Cryptocurrency is the newest asset class on the market, and there’s not much research on where it fits in an overall investment strategy.

For one, what is it? Crypto can be an investment, but you can also buy things with it. It operates independently from the equity markets, similar to an alternative investment like real estate or commodities, except that it’s also hyper-liquid: It trades 24/7.

“This is such a different asset class than anything we’ve ever dealt with,” says Adam Blumberg, a certified financial planner who founded Interaxis, which offers a digital asset certification and education for financial advisors.

But even if it’s hard to define, it’s harder to ignore. High fees aside, returns have been astronomical, even if they’ve been severely volatile. Bitcoin is up more than 400% from this time last year. Companies built on top of Ethereum blockchain are challenging the way the financial services industry looks and operates.

Many investors have treated crypto as a speculative investment: They throw anywhere from a few dollars to a few million into the more than 6,500 digital assets in circulation and track their gains and losses. But more and more, particularly with the approval of the first Bitcoin futures ETF, wealth managers are incorporating Bitcoin, Ether, and other cryptocurrencies into long-term investment strategies, as a way to hedge risk, boost overall returns, or add diversification. Some investors are giving digital assets their own allocation within a portfolio, just as they would with international equities or gold, and they’re periodically re-balancing those holdings.

The problem is there’s no consensus on where digital assets belong in a portfolio, nor what their underlying use case should be. It’s always a stretch to try to forecast how an investment or asset class will perform over time—and even more so with limited data: Cryptocurrencies have only existed since 2009, and institutions have only been actively trading them for a couple years now.

Inflation-ready

Before introducing any investment into a portfolio, it’s good to have a thesis for why it belongs there in the first place. For example, you may invest in certain equities, because you believe they will generate yield. Bonds may offer periodic, predictable income. Alternatives can diversify a portfolio and can help cushion it during a downturn.

Crypto is proving to have a wide set of use cases. Here are a few ways investors are thinking about it now:

–Long-term store of value: Investors who think some cryptocurrencies will maintain, or improve, their value in the long-run may wish to invest a large sum of money and hold it. They also may wish to make periodic, recurring investments.

–Inflation hedge for a portfolio: Investors who are concerned over the purchasing power of the U.S. dollar may want to allocate a portion of their portfolio with a currency that isn’t affiliated with it. However, the idea that crypto is a good hedge against inflation is not universally acknowledged.

–Risk hedge: Some investors use cryptocurrencies as a way to further diversify their portfolio, and protect from potential downturns in the U.S. equity market. That’s because crypto is not correlated with any government or institution.

–Method to boost returns: Considering that interest rates are so low right now, some investors are adding exposure to cryptocurrencies in an effort to improve their annual yields.

Depending on an investor’s strategy, she may want to purchase Ether, then hold it for 15 years. Alternatively, to hedge against inflation, it may make more sense for her to rebalance her ETH holdings each quarter (which means selling off some ETH should its value go up, or buying more if its value falls, in order to maintain a preset allocation). It’s all going to depend on the purpose of the investment, says Blumberg.

How do portfolios perform with BTC, anyway?

Despite the volatility and risk of holding crypto, some initial research has pointed to portfolios holding crypto doing, well, great.

