In Squid Game, the Netflix streaming series taking the globe by storm, 456 people in debt play deadly games for the chance to win $40 million and be freed of their financial burdens.

Seong Gi-hun (Player 456), the main protagonist, is a chauffeur and gambling addict who has racked up huge debt and owes money to loan sharks. His childhood friend Cho Sang-woo (Player 218) is on the run from authorities after pilfering money from clients during his tenure as the director of a securities firm. Before his downfall, Cho was the ideal young professional in South Korea—a graduate of the prestigious Seoul National University and his mother’s pride and joy.

The South Korean dystopian thriller is a resounding success, resonating with audiences worldwide. Squid Game is Netflix’s first series to reach No. 1 in all 83 countries where the streaming platform is available, according to analytics company FlixPatrol. And Netflix announced on Wednesday that the survival series has become its biggest series launch of all time—attracting 111 million viewers in 17 days.

Squid Game has amassed fans globally, but its themes speak directly to South Korea’s young generation—and the “get rich quick” schemes they’re embracing to combat the profound socioeconomic malaise they face in a prosperous but increasingly unequal society. As job competition, unemployment, and home prices soar, young South Koreans, like the Squid Game players, are also choosing quick paths to wealth—even if they come with big risks.

“Such a mentality is widespread in societies where opportunities for social mobility are limited,” says Andrew Eungi Kim, professor of international studies at Korea University. And in Korea, moving up the class ladder is seemingly impossible, he notes.

With homeownership and stable career paths further out of reach, “young people [have] developed a sense that there’s nothing left to lose,” says Jenna Gibson, a researcher and Ph.D. student at the University of Chicago, focusing on South Korean social and political issues and former director of communications at the Korea Economic Institute of America.

Such cynicism has steered young people to schemes that promise to make them wealthy fast like cryptocurrencies, says Gibson. Young people sinking money into mechanisms that dangle a potential windfall is “risky and the payoff is by no means guaranteed—but they still see it as more likely to help than vying for a traditional career within a hypercompetitive job market,” she notes. “I’m reminded of Squid Game, honestly.”

‘Dirt spoon’ generation

South Korean society has long subscribed to the “spoon theory,” whereby individuals born into wealthy families have so-called gold spoons, and those in the middle class hold silver spoons.

In recent years, more of South Korea’s youth are identifying as the “dirt spoon” generation, belonging to the low-income rung of society. Even members of the hugely popular South Korean boy band BTS were known as “dirt spoon idols” when they debuted in 2013, represented by a small, indebted entertainment firm (that is now a profitable public company whose October IPO made the band mates millionaires).

The dirt spoon generation has become more disillusioned under South Korean President Moon Jae-in. Moon rose to power in 2017 with young people’s support because his platform stood for social and economic equality, says Seoho Lee, an international relations fellow at Johns Hopkins University. Four years later, inequality, debt, home prices, and youth unemployment have skyrocketed.

Perhaps the most significant factor prompting young people’s disillusionment is the lack of affordable housing. In the capital city of Seoul, where half of Koreans live, home prices have more than doubled since Moon came to power. The average Seoul apartment now costs nearly $1 million, spiking 12% from January to September this year—the largest price surge in 15 years, according to Kookmin Bank.

For young Koreans, buying a home isn’t “just a part of the plan, it’s a must,” says Jon Sung, a 34-year-old South Korean working in the financial services industry. “It’s a kind of ultimate goal in our lives.” Korean society considers homeownership a prerequisite for marriage and starting a family, and a necessity for a comfortable retirement, Sung says. He recently moved to the U.S. to save up for a home in Seoul.

Yoobin Whang, a 30-year-old Seoul-based entrepreneur, has written off owning a home altogether. “It’s [near] hopeless to be able to buy a decent home with my own hard-earned money,” she says. “I’ll need my parents’ help to do so, and even then, buying a home won’t happen until later in my thirties, if not later.”

In addition to Seoul’s runaway home prices, growing unemployment rates have fueled this generation’s discontent. Since 2017, the number of unemployed or underemployed young people has grown every year, reaching a high of 27.2% in January 2021, despite South Korea having the highest share of young adults with tertiary education of all OECD countries.

