Last week, Western nations launched the “nuclear option” against Moscow in retaliation for Russia’s unprovoked assault on its neighbor Ukraine. The U.S., U.K., Canada, France, Germany, and Italy cut several Russian banks from SWIFT, the international payments system that allows money to travel around the world, in a move intended to “further isolate [the country] from the international financial system and our economies,” the six countries said in a joint statement.

Only a few weeks ago, excluding Russia from SWIFT was considered a last resort that posed risks to Western allies’ own economies, particularly Europe’s, given its close ties to Russia’s economy.

The Western allies also balked at booting Russia from SWIFT for another reason: China. The U.S. worried that banning Russian institutions from SWIFT might strengthen Moscow’s budding alliance with Beijing, bolster the two countries’ alternative payment systems, and boost Chinese renminbi (RMB)-denominated trade. But Russia’s egregious invasion of Ukraine convinced the West to take the unprecedented step. Excluding Russia from SWIFT and other harsh sanctions have already pummeled the country’s economy. The measures may result in what the U.S. had feared: Russia inching deeper into China’s financial world, but an all-out alliance is not certain. While Beijing has the financial infrastructure to help Russia, it may lack the political will as Russian President Vladimir Putin’s assault on Ukraine escalates.

SWIFT squeeze

Established in 1972, Belgium-based SWIFT—the Society for Worldwide Interbank Financial Telecommunication—is the primary global channel that moves money across borders smoothly and efficiently. State institutions including the U.S. Federal Reserve and the European Central Bank oversee SWIFT, which links over 11,000 banks and financial institutions in more than 200 countries. SWIFT averages 40 million messages between platform users every day and accounts for more than half of all high-value cross-border payments worldwide.

Banning Russian banks from using SWIFT cut the country off from a “key artery of finance,” Scheherazade Rehman, director of the European Union Research Center and professor of international affairs at George Washington University, told NPR. Without SWIFT, Russia’s banned banks will be forced to use inefficient methods like fax, telephone, email, and bank-to-bank transfers to execute cross-border transactions, hampering Russian business’s participation in international trade.

The SWIFT ban, however, includes only some Russian banks, not all 300 Russian institutions that use the system, so it’s not exactly the “nuclear option” it was advertised as a few weeks ago, says Artyom Lukin, deputy director for research at the school of international studies at Far Eastern Federal University in Vladivostok, Russia. Western allies have warned that they could add more banks to the sanctions list.

