Defying conventional wisdom, Gen Xers and millennials—who share a reputation for being financially unstable—may be better prepared for retirement than the older and more dependable baby boomers.

This finding by investment advisor Vanguard seems contrary to years of economic research that projected millennials would be worse off than the generations that preceded them. Younger generations have had to weather a number of economic tsunamis: the financial crisis that started in 2007, which struck as many of them were entering the workforce; a crushing housing market that’s made homeownership a fantasy for many; and then yet another economic downturn during the pandemic.

However, financial advisors Fortune spoke to said the better retirement readiness was a result of decades of new regulations that made it easier for millennials to save for retirement, especially when compared to when boomers entered the workforce roughly 40 years ago.

“It’s funny, I’ve always said that the younger generation has really got it going on,” says Steve Azoury, an independent financial planner from Troy, Mich.

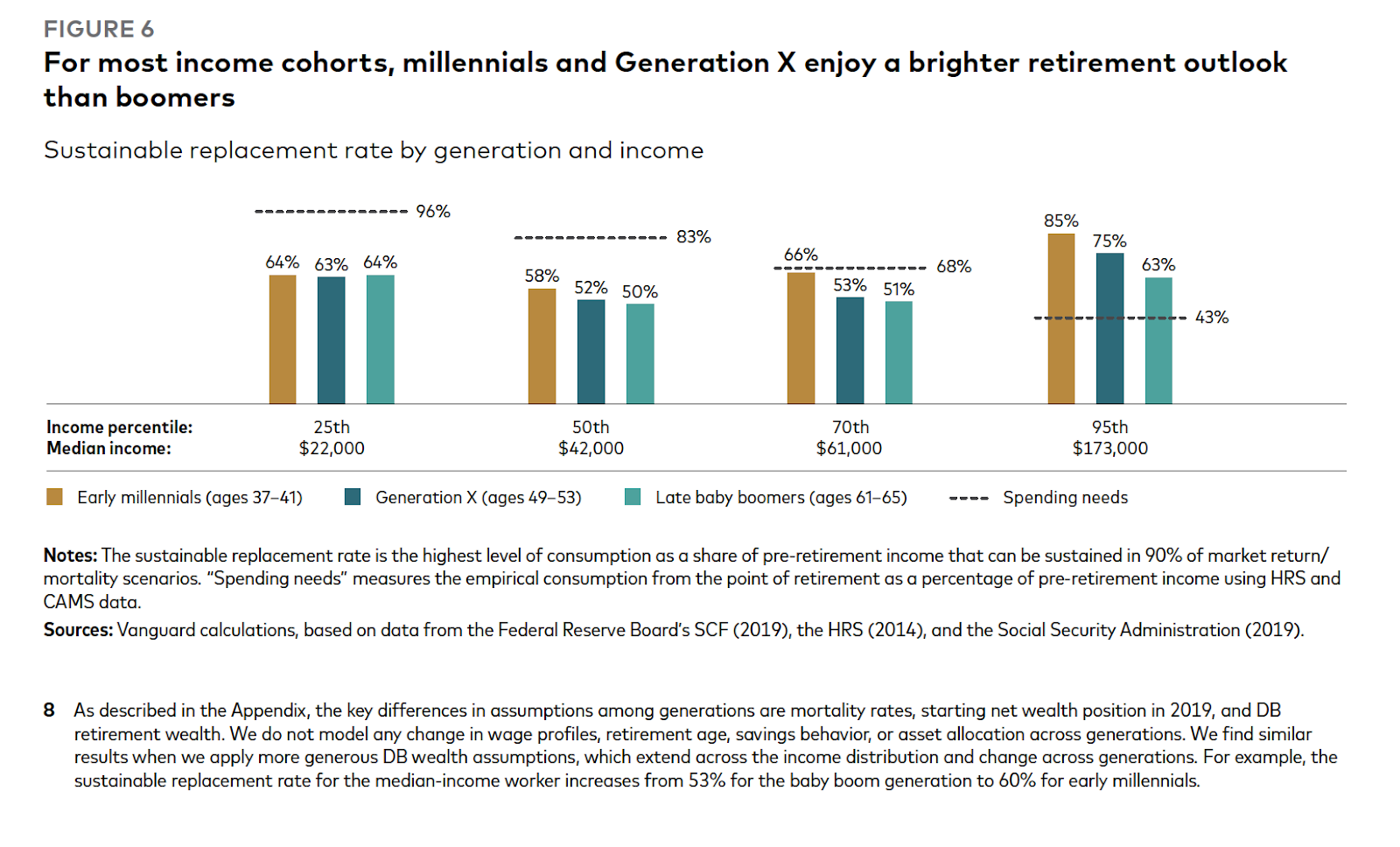

For its research, Vanguard measured the percentage of pre-retirement income and savings of households at different income levels needed to retire comfortably and how far from that target they actually were. In all but the lowest quartile of households, boomers are projected to be less prepared than younger generations. Meanwhile the poorest Americans, regardless of their age, were equally unprepared for retirement.

