Payments on federal student loans have been on pause for nearly two years to give borrowers a financial break during the pandemic. After several extensions, though, borrowers will be on the hook to start making payments again in less than 100 days. Currently, there are about 43 million federal student loan borrowers who hold a collective $1.6 trillion federal student loan debt, according to the Federal Student Aid office.

“It’s important to remember that the payment pause is a response to a specific emergency and not a panacea,” Eileen Connor, director for the Harvard Law School’s Project on Predatory Student Lending, tells Fortune. “Pausing repayment on federal student loans—and preventing interest from accumulating—is humane.”

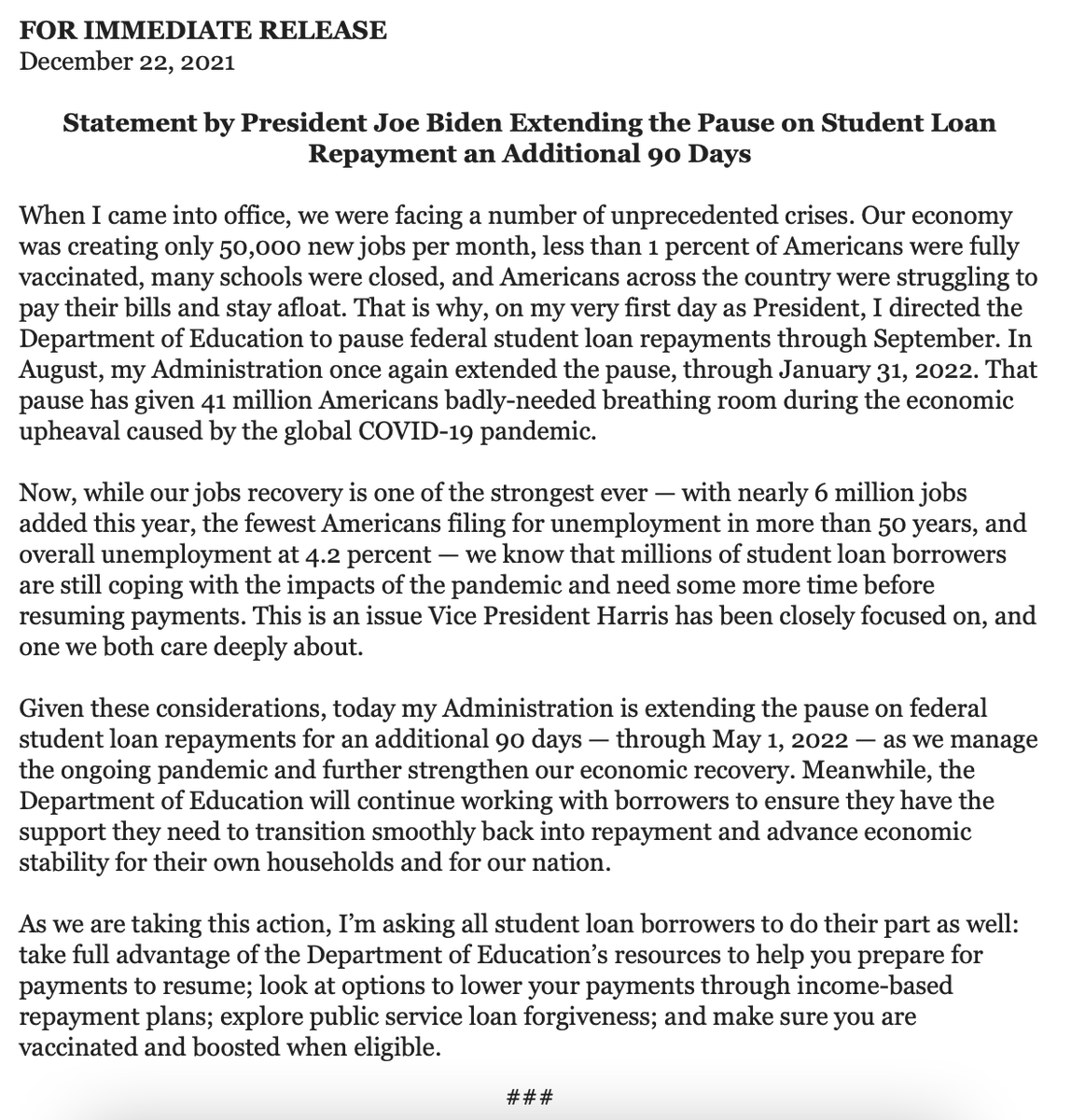

In late December, President Joe Biden extended the forbearance period from Jan. 31 to May 1 as “millions of student loan borrowers are still coping with the impacts of the pandemic and need some more time before resuming payments,” Biden said in a statement. This extension came as a surprise since the January date had been deemed as the final deadline, White House press secretary Jen Psaki confirmed earlier that month.

As we near the new May 1 deadline, advocates and borrowers question whether that date will actually mark the end of the forbearance period since it’s now been extended six times.

“Anything is possible at this point given the number of previous extensions and growing political pressure from progressives during an election year,” Robert Kelchen, higher education professor at the University of Tennessee, Knoxville, tells Fortune.

What could cause another extension

Top Democrats have been some of the loudest voices calling for further student loan forbearance—and even debt cancellation. Travis Hornsby, founder of Student Loan Planner, says that political considerations could cause the administration to extend the pause on student loan forbearance into 2023. An additional extension would require a balance of economic considerations, however.

The forbearance extension until May 1, Hornsby says, elicited pushback from economists such as Larry Summers, former President Barack Obama’s head economic adviser.

“Judged purely in terms of economic impacts, the [a]dministration’s decision to extend student loan moratorium is highly problematic,” Summers tweeted on Dec. 24, 2021.

Biden could decide to extend forbearance yet again if he decides doing so will help his party win the midterm elections, Hornsby says. Otherwise, another virus wave or if the economy were to be “pulled back significantly” could spark a need for further extension, he adds.

“Continuing to suspend student loan payments provides fodder for critics to say that the economy is not strong and the pandemic is not over,” Kelchen says. “My best guess is that student loan payments resume on May 1 barring an unexpected new wave of the pandemic, but I would put the chances of resuming at only about 70%.”

Some borrowers are also holding out hope on the possibility that their loans could be canceled outright since Biden campaigned on forgiving $10,000 per borrower. While Biden created that expectation as a candidate and as president hasn’t done anything to dispel that idea, Connor says, it’s still difficult to predict what will happen.

“This adds to borrower confusion, especially for our clients, who are still waiting for their fraudulent loans to be canceled,” Connor adds.

What borrowers should do

There’s no true indication that the Biden administration is considering another extension beyond May 1 at this point, Adam S. Minsky, a student loan lawyer, tells Fortune.

That being said, “anything is possible—last year, the administration repeatedly characterized the extension to Jan. 31, 2022 as the ‘final’ extension, only to extend it yet again at the last minute,” Minsky says.

But because there’s still so much that remains unknown, borrowers should prepare to resume payments in May, student loan experts agree.

“I would not advise people to plan based on an assumption that there will be an extension of the program,” Bruce McClary, senior vice president of communications for the National Foundation for Credit Counseling (NFCC), tells Fortune. “The best advice for student loan borrowers who are taking full advantage of the forbearance period is to plan for a resumption of payments in May.”

See how the schools you’re considering landed in Fortune’s rankings of the best business analytics programs, data science programs, and part-time, executive, full-time, and online MBA programs.

{kind=link}