Thanks to forbearance programs, stimulus payments, a rapidly recovering economy, and even changing consumer spending and saving habits, Americans’ credit scores have continued to improve during the COVID-19 pandemic.

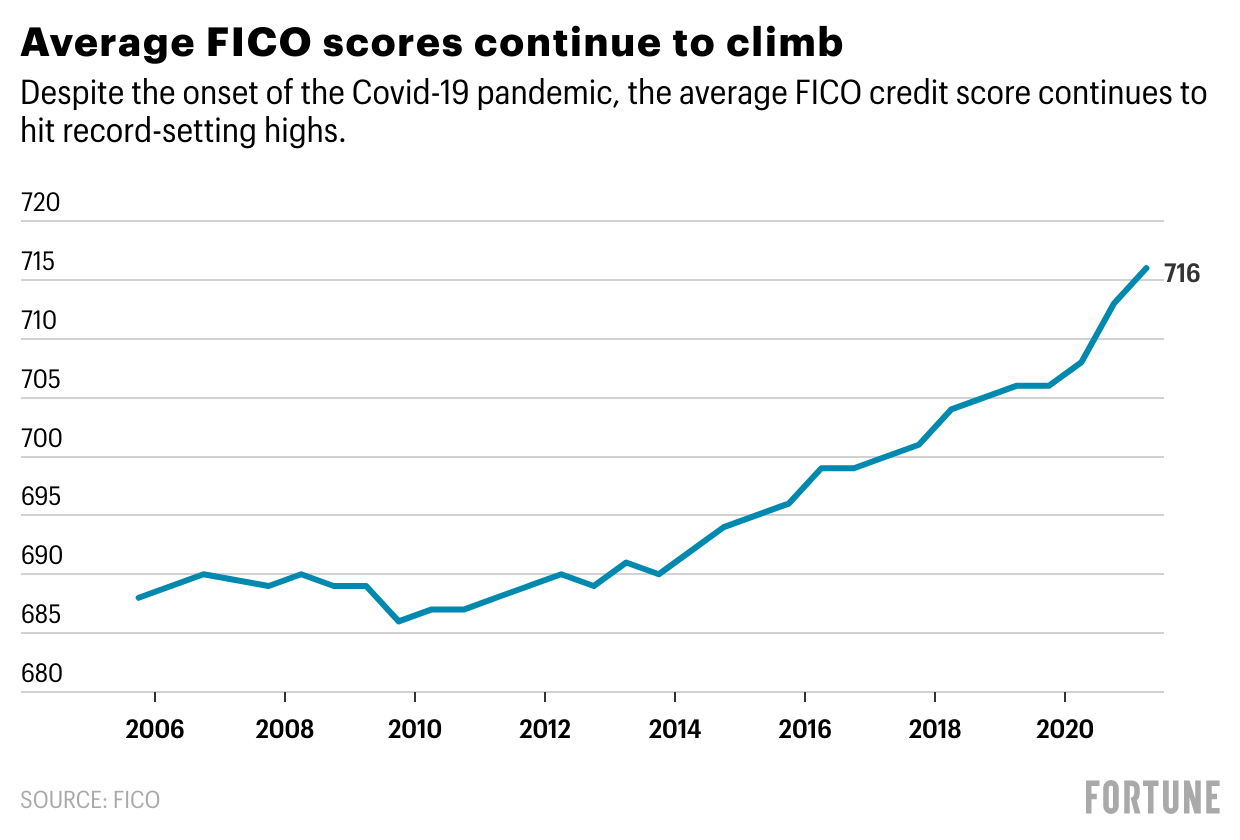

In fact, the average FICO credit score hit another record high of 716 in April, according to the data analytics and credit scoring company, which released the latest average score on Tuesday.

Americans’ FICO scores—which can range from 300 to 850—improved eight points from the year prior and are up three points from last fall, when the average score reached 713, according to Ethan Dornhelm, who leads the research and analytic development of FICO scores globally.

Dornhelm told Fortune the rising scores can be directly attributed to fewer missed payments, lower credit card debt levels, and changes in consumers’ behavior around credit. Just 15% of U.S. consumers had a payment that was past due by a month or more as of April. That’s down nearly 20% from the previous year. Additionally, FICO scores are not affected by certain credit issues when lenders flag that consumers are experiencing natural disasters, forbearance, or deferment.

And despite total U.S. household debt trending upward again this year, many Americans have actually paid down their debt, especially credit card debt. Although many Americans have taken out mortgages amid the boom in homebuying, credit card debt—which is a much bigger driver of credit scores—has been slower to rebound, Dornhelm said. FICO finds that as of April, the average credit card balance has declined by about 10%. That has a big effect on credit scores since about a third of the overall FICO score is based on credit card balances and utilization rates, Dornhelm added.

There’s no question that government programs such as extending forbearance options, pausing student loan payments, and providing stimulus checks helped many struggling Americans bridge the gap until the job market fully recovered, Dornhelm said. But a lot of credit scores’ improvement can be attributed to consumer behaviors such as using stimulus and child tax credit payments to pay down debt, he added.

In fact, much of the uptick in the overall average FICO score is coming from those with lower scores pre-pandemic. Consumers with scores between 550 and 599 saw the average score go up 20 points between January 2020 and April 2021, while those with good credit (scores between 750 to 799) saw virtually no movement.

“Consumers are materially better off financially now,” Dornhelm said of Americans’ financial habits. He believes that many Americans will be on stronger financial footing going forward, even once emergency measures such as stimulus payments and deferral programs halt.

That’s not to say all credit scores improved during the pandemic. About 17% of consumers with FICO scores experienced a drop in their score of 20 or more points between April 2020 and April 2021. And more may be on the way as mortgage forbearance, the student loan payment pause, and other payment deferral programs are set to expire in the coming months.

But Dornhelm says even with these programs expiring, he’s not expecting the average FICO score to decline dramatically. Take mortgage forbearance, for example. There are just under 2 million homeowners left in forbearance, but that’s only a small fraction of the more than 200 million consumers who have a FICO score, he said.

“There’s reason for optimism here, but guarded optimism,” Dornhelm said, adding that it’s difficult to predict the financial impact of the next few months amid surging COVID cases and uncertainty around whether additional federal stimulus or deferral programs are forthcoming.

More finance coverage from Fortune:

- What are stablecoins? Your guide to the fast-rising alternative to Bitcoin and Ethereum

- Adidas gives Reebok the boot. Will this go down as one of the worst sportswear acquisitions ever?

- As climate worries spike, green bonds are having a moment. Should you invest?

- The daunting challenge ahead for Disney CEO Bob Chapek

- Crypto platform offers $500,000 “bug bounty” to hacker for returning stolen assets

Subscribe to Fortune Daily to get essential business stories straight to your inbox each morning.