It’s going to be a hot summer—for real estate that is.

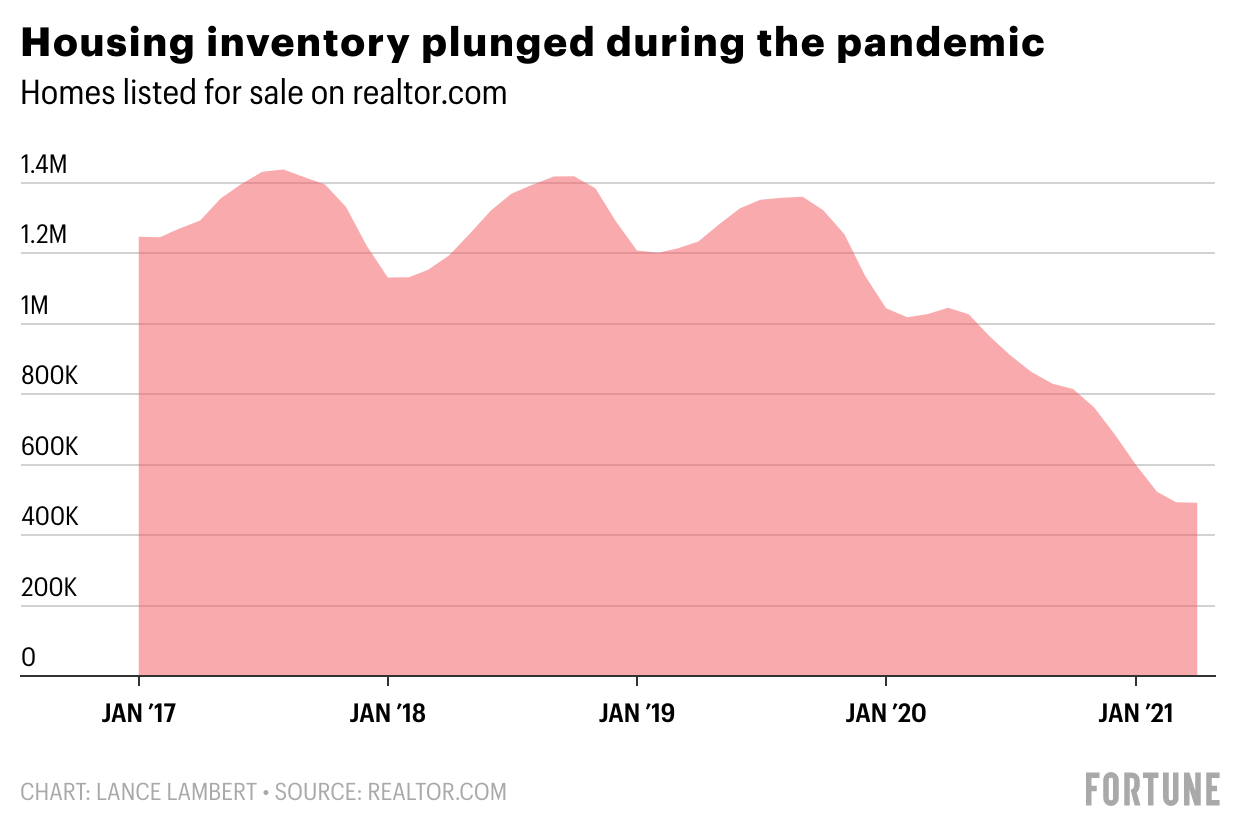

According to the National Association of Realtors (NAR), an astonishing 99% of metro areas saw year-over-year price increases in the first quarter of 2021. And 163 out of 183 metro areas tracked saw double-digit price increases. Meanwhile, according to Realtor.com, supply is at historic lows: The number of homes for sale is down over 50% since the onset of the pandemic.

“Significant price increases throughout the country simply illustrate strong demand and record-low housing supply,” said Lawrence Yun, NAR chief economist. “The record-high home prices are happening across nearly all markets, big and small, even in those metros that have long been considered off-the-radar in prior years for many home seekers.”

The downside? “The sudden price appreciation is impacting affordability, especially among first-time homebuyers,” said Yun. “With low inventory already impacting the market, added skyrocketing costs have left many families facing the reality of being priced out entirely.”

That said, mid-May brought a tiny sliver of hope for buyers: As Chris Morris wrote in Fortune, “New data from Realtor.com shows that price growth in the housing market, which has been soaring for almost 10 months, is starting to slow, hitting its lowest level in seven weeks. Year-over-year increases in home prices were actually down last week, marking a slowdown in a 39-week–long trend.”