In the post–Korean War era, South Koreans exhorted a good education as the key to social mobility. But high-profile scandals in which “gold spoon” families rigged the system in their children’s favor have undercut the belief that education is the great equalizer.

So, too, has the dearth of good jobs for university graduates.

“We have close to 70% of high school graduates enrolling in colleges, and our economy can’t offer enough jobs [to] meet the qualifications and demands of all our highly educated young people,” says Kim. “It’s a structural problem, irrespective of which party is in power.” As a result, young people are taking jobs they’re overqualified for, working part-time, or in temporary gigs, says Gibson. “The job competition is fierce, with a huge number of highly educated and qualified candidates competing for a small number of stable jobs,” she says.

Because of Korea’s inadequate pension systems, many older Koreans also “work way beyond retirement age, further [diminishing] the work opportunities for younger generations,” says Joanna Elfving-Hwang, associate professor and director of the Korea Research Center at the University of Western Australia. South Korea has the highest elderly poverty rate of all OECD nations.

‘Bittoo’: Borrowing to invest

Risky financial behavior has grown alongside the desperation of the “dirt spoon generation.”

Young South Koreans are now bingeing on debt for a chance to get ahead. The practice of “bittoo”—South Korean slang for borrowing to invest—among young people has taken off in recent years, and increased even more during the pandemic when the central bank eased lending rules.

As in many countries, Korea’s under-40 demographic takes out loans to pay for education or supporting an unpaid internship, says Elfving-Hwang. Bank loans for this age group have also increased as young people take on more debt to finance a home. Korea has coined a term, “yung-gul,” meaning people do everything they can, even sell their soul, to buy a home.

At the same time, a growing number of young Koreans are pouring their bittoo money into get-rich-quick schemes, such as cryptocurrencies, stock bets, and online gambling, in hopes of amassing enough wealth to buy a home. Borrowing to invest is considered a “quick way to make money,” says Kim. “[Young people] feel there’s no other way to improve their socioeconomic status.”

