When Hedge Funds Are Toxic for Stocks

Additional reporting by Scott DeCarlo

Some of this year’s most volatile stocks have a key factor in common: hedge funds own a high percentage of their shares. Here’s why “hedge fund hotels” can cause sleepless nights for other shareholders.

Zoetis was plunging, and nobody could figure out why. Shares of the animal-health company started falling in January and kept tumbling between the end of February and the middle of March, dropping a total of 15% even as the S&P 500 began its biggest rally of the year. Investors couldn’t chalk up the selloff to the concerns over drug-price gouging that have depressed other pharmaceutical shares: Zoetis (ZTS), after all, makes medications for dogs—whose health care costs have yet to inspire Senate investigations.

The stock’s underperformance was a “headscratcher” for Jim Tierney, the chief investment officer of the $4 billion U.S. concentrated growth portfolio at AB (formerly AllianceBernstein), which owns Zoetis shares. But then it dawned on him: Zoetis was a big holding in Bill Ackman’s hedge fund, Pershing Square, which was in the middle of its own nosedive because of an 80% drop in its holdings of Valeant Pharmaceuticals (VRX). Investors, Tierney reasoned, were anticipating that Ackman might have to sell other stocks to cash out clients who demanded their money back—and those Ackman watchers were therefore selling their positions in those stocks too.

Ackman says he hasn’t had to sell holdings to fund redemptions. But the manager, known for his vocal activist campaigns, has largely blamed his recent underperformance on the same phenomenon. In a letter to shareholders in January, he even gave it a name: the Pershing Square Correlation, caused by the many investors who follow him into his stock picks and who, after Valeant’s meltdown, “were likely forced to liquidate substantial portions of their holdings which overlap with our own.” While his explanation may include a bit of vanity, the stocks those investors owned in common went down—including Zoetis, more than a fifth of whose shares are controlled by hedge funds. (Ackman tells Fortune he thinks the issue is “a short-term trend.”)

Zoetis’s fall is a signature example of a problem that has recently inflamed investors well beyond Wall Street. Hedge funds as a group lost money in 2015 and the first quarter of 2016—their worst performance in years. Their clients have voted with their feet. Investors pulled $15.1 billion out of hedge funds in the first quarter, the industry’s biggest withdrawal since the recession in 2009, according to Hedge Fund Research. And much of that pain comes down to one simple factor: The stocks that the hedgies like best have become some of the market’s biggest recent losers.

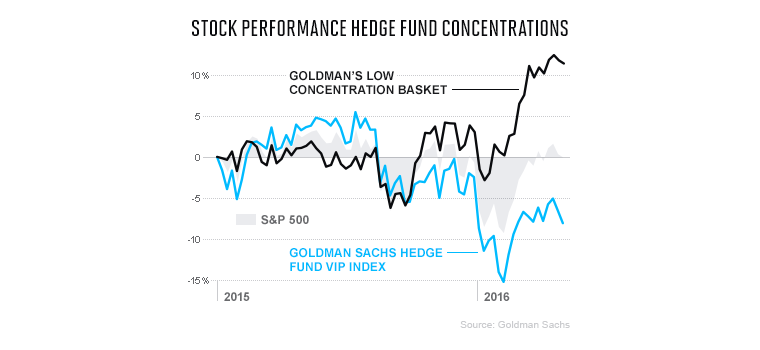

For the past 15 years, Goldman Sachs has been tracking S&P 500 companies with the highest hedge fund ownership, along with its Hedge Fund VIP List, a set of companies that appear most in hedge funds’ top 10 holdings. (Hedge funds own 14% of the VIP companies on average, more than twice what they hold in the typical S&P 500 company.) Though the VIP list has beaten the market nearly two-thirds of the time since 2001, it began underperforming late last summer. Of 27 U.S. stock baskets that Goldman tracks, it’s the second-worst performer year to date, down 5%.

