Hong Kong’s recent moves to combat a fresh COVID outbreak appear to have triggered a secondary epidemic—of anguished accounts in Western media warning of an “expat exodus” sure to bring this once-vibrant global financial center to its knees.

“Foreign executives in isolated Hong Kong head for the exit, sick of zero-COVID curbs,” blared a recent headline in the Wall Street Journal. Hong Kong’s status as an international finance center is “cratering” because of the city’s strict quarantine rules for incoming travelers, Bloomberg lamented. The outlet quoted a London-based finance industry recruiter who declared that “No amount of money is going to convince a candidate to go to Hong Kong.”

Reuters predicts a wave of expat departures from global banks, asset managers, and corporate law firms based in Hong Kong over the next three months as bonuses are paid. The Washington Post says talent is fleeing the city “in droves.” A recent commentary in Nikkei Asia argued Hong Kong “risks sinking into Venetian obscurity.”

But reports of Hong Kong’s death are greatly exaggerated. Expats may be exiting Hong Kong, but their dwindling numbers won’t necessarily threaten the city’s viability as a global business hub. At least four structural advantages—mainland China’s deep talent pool that’s increasingly capable of filling the finance jobs expats vacate, the likely persistence of Chinese capital controls, the continued growth of the mainland economy, and a dearth of viable regional alternatives—all but guarantee Hong Kong’s future as Asia’s financial capital. Those advantages are likely to endure whether the city’s expats stay or go.

Hong Kong’s ‘expat’ community

Underlying many analyses of Hong Kong’s “expat exodus” is an unstated assumption that this city of 7.4 million can’t function without foreigners. That’s partly true—depending on how the term “expat” is defined.

In the broadest sense of the term, Hong Kong has roughly 700,000 expatriates—foreign nationals granted a visa allowing them to live in the city. About half of that number are domestic helpers, most from the Philippines and Indonesia, who earn a minimum wage of about $600 a month. As a group, this category of “expatriate” is vital to the success of Hong Kong’s economy, providing live-in childcare, cooking, and cleaning for as many as 10% of Hong Kong households.

The number of domestic helpers in Hong Kong has fallen by an estimated 50,000 during the pandemic, creating an acute shortage of labor relative to demand. It’s not that those workers are fleeing the city, it’s that Hong Kong’s quarantine policies—which have banned flights from eight countries including the Philippines and Indonesia and set aside only 2,138 quarantine rooms for the helpers who do make it here—have made it almost impossible for new helpers to get in.

But the focus of most Western media assessments of Hong Kong “expat exodus” is executives and finance professionals: bankers, brokers, asset managers, analysts, accountants, lawyers. That’s a much smaller and more affluent group whose members often receive lucrative expat packages featuring housing stipends, club fees, children’s private school tuition, and top-of-the-line health care. Hong Kong has more than 273,000 financial services jobs, but the overwhelming majority of those positions are held by locals or mainland Chinese. The percentage of expats in those roles has been shrinking for decades.

“The pandemic has accelerated trends away from expatriates, and has probably led to more mainland candidates coming into Hong Kong, particularly in financial services, investment banking, and so on,” says Alan Paul, managing director of boutique executive search firm Alan Paul Partners in Hong Kong. “But that was happening very noticeably before the pandemic struck.”

