This is the web version of Bull Sheet, a no-nonsense daily newsletter on what’s happening in the markets. Sign up to get it delivered free to your inbox.

Good morning, Bull Sheeters.

Stocks on both sides of the Atlantic recovered nicely yesterday. Today, that rally looks uncertain. U.S. futures are off their highs, dipping into negative territory, following Europe lower, ahead of Fed Chair Jerome Powell’s testimony before Congress later today.

The big uncertainty can be found in the crypto corner. Bitcoin has sunk below $32K, down more than 20% in the past week. But that’s not the only thing worrying crypto watchers.

During its epic plunge yesterday, Bitcoin achieved something called the “death cross,” which sounds like some kind of 1970s Evel Knievel stunt that the TV networks refused to air. (Right about now, more than half the Bull Sheet readers are muttering, Evel Ka-who? Answer: watch this… and then let’s talk about creating an Evelcoin!)

The big takeaway: after this week’s swoon, Bitcoin is up about 11% for the year, underperforming the S&P 500 over that period.

Let’s see what else is moving the markets.

Markets update

Asia

- The major Asia indexes are bouncing back in afternoon trade, with the Nikkei up 3.1%, recouping most of yesterday’s losses.

- COVID-slammed India vaccinated 8.5 million people yesterday, a new record. Still, it would need to deliver 10 million doses per day to hit its goal of inoculating 950 million adults by December.

Europe

- European stocks were modestly higher out of the gates with the Stoxx Europe 600 up 0.1% in the opening minutes before dipping. Energy stocks were leading the way with tech and autos lagging.

- Shares in Volkswagen, owners of performance-car brand Porsche, were down 1.2% mid-morning. Porsche on Monday announced it will invest €100 million on the development of a high-performance battery cell to take on Tesla.

U.S.

- U.S. futures are struggling to build on yesterday’s rally. That’s after the Dow gained more than 550 points on Monday, and the small-cap Russell 2000 performed even better.

- Shares in MicroStrategy plunged 9.7% on Monday (it’s down in pre-market, too) after the company announced it had purchased yet more Bitcoin, taking its holdings to over 100,000 coins. MicroStrategy is in the true-believer camp, recently issuing junk bonds to buy crypto. Their next analyst call should be a fun one.

- Shares in Amazon were down 0.9% in pre-market trading as we come to the end of yet another Prime Day shopping bonanza. Historically, Prime Day has given the e-commerce giant a massive top-line boost.

Elsewhere

- Gold is flat, trading around $1,780/ounce.

- The dollar is up as, paradoxically, 10-year Treasury notes decline.

- In the last hour, crude went negative, with Brent trading below $75/barrel. On Monday, oil hit a two-year high.

- It’s been a crypto bloodbath with Bitcoin trading south of $32,000 this morning. But the biggest dog of all is Dogecoin, which, according to my crypto Twitter feed, was, at one point yesterday, trading 78% below the Elon Musk Saturday Night Live peak achieved just last month… C’mon, people. Elon wasn’t that lame! Okay, he was pretty lame.

***

Labor pains

Firstly, my apologies for yesterday’s essay. Due to formatting bugs, the FOMC winners and losers chart frustratingly wouldn’t render in the email version. I do have a fix. You can now find an intact version of that essay, chart and all, here.

This morning, let’s talk data.

You no doubt recall that, in December and January, the big market-moving data point was the size of the U.S. stimulus package—how many trillions could be packed into those spending plans to help the economy grow.

Then, in February and March, all eyes were on bond yields. Big spikes in 10-year Treasury notes sent stocks, particularly tech stocks, in retreat. At that time, with the vaccination drive in high-gear, economic recovery was more or less assured, and investor focus switched to any indication that borrowing costs—somebody has to pay for those trillions in stimulus spending—would rise in line with prices.

Which brought us to April and May. Real yields were up, but what about prices? For the answer, we were all fixed on inflation data—namely, CPI and PPI. Those figures, we were told, would give us the full picture on inflation and reveal the Fed’s likely path to tapering.

After last week’s FOMC meeting, the new focus is on… labor data. The health of the labor market should tell us something about whether or not inflation is—here comes that word again—transitory. If there’s a true war on talent then that should lead to a solid rise in wages, which will, in turn, push up prices for the things we buy.

So, the concern went from growth to borrowing to inflation to labor. Through it all, the big question has been: when will the Fed decide it’s time to shift policy to cut back on its money-printing and bond-buying?