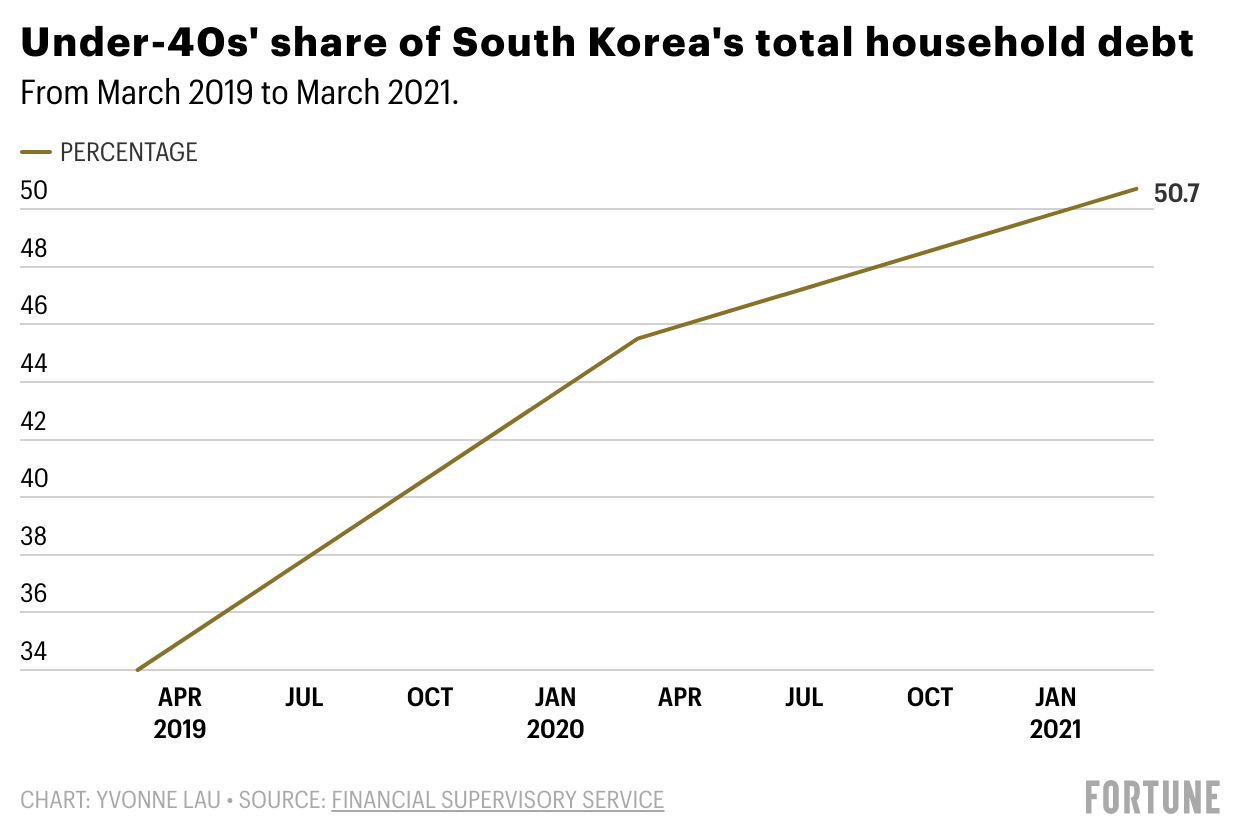

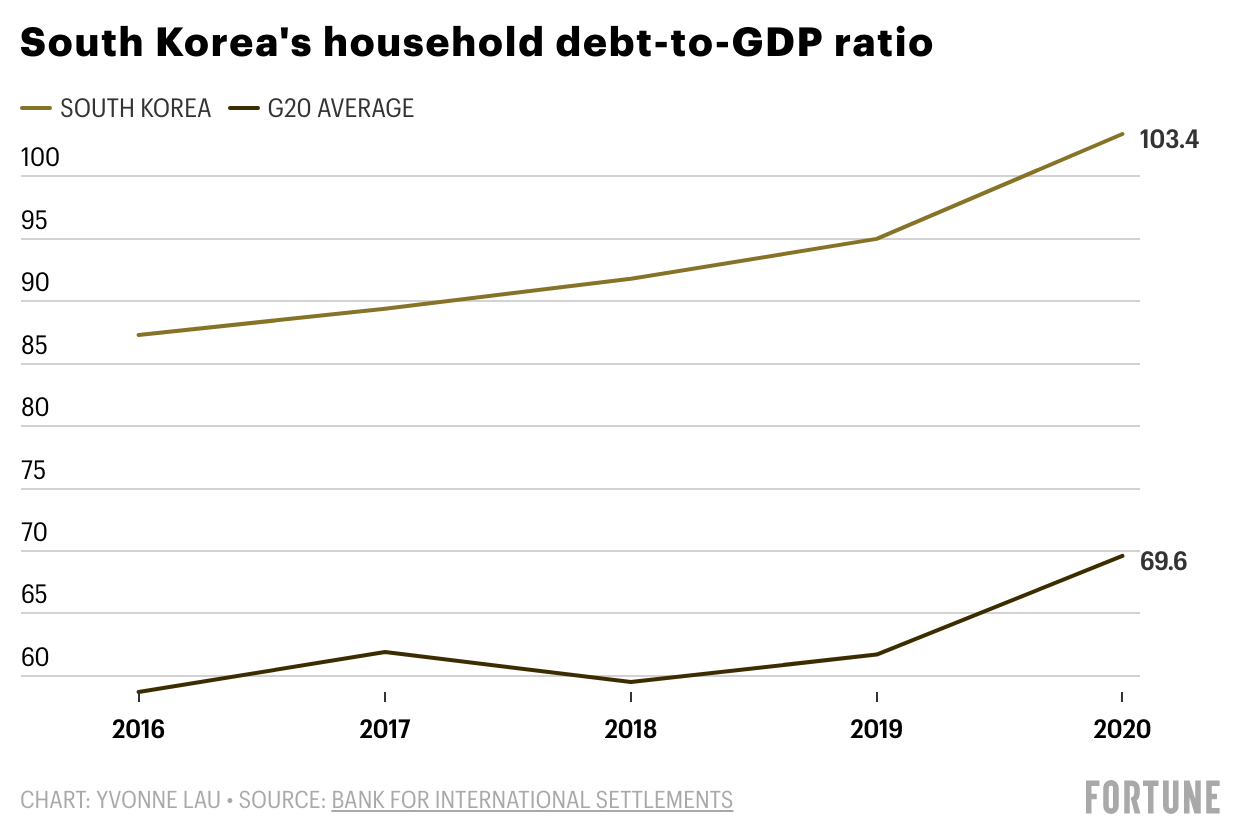

By the end of March, South Koreans in their twenties and thirties held a record $395 billion in loans, a 14% increase from the same time last year, according to the Bank of Korea. Those in their thirties have the most exposure, with their debt equivalent to roughly 270% of their annual income. This figure isn’t far off from other OECD countries—Canadian millennials for instance, have a 216% debt-to-income ratio—but young Koreans’ debt has exploded in recent years. Koreans under 40 now account for over half of the country’s household debt, up from 35% two years ago.

This year, people under 40 accounted for two-thirds of the 2.5 million new users on South Korea’s top cryptocurrency exchanges, according to numbers from opposition lawmaker Kwon Eun-hee. Since the country’s crypto craze first began in 2017, young adults have been the driving force behind the digital coin boom, with a growing number borrowing money to invest in the volatile asset, according to Korea’s Financial Supervisory Service (FSS). Central bank governor Lee Ju-yeol previously raised the prospect of curbing loans to ensure that highly leveraged crypto trading doesn’t spill over and disrupt South Korea’s financial system.

Young Koreans have also flocked to day trading. Known as “ants,” Korean retail traders bought more stocks in the first six months of 2021 than during the whole of last year. The majority of these traders, many of whom are new, are under 40 and also highly leveraged, says brokerage Korea Investment and Securities. Young ants are increasingly taking on more debt in hopes of seizing a stock market windfall. Those who are younger than 30 and trading on margin—using borrowed money to purchase stock—jumped more than 160% from late 2019 to September 2021, a twofold increase that was greater than any other age group, says the FSS.

