Good morning. CFOs in the health care sector are laser-focused on building patient loyalty, and some may be taking a nod from retailers in using advanced tech to enhance the customer experience.

Finance chiefs of hospitals and health care systems understand that competition now includes private equity-backed chains, or companies like CVS Health, said John Summerlin, managing director in Grant Thornton’s national health care advisory practice.

I had a conversation with Summerlin about the firm’s recent survey of 100 health care CFOs in which nearly three-quarters named patient experience enhancement as the most important part of their growth strategy. The survey also asked respondents to provide words that best describe decisions that drive growth and “technology” was cited the most.

Finance chiefs know growth is dependent on serving as many patients as possible, and a controlled way to do that is by providing for all of one patient’s health needs within a single organization, Summerlin said. A system that already features a patient’s primary care doctor, for example, should include—or at least streamline—seeing a specialist or getting lab work done.

Think about shopping at a retailer: If an item is hard to find, or you have difficulty buying it, then you probably won’t return, Summerlin told me. From a health care perspective, if you show up at a primary care visit on Monday, and are told to go to a physical therapist, but there’s no guidance in selecting one, then you’ll most likely find one on your own.

Other priorities mentioned by growth-minded CFOs were expanding into new markets (65%), launching new services (64%), increasing community outreach (60%), and M&A activity (38%), according to the survey.

Enhancing customer experience also includes better technology. A major retailer like Amazon is seen as a leader in its digital experience for customers, according to Qualtrics. A health care system may have a totally different business objective, but enhancing digital offerings for customers still has tremendous upside.

“The patient loyalty model would be: My patients want to engage with me at the highest convenience point—and that includes telemedicine—so I need to deliver seamless, simple access to telemedicine for all of my patients for all of my customers,” Summerlin explained. Another example could be using technology to create more transparency around the bills being sent out.

Components of a health care system include diagnosis, treatment, administration, and operations. Although the health care system has been behind in technology adoption for a long time, he added that “we’re starting to see some more of that adoption and that innovation.”

“Pre-COVID, we thought that no one over the age of 65 would ever engage in telehealth,” Summerlin said. “Two-and-a-half years after COVID, we found out that regardless of age group, people are eminently willing to talk to their provider on their computers or on their phone.” And a new generation of doctors and nurses are also more comfortable doing so.

Generally, with “the retail conversion of health care,” CFOs in the sector may have to think like a retailer when it comes to customer experience, Summerlin said. But they also can’t lose sight of the original mission.

“The business of health care is not deploying technology, or closing the books, or writing the journal entry, or ordering the supply—it’s providing the best care to patients,” he added. “That is a very unique challenge.”

Sheryl Estrada

sheryl.estrada@fortune.com

Leaderboard

Kate Thomson was named CFO at BP, a British multinational oil and gas company, effective immediately. Thomson has held the role of interim CFO since September 2023. She was previously BP’s SVP of finance for production and operations, responsible for the financial stewardship of and commercial partnering with the business globally. She has been with the company since 2004, previously holding a number of senior financial roles, including group treasurer and group head of tax.

Phil Graves was named CFO at Meati Foods, a producer of meat alternatives based on the company's MushroomRoot, effective immediately. Graves joins Meati from Wild Idea Buffalo Co., where he served as the CEO for nearly two years. Previously, he served as the chief sustainability officer and foundation president at Bass Pro Shops, the VP of corporate development at Patagonia and founder of its corporate venture fund, Tin Shed Ventures.