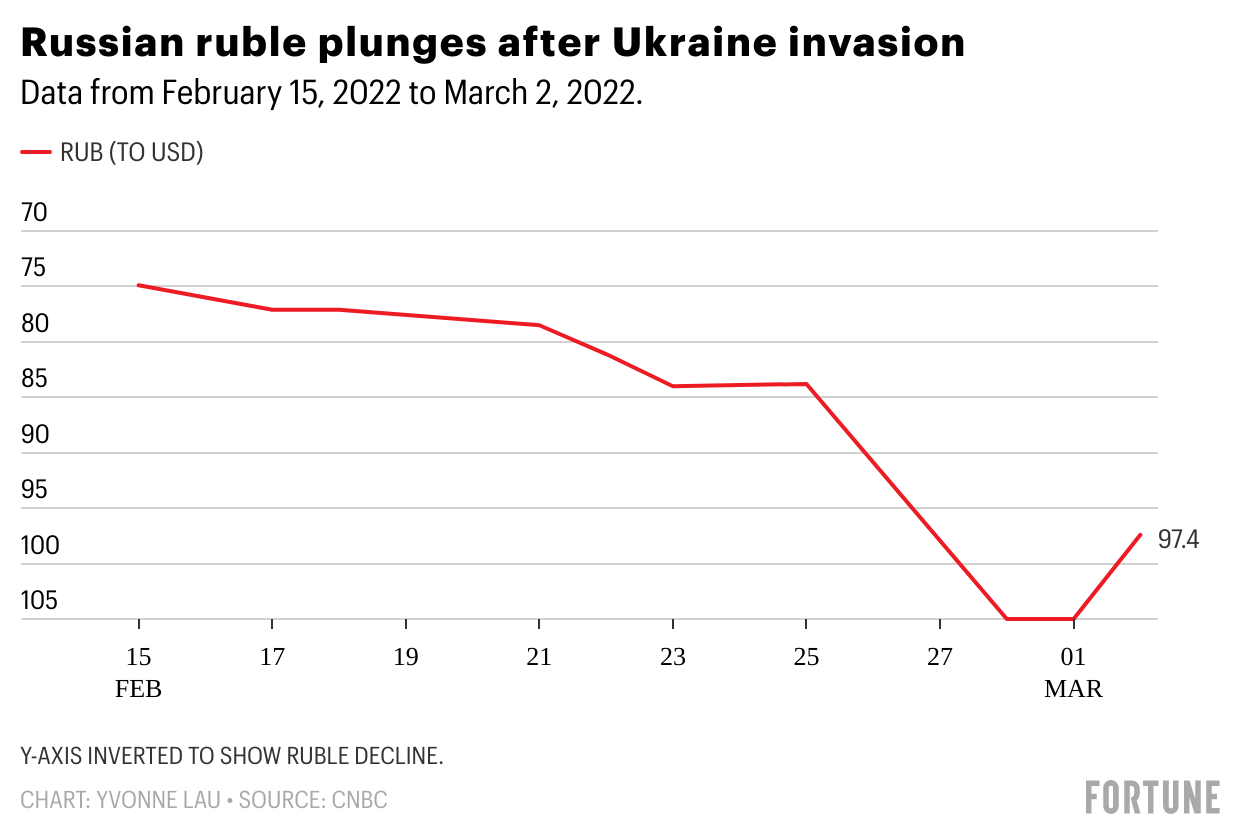

Still, Russia’s SWIFT banishment, coupled with the country’s frozen foreign exchange reserves, rocked the Russian economy almost immediately. On Monday, two days after Western allies passed their latest round of sanctions, the Russian ruble had collapsed, plummeting roughly 30% to trade at 104 against the U.S. dollar, making the currency worth less than one U.S. cent. The Moscow Stock Exchange shut down on the same day and remains closed. Russian stocks listed on the London Stock Exchange have plunged 98% in the past two weeks, wiping out $572 billion in value. Meanwhile, the Central Bank of Russia, also the subject of sanctions, hiked interest rates to 20% from 9.5% and imposed capital controls.

The sanctions will hurt ordinary Russians, who face a future of surging inflation and little to no access to the global economy. During a media call on Wednesday, Kremlin spokesperson Dmitry Peskov admitted that the Russian economy is suffering “serious blows.” In the past few days, news reports and social media accounts showed long ATM queues in Russia and included accounts of services like Apple Maps, Apple Pay, and Google Pay not working in the country. A long list of companies including Nike, Netflix, Meta, Apple, and Google have pulled back from Russia. Apple, for instance, has halted all product sales in the country.

Russia’s economy now faces a “severe recession” and a financial crisis that will strain Russian banks, Oliver Allen, markets economist at Capital Economics, wrote in a Monday note. Elina Ribakova, deputy chief economist of the International Institute of Finance (IIF), a global banking lobby, warned Monday that a Russian default is “extremely likely” if the situation continues as is or escalates. Ribakova also predicts that the Russian economy will contract and inflation will surge this year—both by double digits. J.P. Morgan estimates Russia’s economy will contract by 35% this quarter alone.