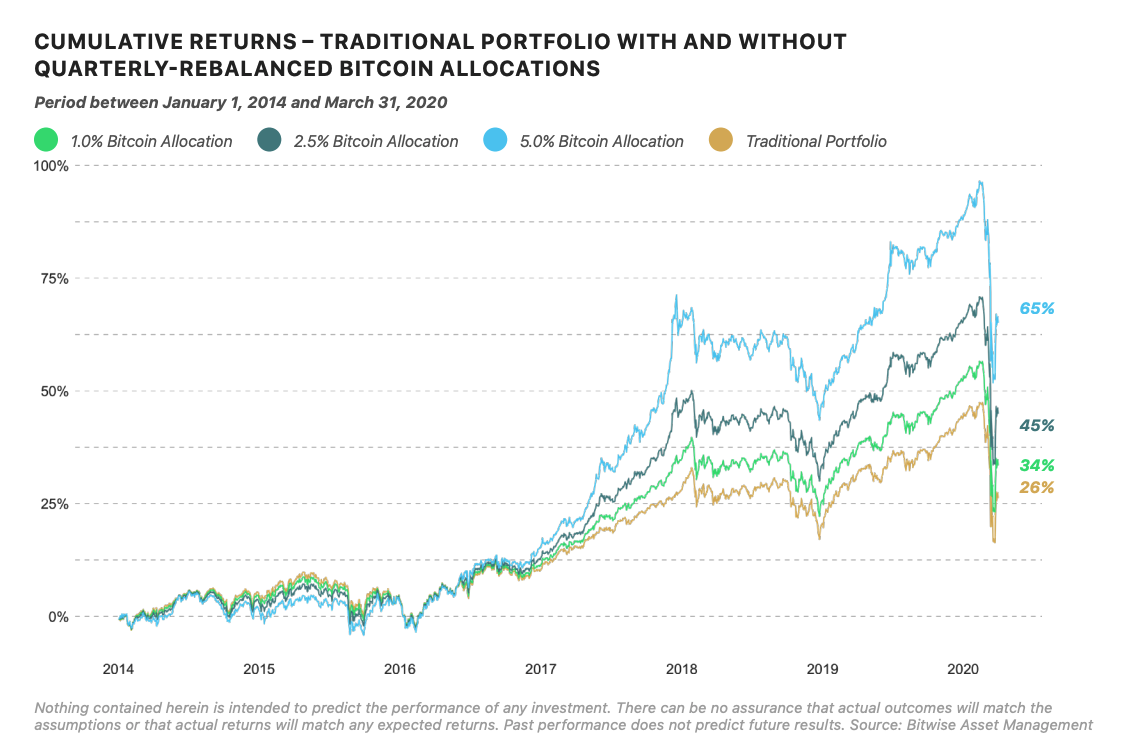

Portfolios that allocated 2.5% of their assets into Bitcoin would have improved their returns by 18.7 percentage points between Jan. 2014 and March 2020, according to research from Bitwise that evaluated 60/40 portfolios (meaning that they invest 60% of assets in equities and 40% in bonds). A 5% Bitcoin allocation would have doubled returns. Just a disclosure here: Bitwise has funds that offer exposure to cryptocurrency.

Here’s a look at Bitwise’s findings:

But it’s very important to keep in mind that there’s a lack of track record here, and it’s possible that things could go the other way. We only have 12 years of data on crypto—and much less if you’re looking at when major institutions started entering the market. Portfolio models have been carefully constructed using decades of market data, so it’s hard to say these charts will look so plump 10 years from now. There’s also the question over how regulators will get involved, particularly in the arena of decentralized finance (which could directly impact the value of ETH). There are a lot of question marks, and not a lot of data so far.

There is academic research that suggests Bitcoin or other cryptocurrencies shouldn’t be considered a replacement to any other asset class just yet—though it might be tempting. Research published in the Journal of Risk and Financial Management found that, while Bitcoin has thus far been “immune” to downturns in the economy and stock market and therefore been a diversifier, “it would be going too far to assert that Bitcoin can serve as an alternative asset due to its random spikes and movement in prices,” the report says. “Considerably more evidence in Bitcoin’s favor” will be necessary before considering it as an alternative to commodities or gold, the report says.

For those that are risk-averse, or nearing retirement, it may not be a good fit at all. That’s going to be up to each investor.

“It’s a whole lot of theory without nearly as much practice as we need,” Blumberg says.

WEEKLY CHART

Here’s a look at the number of active Bitcoin and Ether wallets over the last three years. Bitcoin is still, by far, the most widely held cryptocurrency.

JARGON, EXPLAINED

“Alternative investments”— Alternatives are non-conventional investments, so essentially anything that isn’t stocks, bonds, or cash. Financial advisors or wealth managers may invest somewhere around 15% of a portfolio into alternative assets: Things like hedge funds, private equity, real estate investments, or commodities (This, of course, depends on how much money you have to invest as some of them have high minimums). Alternatives help diversify a portfolio and make it less sensitive to equity market movements. Alternative investments typically tend to be more illiquid than stocks and bonds—unlike crypto, which is the most liquid of any asset class, because it trades 24/7.

DON’T MISS THIS

The first Bitcoin futures ETF—the ProShares Bitcoin Strategy ETF (BITO)—started trading this week, and it had a pretty impressive launch, becoming the second-highest traded fund ever on its first day. In other news, Fortune hosted its Most Powerful Women Summit last week. Make sure to read about why Goldman Sachs is investing in Black women, the emergence of Nasdaq onto the Fortune 500 list, and more on how the pandemic has cut into women’s stock market returns.

Have an investing query you’d like to see addressed? Send me your thoughts and feedback below. Thanks for reading.

Jessica Mathews

Twitter: @jessicakmathews

Email: jessica.mathews@fortune.com

More finance coverage from Fortune:

- 4 things to know about stimulus checks in 2022 and beyond

- GameStop report from SEC sheds new light on meme stock mania—conspiracies and all

- How high Goldman Sachs predicts home prices will go in 2022

- Mortgage rates may spike 30% next year, according to a new forecast

- These markets are expected to be the hottest for real estate in 2022

Welcome to The Dividend, Fortune’s new weekly investing column, available exclusively to subscribers. Each week we’ll dig into an area of the market that’s making headlines and help you figure out what deserves a place in your portfolio—and what doesn’t.