Big deal

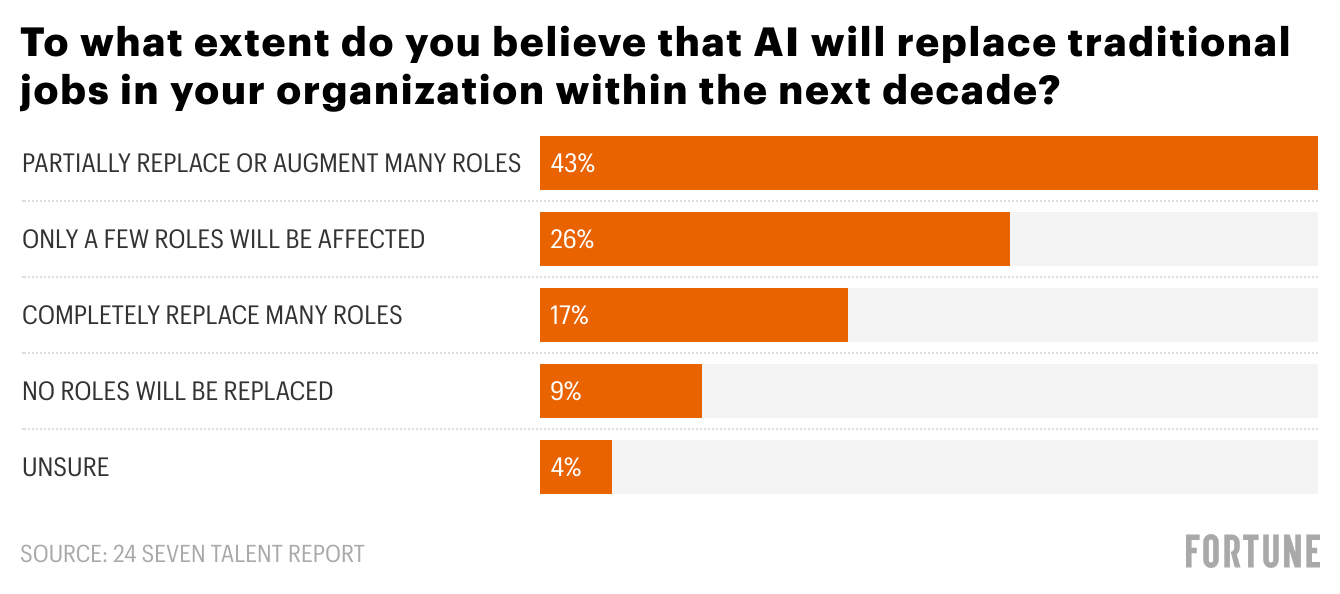

24 Seven's new report, AI, Upskilling, and Staff Augmentation, focuses on specific hiring, staffing, and training challenges companies face. The findings are based on the viewpoints of 2,100 professionals across the U.S., Canada, and the U.K. in the marketing, creative, tech, fashion, and retail sectors.

One of the key findings is that 84% of respondents say their organization is using AI-powered tools. However, 55% believe employees in their organization only have basic, very limited, or no understanding of AI, according to 24 Seven, a marketing, creative, and tech recruiting firm. The survey also finds that 43% of respondents believe AI will replace or partially augment roles, and just nine percent believe no roles will be replaced, according to the report.

Going deeper

Pew Research Center's new report on social media provides insight on the patterns and trends of how Americans engage with content and share information. Overall, YouTube and Facebook are the most-widely used online platforms. Meanwhile, about 50% of U.S. adults say they use Instagram, and smaller shares use sites or apps such as TikTok, LinkedIn, and Twitter. The report also breaks down the findings by demographics. For example, 93% of Americans 18-29 use YouTube, 78% use Instagram, 67% use Facebook, 65% use Snapchat, and 62% use TikTok. Less than half (42%) say they use X (formerly known as Twitter). The findings are based on a Pew survey of 5,733 U.S. adults.

Overheard

“In my little group chat with my tech CEO friends there’s this betting pool for the first year that there is a one-person billion dollar company, which would have been unimaginable without AI and now will happen.”

—OpenAI CEO Sam Altman said during an interview with Reddit cofounder Alexis Ohanian that he regularly speculates about when the first startup founder will reach a billion-dollar valuation. Unicorns, startups valued at $1 billion before going public, are facing a reckoning, and those that have gone belly up, have become “unicorpses” leaving founders, employees, and investors in a vulnerable position, Fortune reported.

This is the web version of CFO Daily, a newsletter on the trends and individuals shaping corporate finance. Sign up for free.