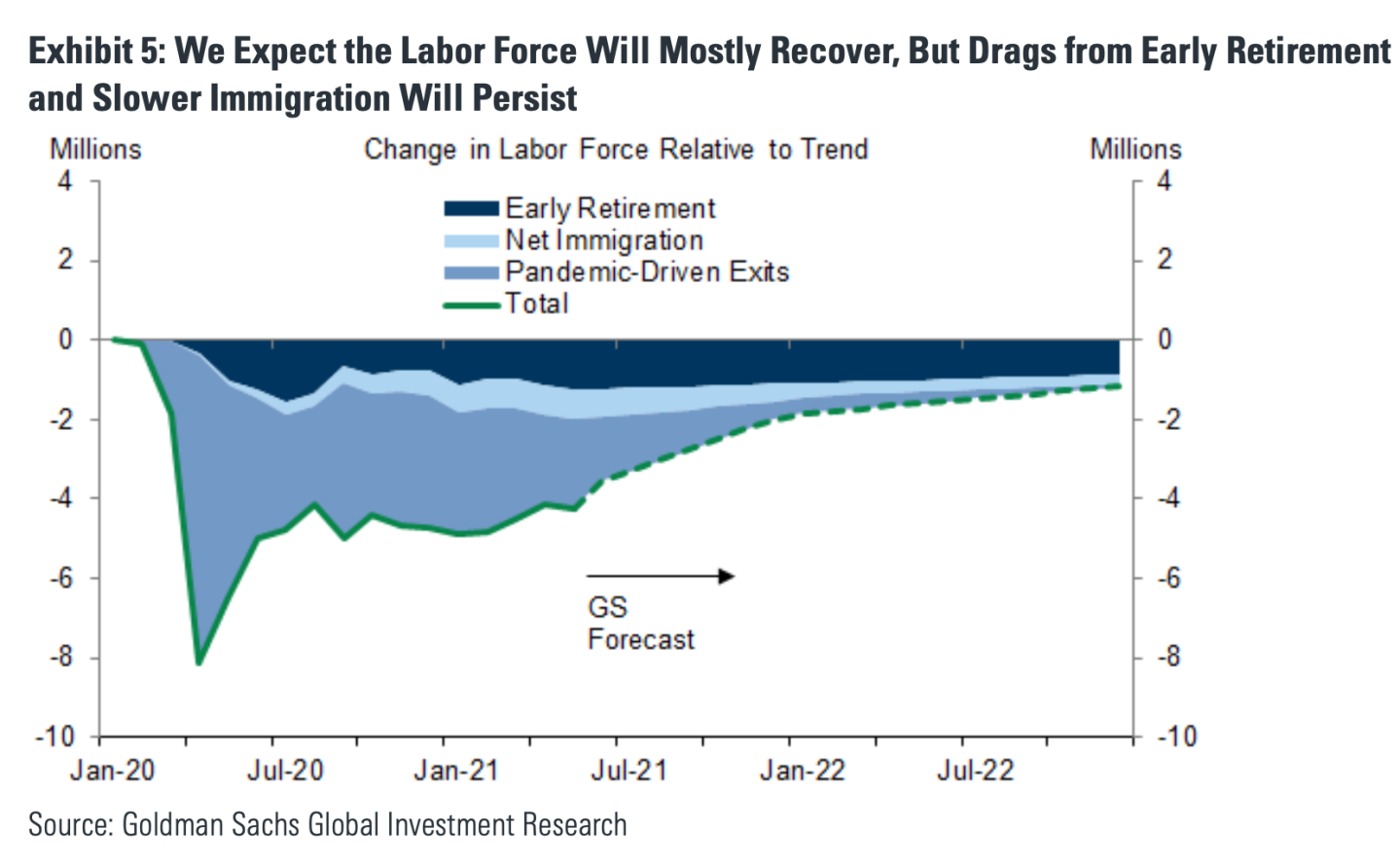

The speed of a recovery in the labor market is yet one more puzzle piece needed to tell us what is the Fed’s next step. According to a new Goldman Sachs report, the labor market is looking iffy. Specifically, the labor participation rate won’t return any time soon to pre-pandemic levels.

The problem is not those ex-workers who are sitting it out while they collect enhanced unemployment benefits, Goldman says. The issue is that older workers are leaving the workforce in larger numbers and that COVID-19 has walloped a vital and much misunderstood (by politicians, anyhow) sector of the labor market: immigrants.

“The collapse in immigration during the pandemic had less of an impact on the participation rate,” Goldman writes, “but has reduced the size of the labor force by an additional 750k workers today, of which a roughly 300k drag will persist. After adding this immigration hit to other drags, we estimate the labor force will remain over 1.2mn workers below trend by the end of 2022.”

The upshot is a tight labor supply will be with us for much of the next 18 months.

Economists warn that the removal of a sizable and reliable segment of the labor force carries all kinds of risks. It doesn’t just challenge a country’s competitiveness, it also creates, in the short term, a data headache. Economists are already divided on which numbers are permanent and which are transitory. That’s an unsurprising debate as you begin to emerge from a pandemic.

But what happens if the labor pool becomes permanently smaller?

That’s the new puzzler the Fed—and us investors—are trying to figure out.

***

Bernhard Warner

@BernhardWarner

Bernhard.Warner@Fortune.com

As always, you can write to bullsheet@fortune.com or reply to this email with suggestions and feedback.

Today's reads

Path to Zero. A new series of Fortune special reports is out today, this time looking at how businesses are leading in the fight against climate change. Our reporters go deep on e-waste, the rise of eco travelers and Starbucks' latest efforts to recycle its ubiquitous cups.

Eight crazy days left. Q2 ends on June 30th—just eight days away. What makes that point on the calendar so remarkable this year is that it will tell us whether Tesla ultimately needs to book a profit or a loss from its big bet on Bitcoin, depending on where the crypto coin is trading at that point. According to Shawn Tully's latest analysis, if it were to fall even a little bit lower, we could see a big impairment charge from Tesla.

Some of these stories require a subscription to access. There is a discount offer for our loyal readers if you use this link to sign up. Thank you for supporting our journalism.

Market candy

Quiz time

Even with the recent pullback, commodities continue to outperform this quarter. And energy tops the leader board. Crude oil is the top performer this quarter. What's No. 2? Is it...

- A. Corn futures

- B. Coffee

- C. Copper

- D. Gold

The answer is B, coffee, up 23.4% so far this quarter. Savor every sip, dear reader. ☕