Fortress Russia’s best friend

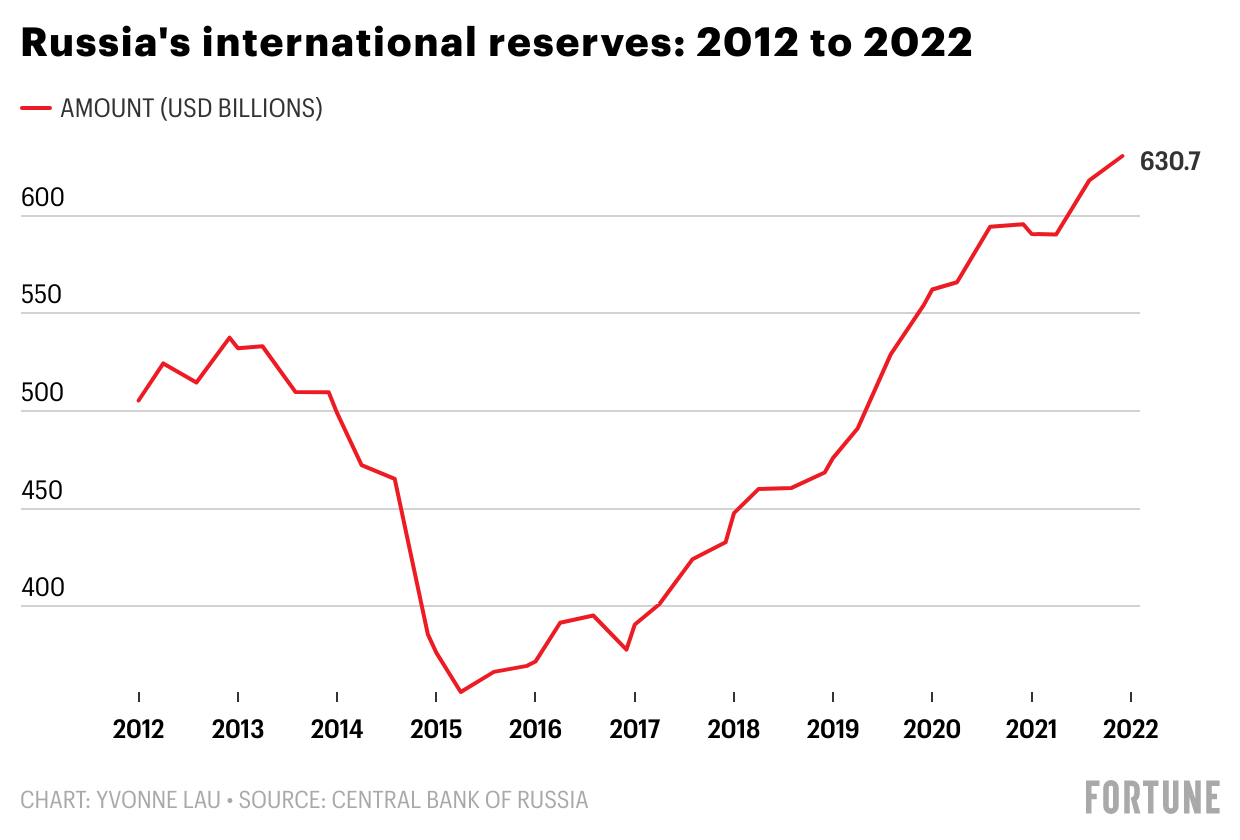

Russia, however, has been bracing for a fresh wave of Western sanctions. After Russia’s 2014 annexation of Crimea, Western sanctions battered the Russian economy, and Putin tried to “sanction-proof” his country by balancing its budgets, reducing its U.S. dollar dependency, and building its arsenal of foreign currency reserves.

As part of that effort, Russia cultivated closer ties to China. Now the West’s ongoing financial offensive against Russia will “further push Russia into China’s financial orbit,” says Lukin. Without SWIFT access, Russian firms need an “immediate remedy” to resume cross-border economic activity with the world—and China could offer just that, says Chris Pereira, executive director at China-focused investment research firm EqualOcean.

Over the past decade, Russia and China have built their own alternatives to SWIFT. Russia created the System for Transfer of Financial Messages (SPFS) in 2014, while China launched its Cross-border Interbank Payment System (CIPS) in 2015. Russia’s SPFS has limitations. It operates only during weekday working hours and messages are limited to 20 kilobytes, compared to SWIFT’s 24/7 system that allows messages of up to 10 megabytes, Chris Devonshire-Ellis, founder of consultancy Dezan Shira, wrote last December.

For those reasons, Russian banks banned from SWIFT will likely sign up with China’s CIPS, says James Fok, author of Financial Cold War: A View of Sino-US Relations From the Financial Markets. CIPS lets global banks clear cross-border RMB transactions onshore. Nearly 1,300 financial institutions—half of which are Chinese—in over 100 countries are on CIPS. The system processed $12.7 trillion last year.

Still, CIPS won’t save Russia, says Alicia Herrero-Garcia, chief economist for Asia-Pacific at French investment bank Natixis. CIPS still depends on SWIFT for international financial messaging. CIPS has its own system, but China so far has used it only for domestic transactions. If CIPS moves away from SWIFT, transaction costs would jump as much as 30% due to CIPS’s less efficient messaging system, Herrero-Garcia says. And because CIPS’s roster of financial institutions is only a fraction of SWIFT’s 11,000, Russian banks could reach only a limited number of their peers, she says.

