “A common narrative was that millennials were going to migrate to city life, not normalize to suburban life when they married and had kids,” he says. “Our view was always that the production deficit in entry-level homes would be reversed, and that millennials would raise their families in the suburbs, that they’d want parks and backyards.” Around 2016 he saw demand building in the two markets where Lennar did do starter homes, Texas and Florida. Miller also predicted that the 2017 tax law that slashed deductions for state and local levies would cause an exodus from coastal cities to the Sunbelt. Pre-pandemic, Stuart, Jaffe, and Beckwitt were convinced that the slow but steady flow of millennials into housing would become a torrent.

Lennar’s shift down-market was part of a blueprint to hike profitability. It takes half as long to build and deliver an entry-level home that’s smaller, occupies less land, and requires lower-end siding and moldings than a roomier, fancier move-up manse. Lennar could deliver eight homes a week, say, in a starter section, at least twice the number in a move-up community. Naturally, a $400,000 home yields more dollars in profit than one fetching $250,000. But the Lennar brain trust figured that if it could sell smaller footprint starter homes at extremely high volumes and speed, it could generate much bigger revenues on the same or even lower levels of inventory of land and in-ground construction. It could free up capital from one project faster to start the next one. That game plan would generate richer margins on assets and equity.

D.R. Horton was first to wager big on the millennials’ return by launching its no-frills Express brand in 2013. But Miller still saw plenty of space for Lennar. “It was a part of the marketplace homebuilders hadn’t been building for,” he says. “The underproduction weighs more heavily on the entry-level market to this day.” In 2017, Lennar made its first major foray toward achieving the scale required to bolster its new strategy by agreeing to purchase rival CalAtlantic for $9.3 billion. The deal allowed Lennar to leapfrog D.R. Horton to become America’s biggest homebuilder. The acquisition’s goal was to greatly strengthen Lennar’s position in markets where it was already big, notably California, Florida, and Arizona. “The concept was to move CalAtlantic, which owned a lot of land, to lower price points,” says Jaffe. The deal enabled Lennar to give more work to framers, electricians, and plumbing contractors in metros where the combination commanded a much bigger market share, hence lowering labor costs. Its expanded footprint also delivered big economies of scale in purchasing everything from appliances to aluminum siding.

Lennar’s down-market move caught a rising wave. From the start of 2012 to June 2017, the combined medium-high and high-priced categories, as defined by the American Enterprise Institute’s Housing Center, rose faster than the two entry-level tiers, labeled “low and low-medium.” But in mid-2017, the formerly sluggish entry level lifted off. From then until the close of 2020, prices in low-medium, the larger swath of the starter categories, grew 18% to $252,000, while medium-high and high declined 4%. “In that period, all the growth in new home prices came in low-medium,” says Ed Pinto, director of the AEI Housing Center. The trajectory was similar in sales: The low-medium bin rose 50%, triple the combined increase in medium-high and high.

That outperformance continued until the pandemic-driven explosion starting in mid-2020. Then, a reversal occurred that Pinto marks as a first in the annals of housing bull markets. Although starter homes continued to post bigger gains in volume, suddenly the fancier homes were garnering the fastest-rising prices. In March, the medium-high tier rose an incredible 21% over the previous year, and “high” vaulted 18%. The entry categories registered still stellar increases of 12% to 13%. The reason for this anomaly: The “arbitrage” effect—the exodus from Seattle, San Francisco, and New York of work-from-anywhere folks in search of bargains to Orlando, Sacramento, and Raleigh—is inflating move-up homes in those super-affordable metros.

That’s a trend that Frank Walker, Lennar’s division president in Colorado, sees vividly. “We’re drawing people from the coasts who can work from anywhere and get a better lifestyle, and much more home, for their money,” says Walker. “Two years ago, those people couldn’t have made that move.” Joy Broddle, who oversees Las Vegas, says Lennar is benefiting from a big influx from pricey California cities. Its bestselling design is the “Next Gen” home, which encompasses a separate suite with its own entrance and kitchen that is popular for live-in grandparents and is now also being used as a roomy workspace or home gym. Customers are also willing to move much farther from their jobs than ever before. Broddle finds that people working and renting in the Henderson, Nev., area would seldom buy a home 29 miles northwest in Summerlin because of the long commute—even if they could afford to upgrade. Now, Lennar’s subdivisions are seeing a parade of buyers previously tied to their jobs in Henderson who love Summerlin’s breathtaking desert views.

Carlos Gonzalez, who heads Lennar’s operations in Miami-Dade, observes that young professionals who once flocked to downtown apartments are now buying in the suburbs. “Before the pandemic, that millennial market barely existed for us,” he says.

Winning the rodeo is the Lone Star State. Texas is benefiting from a nexus of all the big trends and migration from the coasts—coming from both refugees seeking bigger, cheaper homes who can work in San Francisco and live in Dallas, and the people moving to work in one of the nation’s strongest cities for job creation. David Grove, who heads the Dallas/Fort Worth division, says that many renters and owners who already had long commutes now will move much farther from their jobs because they no longer have to commute at all, and can bank big savings on transportation, freeing funds to buy a home. In 2018, Lennar closed on 2,000 homes in Dallas/Fort Worth. This year the figure is 2,600, and by the end of 2021, Grove expects to hit over 3,000. A big reason: The market has one of the highest concentrations of starter homes in the Lennar network. Its $175,000 to $250,000 entry-level abodes account for 70% of sales.

Much as he’s become attached to his home office, Stuart Miller ventures out many evenings to his favorite eatery, Prime Italian in Miami’s South Beach. There, he always occupies the “elbow” at the same corner of the bar when dining alone, or with a frequent dinner companion such as LenX head Feder, who sits diagonally across. The two, who have been a fantastically successful team as tech investors, often joke about that early vision of Lennar’s “Home of the Future.”

Miller was clearly, and comically, ahead of his time. Now, it appears, he’s in exactly the right spot.

This article appears in the June/July 2021 issue of Fortune with the headline, “Subdivide and conquer.”

Our mission to make business better is fueled by readers like you. To enjoy unlimited access to our journalism, subscribe today.