Mainland talent

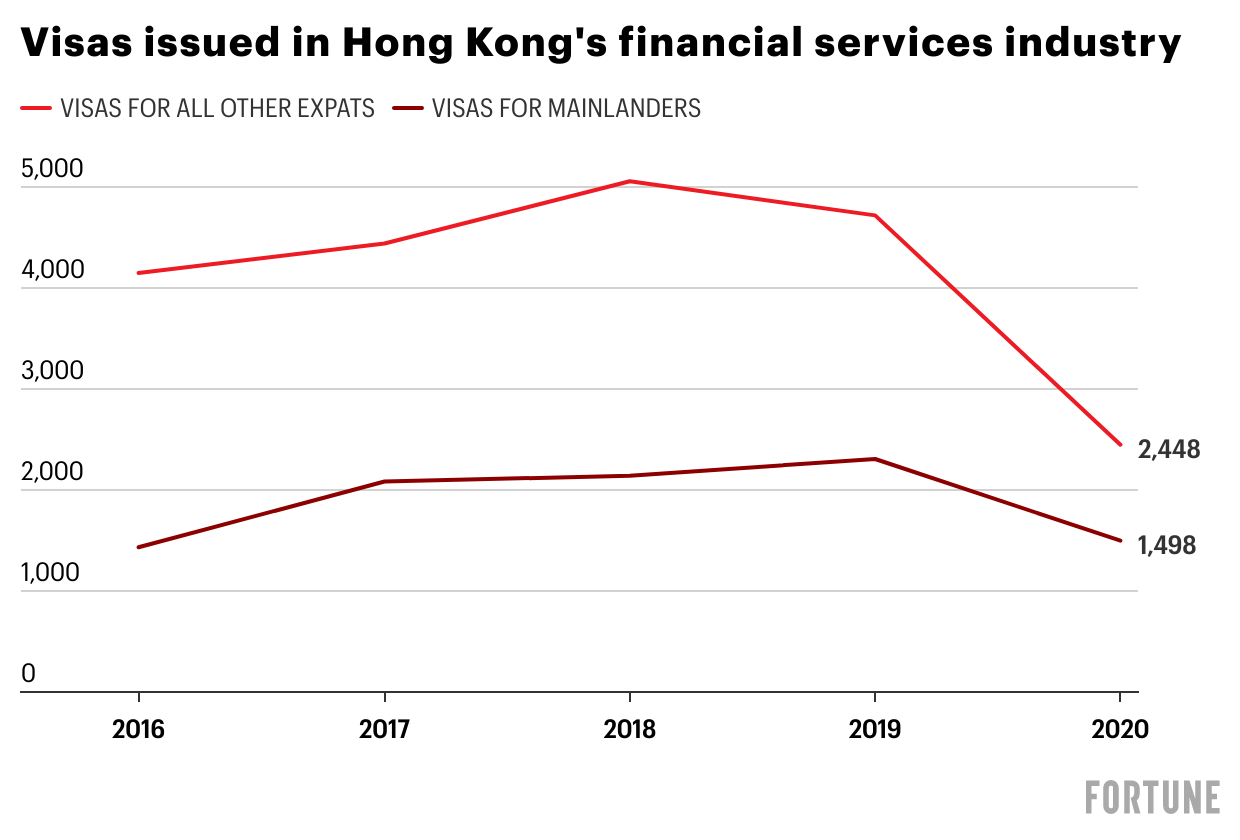

According to Hong Kong’s Immigration Department, the number of work visas approved for financial services professionals from mainland China has risen steadily over the past five years, apart from 2020, when the pandemic hit. Hong Kong approved 2,307 visas for mainland Chinese financiers in 2019, up from 1,433 in 2016. In 2020, it issued 1,498.

The data for “expat” bankers, which are counted separately from mainlanders, shows visa approvals peaking at 5,507 in 2018. Visa approvals dropped to 4,719 in 2019—the year of the Hong Kong protests—and plummeted to 2,448 in 2020.

In the first nine months of 2021, Hong Kong approved 1,874 visas for expat bankers and 1,809 for mainland Chinese, meaning it welcomed mainlanders at a quicker pace last year than in 2020. More important, those stats show that banks are still hiring regardless of the pandemic and the city’s onerous quarantine rules.

“Hong Kong has such a unique role on the doorstep of mainland China, and the contacts and the connections to China are so important. The major financial institutions have no choice but to find ways to work with the current situation,” Paul says.

A financial gateway

Although Hong Kong’s strict border controls effectively isolated the city from the rest of the world, the special administrative region remains the Western financial system’s gateway into China—as well as a venue where Chinese firms can raise foreign capital.

In the first nine months of 2021, Hong Kong’s bourse operator, Hong Kong Exchanges and Clearing (HKEX), reported that it was on track to have its best year ever, bolstered by mainland Chinese tech firms debuting on the city’s stock exchange. Mainland Chinese firms constitute the majority of companies on the city’s benchmark Hang Seng index.