And just like Seong, the Squid Game protagonist, more of Korea’s young people are turning to gambling—an activity that has long been viewed as the domain of older Korean men. Now, the majority of individuals with gambling addictions in South Korea are in their twenties and thirties, according to the Korea Center on Gambling Problems, with online gambling (which is illegal in the country) by far the most popular form of betting. Even teenagers are rolling the dice: Since 2015, the number of teens in Korea seeking help for a gambling addiction has increased more than 14-fold.

The government is worried about young people’s turn to risk and debt. The state looked to trim debt by introducing loan curbs in July, and the central bank raised interest rates in August, the first major economy to do so during the pandemic.

Now, authorities are reviewing additional regulations for nonbank loans as young people increasingly turn to alternative money lenders. Private, person-to-person lending startups have proliferated in recent years, and so have opaque money lenders, some of whom prey on young investors and charge exorbitant interest rates.

Young South Koreans don’t necessarily see their financial decisions as risky or an attempt to get rich quick, says Elfving-Hwang. Instead, they are making a conscious calculation that borrowing to invest in cryptocurrency and the stock market are more likely than the traditional path to give them the life they want. They’re simply ensuring the “best possible chance of success against all odds,” she says.

Squid Game creator Hwang Dong-hyuk, for his part, said in a CNN interview this month that the show is ultimately a personal story—and one about the winners and losers in South Korean society. The “winners level up,” he said, “[while the] losers, those who struggle through the challenges of everyday life…get left behind.”

Dive into stories from Fortune’s print edition:

- How one TikTok star went from living in his car to building a comedy career

- Oatly learns that it’s not easy being “green”

- Are women on a collision course with the COVID ceiling?

- Is the “unicorn” boom turning into a bubble?

- Daimler tackles the dirty secret behind clean cars

Subscribe to Eastworld for insight on what’s dominating business in Asia, delivered free to your inbox.