Kevin Kelleher here, filling in this week while Jessica is on vacation.

The California Public Employees’ Retirement System (CalPERS) has long stood heads and shoulders above its fellow pension funds. And because its fiscal year ends on June 30, its annual net investment reports are both a bellwether and a harbinger of pension fund performance for the full year.

So what does CalPERS have to tell us about pension funds in 2022? The news isn’t good. In contrast to the banner year of 2021, when pension funds enjoyed a median 25% return in 2021’s calendar year—the best performance since the 1980s—most funds will be bracing for declining returns in 2022.

In a preliminary announcement, CalPERS said last week that net returns on its investments fell 6.1% in the 12 months through June 30, its worst performance since the Great Recession. Last November, when CalPERS reallocated its investment portfolio, it assumed an annual 6.8% return.

It’s no surprise, then, that many pension funds like CalPERS are looking to push even more into alternative assets like private equity and real estate.

“As the market gets more competitive and rates start to rise, there’s a little more pressure on returns,” says Rishi Chhabria, a partner at Campbell Lutyens, a private-market advisory firm. “If anything, public pension plans are pushing more capital towards private markets.” These investments may include infrastructure projects, which offer price stability, and private credit, which can hedge against inflation.

Public pensions may seem like a relic from an era before workers had to manage their own 401(k) and IRA accounts, but it’s still a big–if not exactly thriving–sector. According to the Center for Retirement Research at Boston College, there are still nearly 6,000 state and local retirement systems that oversaw $5.1 trillion in 2021. That collective clout gives them a loud voice at shareholder meetings and a prominent role as limited partners.

But pension economics are changing. In 2001, state and local pension funds were fully funded, meaning their assets were equal to the lifetime benefits they’d promised to pay out. That ratio dropped to 75.5% last year and has likely fallen even further during 2022’s selloffs in stocks and bonds, which together make up 70% of pension portfolios.

At CalPERS, the funded ratio fell to an estimated 72% in June from 80% a year earlier. The impact of the 2022 selloff on the giant fund is even more stark if we look at the value of its assets under management, which it reports monthly. At the end of May, the most recent data available, the fund held $208 billion in global equities, down 19% from the end of 2021, and $124 billion in fixed income, down 13%. Both stock and bond indexes were trading close to record highs at the end of last year.

The silver lining for CalPERS came from its alternative investments. Private equity assets increased 9% to $54 billion in the first five months of 2022. Real assets—which can include real estate, farm and timberland, commodities, and infrastructure–rose 21% to $67 billion. But these assets are a smaller portion of CalPERS’ portfolio. Private equity holdings make up 12% of the total, and real assets about 15%.

“This is a unique moment in the financial markets, and we’ve seen a deviation from some investing fundamentals,” Nicole Musicco, who was appointed as CalPERS chief investment officer in February, said in a statement (CalPERS declined to comment for this story.) “Our private market asset classes… are bright spots that we can build on as we implement our new strategic asset allocation and increase our exposure to private market assets.”

CalPERS was an early pioneer in alternative investments but after most other funds followed its example, its performance has sometimes lagged those of its peers. The 6.1% negative return for CalPERS’ fund is larger, for example, than the negative 2.8% return for San Francisco’s public pension fund. Santa Barbara County’s fund even eked out a 0.3% return in its last fiscal year.

When CalPERS reallocated its portfolio last fall, it slashed investments in global equities while boosting holdings in private equity and real assets and adding a 5% allocation to private debt. “Within private markets, the team has done a great job in what I would call the great catch-up,” Musicco said in a press conference discussing the investment returns.

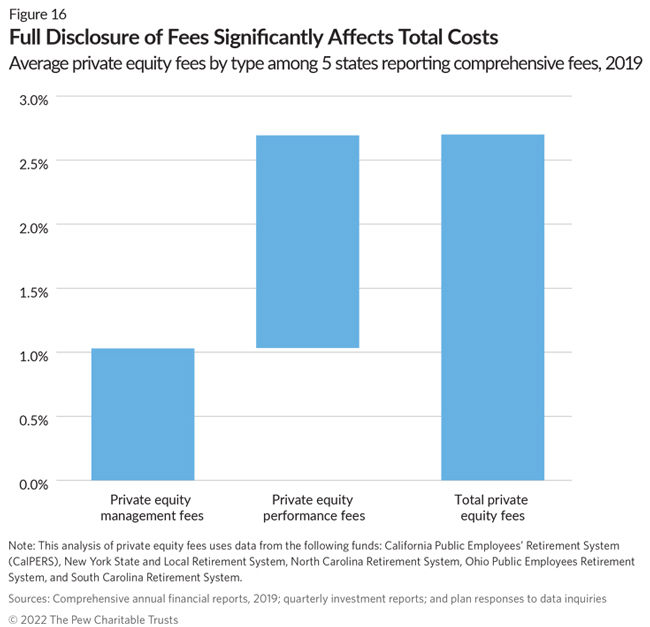

Musicco reportedly has ambitions of weaning CalPERS off fees to PE firms, which typically charge a 2% management fee and a 20% performance fee. These fees can add up, amounting to 2.75% of the value of pension fund holdings. CalPERS aims to lessen PE fees by buying direct stakes in private companies, a model more common to public pensions in Musicco’s native Canada.

