Good morning,

Most bosses blame layoffs on economic downturns, a decline in demand for services, or even overhiring. But one Wharton professor has a different view: It’s how U.S. accounting rules force companies to classify human capital that makes them seem like an expense to be cut, rather than an asset to be protected.

Peter Cappelli, the George W. Taylor professor of management at the Wharton School, is the author of the new piece, “How financial accounting screws up HR,” published in Harvard Business Review. Cappelli argues that employers have gotten bad at managing employees and U.S. financial reporting standards are in part to blame.

“If employees had asset value, one would think twice about just cutting them,” says Cappelli, also the director of Wharton’s Center for Human Resources.

For decades, public companies have been required to use generally accepted accounting principles to report their financials. But the standards for these accounting rules set by the Financial Accounting Standards Board need a reboot, according to Cappelli. Though they may be your biggest competitive advantage, “Employees are not considered assets—even though the tenure of a valuable employee is often far longer than the life of any piece of capital equipment,” he writes.

Employees, along with investments in them, are treated as expenses or liabilities, Cappelli notes. According to Layoffs.fyi, a website that tracks tech layoffs, 312 tech companies have laid off more than 97,000 workers since January.

But sometimes layoffs are counterproductive as there are also hidden costs, Fortune’s Geoff Colvin reports. “Some companies learned this lesson the hard way in past downturns,” Colvin writes. “In the prelude to the Great Recession, Northwest Airlines fired hundreds of pilots. When business recovered, it couldn’t hire pilots fast enough and lost millions of dollars of revenue from canceled flights.”

The current state of financial accounting of human capital also distorts practices in hiring, training, and benefits, according to Cappelli. Let’s say a company believes in an employee’s potential and sends them for a tech course. You’d think that would be investing in an employee. However, the financial accounting rules consider training costs an expense that “needs to be completely offset by income earned that year,” Cappelli writes.

Some investor groups are pushing companies to report more on HR data in financial accounting to better estimate a company’s value, he says. As a result, since 2020, the U.S. Securities and Exchange Commission has required public companies to report on aspects of human capital that are material to understanding their businesses. But the agency gave companies the power to decide what to disclose. (However, experts predict the SEC will soon begin to scrutinize human-capital disclosures.) Companies can use this as an opportunity to enhance reporting on employee training, for example, Cappelli says.

“We have seen in other contexts where employers start reporting information that is not required, most notably around diversity and demographics,” he says. “The leadership had to be willing to do that, but it was also pushed along by clients, who wanted to see those numbers.”

Cappelli thinks the investment community needs to keep pressuring the SEC for change. Would that lead to a better experience for employees? What do you think?

See you tomorrow.

Sheryl Estrada

sheryl.estrada@fortune.com

Sign up here to receive CFO Daily weekday mornings in your inbox.