This trend has a lot to do with the type of stocks hedge funds favor: companies with high earnings growth and a proclivity for acquisitions, as well as “momentum” stocks—stocks on an upward tear ahead of the market. But such stocks can sting shareholders when sentiment about the economy sours. And sure enough, momentum suddenly took a U-turn earlier this year, when bear market fears spurred by China and tepid global growth sent investors fleeing to cheaper, defensive stocks. “It’s not their fees that’s killing them. It’s their not buying the right companies,” says Bob Olstein, a value investor and the founder of the Olstein mutual fund family. “Everybody is buying companies that are sexy but aren’t producing any cash.”

The second culprit in hedge funds’ underperformance is their tendency toward a herd mentality. They crowd into the same stocks, leaving a shortage of prospective buyers when they try to flood out at the same time and worsening the free fall in the stocks’ prices. Companies like Valeant and SunEdison (SUNE)—quintessential hedge fund hotels, as the industry’s favorites are known colloquially—have been case studies in the dangers of herding. And those problems only deepen when other investors, including mutual fund managers and owners of ETFs that imitate hedge funds, join the stampede in and out of the stocks. The more than 100 hedge funds that owned Valeant going into the fourth quarter of last year lost $15.2 billion over the next six months, according to research firm Symmetric.io. And 56 hedge funds together owned as much as 32% of SunEdison when it filed for bankruptcy in April.

Now hedge fund managers are accusing one another of compounding their mutual woes. Speaking at the Milken Institute conference in May, SAC Capital founder Steven Cohen, whose family office, Point72, manages $11 billion, bemoaned becoming “collateral damage” as other hedge funds sold down stocks that he happened to own too. He said his “worst fears were realized” as he lost 8% in four days in February because of such moves, even as the rest of the market rose.

Amid the carnage, though, lies an opportunity for individual investors to get a leg up on the supposed smart money. Goldman Sachs, in addition to tracking the Hedge Fund VIPs, follows the S&P 500 stocks least owned by hedge funds. Those companies just turned in their strongest six-month returns since 2008. They’re up 8% through May 6, beating the S&P 500’s 0.6% gain.

More striking, when Fortune ran its own analysis of a larger universe—thousands of U.S. stocks with a market cap of $1 billion or more—the same pattern emerged. The lower their hedge fund ownership, the better their performance, and vice versa.

What do these winners have in common? The stocks that hedge funds have largely ignored tend to be much larger than the hotels, have less debt, grow earnings more slowly but consistently, and pay bigger dividends (an average yield of nearly 3% for the S&P 500 constituents, compared with 2% for the index overall). They don’t have the scent of instability that often attracts activist investors. “If a hedge fund is saying no, that’s actually a good sign for us,” says Kate Warne, an investment strategist at Edward Jones who oversees $900 billion.

Those stocks also tend to hold up better in periods of volatility, when hedge funds often sell their large-cap stocks to boost their own liquidity. “I absolutely look at what I call the neighborhood when I’m investing in a stock, to see what other kinds of investors are in there,” says Whitney George, who manages the Sprott Focus Trust, “so you don’t end up sitting in a very crowded movie theater when a fire breaks out.” And generally, says David Kostin, Goldman’s chief U.S. equity strategist, “Hedge funds can’t sell what they don’t own.”

Of course, simply having stocks with the lowest hedge fund ownership isn’t a promising long-term strategy. Kostin expects hedge fund VIPs to perform well again once the U.S. and global economies show clear signs of growth, China’s slowdown stops threatening the rest of the world, central banks stop seesawing, and investors stop worrying so much about an impending market crash. (If you can predict when all that’s going to happen, good for you.) And copycatting top investors isn’t inherently a bad idea. Warren Buffett, a onetime hedge fund manager, has more investing disciples than just about anyone else, and few would complain he has steered them wrong over the years. Still, it’s never a bad time to hedge the hedgies. In the stories linked below, we offer stock picks (and stocks to avoid) for investors who want to do just that.

More from the Fortune Midyear Investor’s Guide:

• 6 Stocks You Should Own Because Hedge Funds Don’t

• 3 “Hedge Fund Favorite” Stocks to Avoid

• Why Starbucks Is a Hedge-Fund-Proof Stock

A version of this article appears in the June 1, 2016 issue of Fortune with the headline “Why Hedge Funds Make Bad Neighbors.”