To make those direct investments, CalPERS is freeing up cash by backing out of some PE fund investments. It recently sold about $6 billion of its stakes in PE funds to secondhand buyers, or firms that specialize in such illiquid trades. The deal came with a 10% discount to the holdings’ value, Bloomberg reported this month. But it frees up cash for the firm to make new investments in a market with falling valuations.

While CalPERS is the largest and most visible pension fund struggling with market conditions, it’s not alone in pushing further into alternative investments. States like Wisconsin and Minnesota are making similar moves.

Pensions have lowered return assumptions from 8% to 7.25% over the past decade, even as alternative investments have grown from 18% of pension allocations to 27%, a Pew Charitable Trust report in May said. Still, Pew expects future pension returns to be closer to 6%. “Pension funds should not expect to replicate unusually high annual returns anytime soon,” the Pew report said. “Increased allocations to stocks and alternatives can result in greater financial returns but also heighten volatility and the risk of losses.”

Chhabria of Campbell Lutyens says pension fund managers can mitigate risks of alternative investment with capital structures that avoid practices like buying on leverage or financial engineering. In the meantime, most funds should ride out 2022’s turbulent markets and even have dry powder for new opportunities. “Most of them have large balance sheets, which can give them purchasing power for strategic investments.”

Kevin Kelleher

Submit a deal for the Term Sheet newsletter here.

P.S. Sign up for Fortune’s new newsletter, CHRO Daily, launching August 1. HR executives have become essential leaders in the C-suite and the workplace, and our newsletter will provide them with the news, analyses, and tips they need to navigate their ever-evolving role and the demand that comes with it.

Jackson Fordyce curated the deals section of today’s newsletter.

VENTURE DEALS

- Whatnot, a Marina Del Rey, Calif.-based live stream shopping platform, raised $260 million in Series D funding. CapitalG and DST Global led the round and were joined by investors including BOND, a16z, and YC Continuity.

- Cleerly, a New York-based heart disease treatment and analytics company, raised $192 million million in Series C funding. T. Rowe Price and Fidelity led the round and were joined by investors including Novartis, Sands Capital, Piper Sandler’s Merchant Banking, Heartland Healthcare Capital funds, Mirae Asset Capital, Peter Thiel, Breyer Capital, Vensana Capital, LRVHealth, New Leaf Ventures, Cigna Ventures, and DigiTx Partners.

- Shares, a London-based social and community-based investing app, raised $40 million in Series B funding led by Valar Ventures.

- Theator, a Palo Alto, Calif.-based surgical intelligence platform, raised $24 million in Series A extension funding. Insight Partners led the round and was joined by investors including Blumberg Capital, Mayo Clinic, NFX, StageOne Ventures, iAngels, former Netflix CPO Neil Hunt, iCON, and TripActions’ CEO and co-founder Ariel Cohen.

- Better Stack, a Prague-based managing and monitoring software platform for developers, raised $18.6 million in Series A funding. Creandum, Susa Ventures, K5 Global, Credo Ventures, Kaya.vc, Lachy Groom, and other angels.

- Atlantic Money, a London-based international money transfer company, raised $3 million in additional seed funding led by Amplo.

PRIVATE EQUITY

- Bernhard Capital acquired KC Harvey, a Bozeman, Mont.-based environmental consulting firm. Financial terms were not disclosed.

- Valsoft acquired WorkDynamics Technologies, an Ottawa-based software provider. Financial terms were not disclosed.

EXITS

- Red Arts Capital and Prudential Private Capital acquired a minority stake in Sunset Pacific Transportation, a Chino, Calif.-based LTL, freight, and transport company, from Granite Creek Capital Partners. Financial terms were not disclosed.

OTHER

- Orange, a Paris-based telecom operator, and MasMovil, a Madrid-based telecom operator, agreed to a merger, for close to $19 billion.

This is the web version of Term Sheet, a daily newsletter on the biggest deals and dealmakers. Sign up to get it delivered free to your inbox.

{kind=link}