For now, China remains heavily reliant on SWIFT. Most transactions between China and Russia take place on the system and are denominated in U.S. dollars rather than Chinese yuan. That means Western nations have leverage to pressure SWIFT stakeholders and the G10 countries’ central banks that govern SWIFT to block China from the system, just as it did with Russia.

China and Russia are, in theory, working on a joint financial payments system. Last December, Putin’s foreign policy adviser Yuri Ushakov announced that Russia and China were both “intensifying efforts” to build a service to facilitate trade between the two countries that was beyond the West’s reach. A joint Sino-Russian financial system would settle bilateral trade in renminbi or rubles, rather than dollars, says Fok.

But a unified Sino-Russia SWIFT alternative is far from becoming a reality and will be feasible only if there’s “political will on the Chinese side,” says Lukin. “If Beijing [commits to] supporting Russia as its main strategic partner, then Chinese financial institutions” will follow suit, he says.

China, which views Russia as a strategic energy partner, is threading a needle of supporting Russia financially while not running afoul of Western sanctions or risking its ties to the West, Mark Williams, chief Asia economist at Capital Economics, wrote in a note last week. China stands to benefit from Russia’s pariah status in the global economy. In recent days, it has inked major agriculture and energy deals with Russia. But one day after Russia attacked Ukraine, two of China’s biggest state-owned banks, ICBC and the Bank of China, restricted financing for buying Russian commodities, according to a Bloomberg report.

Initially, China danced around Russia’s assault on Ukraine, refusing to condemn the invasion and referring to it only as a “special military operation.” China’s banking and insurance regulator announced that it won’t support sanctions against Russia. But as the conflict drags on, Beijing has expressed more alarm. On Tuesday, China’s Foreign Minister Wang Yi told his Ukrainian counterpart that Beijing is “extremely concerned” for Ukrainian civilians caught in the crossfire and called the conflict a “war.” China is scrambling to evacuate its own citizens in Ukraine to neighboring European countries. The Ministry of Foreign Affairs website now says China “deplores the outbreak of conflict between Ukraine and Russia.”

Last week, a senior Biden administration official said that signs point to China “not coming to [Russia’s] rescue.” Though China sympathizes with Russian objections to NATO’s creep into Eastern Europe, Beijing is being careful to not cross the U.S., Fok says. Chinese institutions worry that processing payments for sanctioned Russian companies and individuals could subject them to Western sanctions too, Fok says.

“It’s not in China’s interest to test the resolve of the U.S. in its sanctioning of Russia,” says Pereira. China is likely to maintain a neutral stance in the conflict and settle cross-border transactions via existing channels but not stick its neck out beyond that, he says.

Western actions against Moscow are also driving Russia away from the U.S. dollar and euro and toward the RMB. Russia’s central bank and the country’s sovereign wealth fund likely own a combined $140 billion in Chinese bonds, according to a report by bank ANZ. Fok estimates the holdings represent 35% of global RMB reserves. Moscow has amassed a war chest of foreign reserves, but half those funds are deposited in countries that have frozen its assets, according to the IIF. Beijing hasn’t taken such an action, so Russia could “liquidate the assets if [RMB] cash is needed to meet other payment obligations,” the bank report said. Yet this week, the Chinese yuan hit a record high against the Russian ruble, making Russia’s trade with China much more costly.

Russia’s stockpile of RMB has accelerated China’s campaign to make the yuan more widespread worldwide, says Fok. The Chinese yuan’s presence in the global economy has grown in recent years but is still at a comparatively low level compared to the U.S. dollar, says Bruce Pang, head of macro and research at China Renaissance Securities. The RMB’s percentage in global foreign exchange reserves stands at 3% compared to the U.S. dollar’s 60%.

A global reserve currency functions best when its value is built on long-term economic trends, rather than short-term political expediencies like the Ukraine crisis, Pang says. “Building an international payments network and increasing the share of the [yuan] in mutual settlements would be a rosy story,” he says. “It’ll take a long time to come true.”

Never miss a story: Follow your favorite topics and authors to get a personalized email with the journalism that matters most to you.