The study factors in only a small slice of ages within the millennial, Gen X, and boomer generations because looking at the entirety of each generation, spanning some 20 years, would have been too difficult to accurately project, according to Fiona Greig, global head of investor research and policy at Vanguard and coauthor of the report. Within the study Vanguard’s researchers looked only at financial holdings, such as stocks, cash, and bonds, and didn’t include housing, which can be a significant source of an individual’s net worth that can be tapped for retirement.

One of the main reasons that younger generations are, perhaps counterintuitively, better prepared for retirement is because they have access to retirement plans with more sophisticated resources and better investment opportunities, according to Greig. In 1978, Congress passed legislation to create the modern-day 401(k) retirement accounts into which some employers match contributions. Previously, many employers paid pensions to retired workers. But as employees lived longer, changed jobs more frequently, and unions lost power, companies became less enthused about shelling out money for ex-employees to enjoy retirement.

“Employers were saying, ‘Forget it, I can’t do this anymore,’” says Azoury. “I can’t pay you a benefit for longer than you worked for me.”

Among the most significant developments involving 401(k)s have been automatic contributions, automatic increases in the amount employees contribute, and inclusion of target date funds, which adjust an individual’s investments as retirement approaches, Greig says. All of these developments mean that even the least financially savvy person can end up with a viable retirement nest egg as long as they contribute enough money into it.

“The procrastinator who says, ‘I’ll get to it later on’ and never gets to it—he’s automatically enrolled,” Azoury says. “And then when he starts seeing statements with his name on it and his accounts are growing, he gets very excited.”

There’s evidence to back up these claims. When companies implement automatic retirement account enrollment plans, 91% of eligible employees participate by saving for retirement. When enrollment becomes voluntary, that number drops to just 28%, according to research cited by Vanguard.

However, when it comes to the poorest U.S. households, millennials and Gen X lose the advantage over boomers. Greig suspects this is because people at the lowest income levels don’t have access to employer retirement plans, which have helped higher earners in their generations save.

“Low-income workers are less likely to be in a job that offers a retirement plan, right?” Greig says. “So these improvements in plan design only apply to those who have access to a plan.”

In fact, lower income households making less than $22,000 a year, across all generations—millennials, Gen X, and boomers—are on track to have just 63% to 64% of their pre-retirement income saved when they retire compared to the 96% they’d need. People in that income bracket, however, often make retirement planning a distant afterthought while prioritizing day-to-day needs. “I don’t even know how someone can survive on that to be honest let alone save for retirement,” says Russell Gaiser, a financial planner with the Financial Guys, a wealth management firm.

Homeownership is a ‘powerful but imperfect lever’ for retirement

Workers facing a gap in the amount of money they’d need to retire have a few options to make up for the shortfall, according to the Vanguard report. There’s the obvious one—working for more years. Delaying retirement was a popular decision for those who had expected to do so in 2022, due to it being a down year for stocks and a historically bad year for bonds, according to Gaiser.

Another option, which is more controversial but nonetheless touches on generational economic anxieties, is to tap into one’s home equity. Millennials have long struggled to own a home amid a national housing shortage and recent sky-high interest rates, while boomers had an easier time. More baby boomers may also be paying off mortgages than millennials and Gen X, more of whom rent, leaving boomers with less disposable income to contribute to their savings accounts.

Vanguard calls using home equity to make up the gap in retirement readiness “a powerful if imperfect lever.” The report cites two options: a reverse mortgage on a fully paid-off home or selling it altogether and either moving to a cheaper location or downsizing. Both would provide a windfall of cash. Gaiser considers these options more of a safety net than a chess move. “Tapping home equity is an option if it’s needed, but I don’t see that as a sustainable thing to recommend to folks,” he says.

Azoury doesn’t share the same reservations. Selling a home and buying a cheaper, smaller one is a lifestyle choice as much as a financial decision. “Maybe I don’t want to take care of a home when I retire,” Azoury says. “I’ll go to a nice condo and then use that equity to buy the condo. So now I’ve got housing at no charge.”

For younger people who may feel priced out of the tight housing market, Azoury recommends considering homeownership as part of their retirement plan alongside savings. Millennials “just have to realize that maybe part of their portfolio is going to be the house,” he says. “It’s not just my 401(k) or any [other investments], but also the house. Hopefully I’m in a nice area that’s going to appreciate, and that’ll be part of my retirement plan.”

Greig, however, thinks individuals can still properly prepare for retirement without owning a home. (Vanguard’s analysis in the report didn’t account for homeownership.) In fact, she doesn’t consider owning a home to be the financial benefit it once was because it can lock too much of people’s wealth into a single asset that can take time to sell.

“Maybe this is a bit provocative, but the notion that there will be a generation of people who are lifelong renters, who don’t invest in a home, but build out their wealth and their retirement in financial assets, rather than housing assets, isn’t necessarily a bad thing,” Greig says.