Big deal

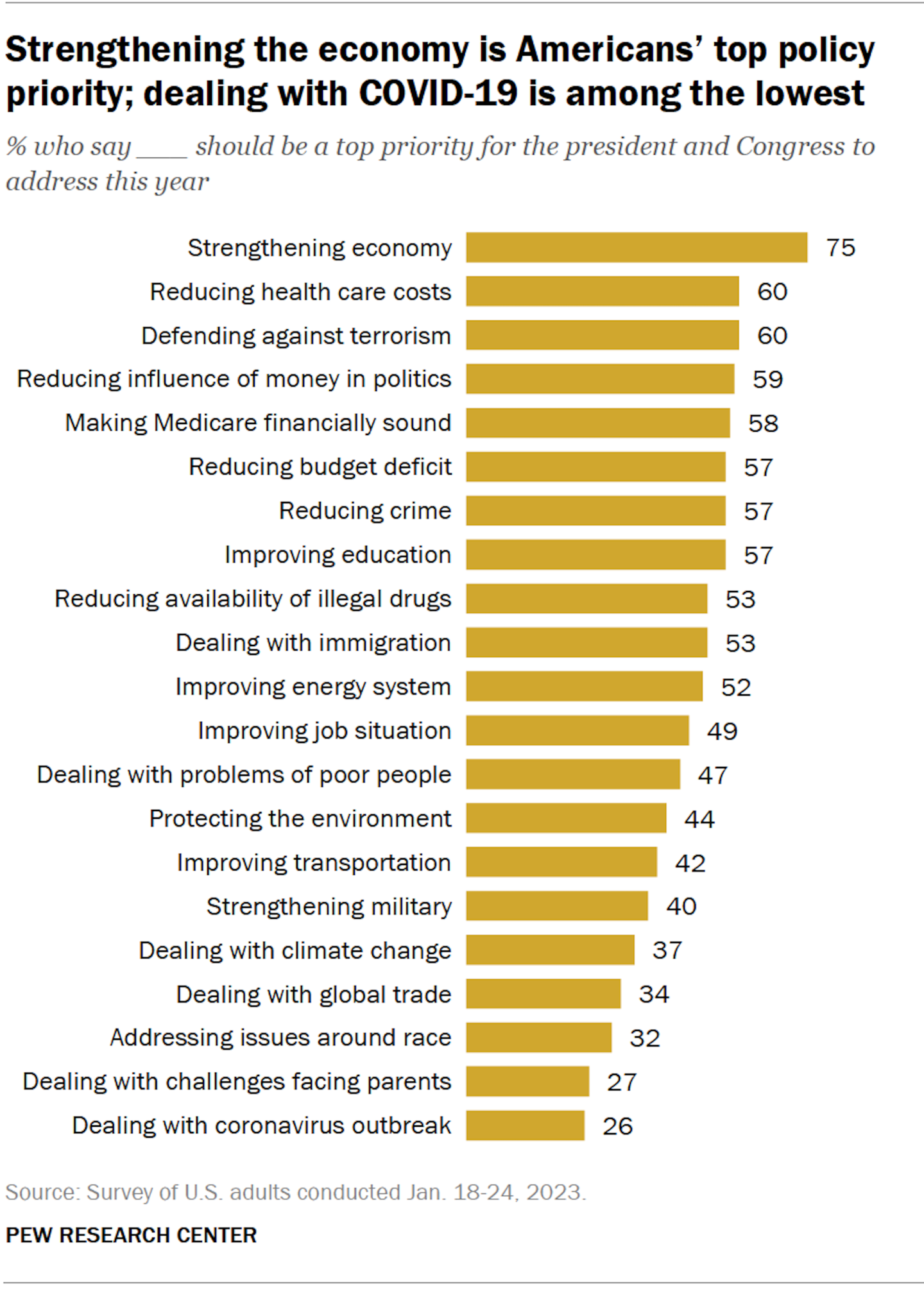

A new Pew Research Center survey found 75% of Americans say strengthening the economy should be a top priority this year. Despite continued job growth and signs that inflation may be easing, Americans continue to express negative views of national economic conditions, according to Pew. Twenty-one percent rate economic conditions as excellent or good, a slight increase from 17% in October. Respondents gave the lowest priority to dealing with the coronavirus outbreak (26%). The survey of 5,152 U.S. adults was conducted from Jan. 18-24.

Going deeper

"Starting up as a new CFO," a new report by McKinsey, offers seven "key mindsets" and practices for newly-appointment finance chiefs. "Day one is a unique chance to ask, 'What would this company’s support structures and aggregating budgets be if we weren’t defaulting to what we’ve done in the past?'" according to McKinsey. And, "How likely are these projected scenarios, really?”

Leaderboard

Teri Gendron was named CFO at Markel Corporation (NYSE: MKL), a financial holding company, effective March 20, succeeding Jeremy Noble, who became president of Markel's insurance operations earlier this year. Most recently, Gendron was CFO of Jefferies Financial Group Inc., and she has also held senior finance positions at Gannett Co. and NII Holdings. Gendron began her career at KPMG.

Darlyn Phillips was named CFO at Invariant, a bipartisan government relations and communications firm. Phillips has more than 25 years of experience in financial and business management. Phillips joins Invariant from Next Fifteen Communications Group plc, where she served as CFO and head of operations for the portfolio brand Outcast. Phillips led three acquisitions in this role, placing the agency into the global market.

Overheard

"The disinflationary process has begun. It has begun in the goods sector, which is about 25% of the economy."

—Federal Reserve Chair Jerome Powell said of the U.S. economy on Tuesday during an interview at the Economic Club of Washington, D.C. Powell also said, "We will likely need to do additional rate increases," to bring inflation back to its 2% target, Yahoo Finance reported.

This is the web version of CFO Daily, a newsletter on the trends and individuals shaping corporate finance. Sign up to get CFO Daily delivered free to your inbox.