Hong Kong remains “a convenient and necessary offshore destination for mainland investment,” says Bruce Pang, head of macro and strategy at China Renaissance Securities.

China’s tight capital controls, including restrictions on foreign investment and the export of the Chinese yuan, coupled with the volatility of mainland China’s retail investor–led financial markets, have thwarted the central government’s dream of positioning Shanghai as a global financial hub to rival Hong Kong. In Hong Kong, Chinese firms gain easy access to the U.S. dollar, which the city’s Monetary Authority is authorized to clear.

Meanwhile, Hong Kong offers foreign investors access to shares of some of China’s largest firms, as well as China’s offshore bond market for the Chinese yuan. The city remains the primary destination for capital flowing between China and the West, which is more than enough reason for banks to keep an oar in Hong Kong.

HSBC, BlackRock, Citibank, Deutsche Bank, and Goldman Sachs all have said they are adding staff in Hong Kong to capitalize on opportunities in China. And although some mid-level foreign bankers are considering leaving Hong Kong because of the city’s strict quarantine rules, banking chiefs have aligned with the government’s priority of reopening its borders with mainland China first.

“It’s important for Hong Kong to establish what they need to establish with China on reopening,” HSBC Holdings CEO Noel Quinn told Bloomberg at the news service’s New Economy Forum in Singapore last November. “I don’t want to do anything that would jeopardize that.”

Pang acknowledges an expat exodus, combined with emigration of some local financial professionals, may weaken the city’s banking sector in the short term because foreign bankers often bring valuable networks and insights that can’t be matched by local Chinese staff.

But Pang argues such “outward-facing skills” may become less important in coming years as Hong Kong’s financial system aligns itself more tightly with China. “Some professional skill sets may be left as a legacy, and the influx of mainland Chinese firms may partly offset expat departures,” he says.

Professionals from mainland China also bring language skills that their Western peers likely can’t match. In 2020, Christian Brun, chief executive officer at executive search firm Wellesley, told Bloomberg that roughly 90% of the firm’s job placements in Hong Kong require Mandarin fluency—a qualification few Westerners can satisfy.

While Hong Kong’s economy more closely integrates with the mainland, banks and other financial institutions may place less value on employees who only speak English and instead favor those with the skills to interact with colleagues in the mainland and close deals in Mandarin.

No great alternatives

Singapore and Tokyo are often touted as alternatives to Hong Kong as Asia’s financial capital. But neither poses a realistic threat. Singapore is comfortable and cosmopolitan with a British-style legal system. The population is predominantly Chinese, but English is widely spoken. And yet, where Hong Kong is just across the border from China’s mainland, Singapore is a five-hour flight from the nearest Chinese city. The total market capitalization of Hong Kong’s exchange is about $5 trillion, seven times that of the Singaporean exchange.

Tokyo is capital of the world’s third-largest economy, home to the largest pool of pension assets after the U.S., and a leading source of direct investment. But any bid to create direct trading links between Tokyo and exchanges in Shanghai and Shenzhen would require support from Chinese financial regulators—an unlikely prospect. And to global bankers and asset managers, Japan’s high income taxes—the rate for the country’s top tax bracket is 55%, more than triple Hong Kong’s 17% flat tax—are an even greater scourge than Hong Kong’s dreaded quarantine policies.

On Thursday, Hong Kong Chief Executive Carrie Lam showed the first signs of a return to normal, reducing the city’s daunting three-week quarantine mandate for arrivals to two weeks.

“This certainly should help alleviate some of the stress on cross-border business operations and talent shortages due to the lockdown,” George Leung Siu-kay, CEO of the Hong Kong General Chamber of Commerce, said to the SCMP. Though David Graham, executive director of Hong Kong’s British Chamber of Commerce, told the SCMP that the reduction to 14 days “is just the start of what’s needed.”

When the pandemic passes and the city’s drawbridges are lowered, the banks will still be here. And the expats—so long as they’re unperturbed by Hong Kong’s slide down Freedom House’s rankings for civil liberties—may yearn to return, lured by the same low taxes and high standard of living that have always made Hong Kong an attractive capital for finance.

Never miss a story: Follow your favorite topics and authors to get a personalized email with the journalism that matters most to you.