“This week the housing market took a very tiny step in a buyer-friendly direction,” said Danielle Hale, chief economist at Realtor.com. “It is still solidly a seller’s market, with homes selling 28 days faster year over year for the week ending May 8. However, homebuying opportunities could be on the horizon.”

But hang on, why are real estate prices so strong coming out of a global pandemic?

As Fortune’s Shawn Tully explains, “The U.S. is riding the greatest housing price explosion since the height of the 2006 craze, setting a pace that’s due to hit the mid-teens by early spring, according to the American Enterprise Institute’s Housing Center. But this boom is a game changer, a completely different phenomenon from previous bull runs featuring super-low mortgage rates and slender inventories. In a historic turnabout that’s one of the biggest, most underreported stories of the COVID economy, expensive homes—which almost always lag in a surging market—are racing neck and neck with the sizzling low end.

“The reason: Affluent Americans who used to shop for move-up manses where they live and work no longer need to commute to an office complex and can work from anywhere. So they’re selling in San Jose, Seattle, or Chicago and buying a bigger, cheaper house in Phoenix or Boise or Cincinnati, where they Zoom with colleagues from expansive home dens, spend weekends poolside, and watch their kids frolic in a big backyard.”

How low is the housing supply?

Low. Really low.

Tully talked extensively with Ed Pinto, director of the AEI Housing Center, who stressed how much demand is outpacing supply. “Since January 2020,” Tully notes, “the number of homes listed for sale has cratered from 1 million to 600,000. ‘Months of supply,’ the time required to sell all listings at the current pace, has fallen in that period from 3.3 months to 2.0 months. That’s less than half the five-month stock that marks a balanced market. Remarkably, the number for homes in the medium-high category is a paltry 2.2 months, and the high end stands at 4.7 months, about half the 8.9 reading last April.”

Why is the housing supply so tight?

Tully explains that, “as America’s hunger for houses intensified, the stock of homes for sale kept shrinking. Pinto offers four reasons for the inventory crunch. First, older baby boomers in their sixties and seventies are staying longer in their homes instead of downsizing to apartments, in part because the pandemic makes having space for hosting the family so attractive. Second, in places like the Carolinas and Texas, where building has been relatively plentiful, it’s been taking longer and longer to get land zoned and approved for new construction. Third, severe land use restrictions in the Northeast and much of the West continue to keep a tight lid on fresh supply. Fourth, COVID magnified the damage from those barriers by shutting down construction for a couple of months in the spring and summer.”

It’s also the result of demographics: In 2019, the country began the five-year period when people born between 1989 and 1993—the biggest birth years for millennials—will turn the all-important first-time homebuying age of 30. Builders knew for years this was coming, however, the aftermath of the subprime mortgage crisis had put many of them out of business—and the surviving firms became too risk averse to invest heavily in future trends.

That demographics wave, coupled with low mortgage rates, has only worsened the housing shortage.

Okay, but seriously, what is going on with lumber prices?

If you’ve seen the meme of two well-dressed people eating a fancy dinner with the caption “Take me someplace expensive”—and the background is the lumber aisle of a superstore—you have some idea of how out of control lumber prices have gotten. As Fortune’s Lance Lambert has been assiduously reporting, it has been “pure panic” as builders wrangle for supply.

On Tuesday, the price per thousand board feet of lumber soared to an all-time high of $1,359, according to Random Lengths. Since the onset of the pandemic, the price of lumber has skyrocketed 280%.

As Lambert wrote recently:

“For weeks, Fortune has relayed a similar message to readers: The price of lumber is likely to continue posting new all-time highs this spring. To the ire of homebuilders and DIYers alike, that prediction continues to be right. And signs point to this all-time high soon getting topped too. On Tuesday, the July futures contract price per thousand board feet of two-by-fours jumped $63 to $1,481. That squeeze is a result of homebuilders scrambling to get lumber for upcoming summer projects they already have on the books.”

“The fact is that we are in the midst of a global supply shortage for all forest products, and pure panic is accelerating the pace of demand. Additional supply cannot and will not be added fast enough to allow for sustained price deceleration in the coming year,” Kyle Little, COO of Sherwood Lumber, told Fortune on Tuesday.

This unprecedented mismatch in lumber supply and demand was ushered in by the pandemic. During the early days of the crisis, sawmills halted production and unloaded inventory. At the same time, bored quarantining Americans rushed to Home Depot and Lowe’s to buy up materials for do-it-yourself projects. But before sawmills could respond to that uptick in demand, another demand spike took place: Recession-induced, record-low interest rates helped spur a housing boom. That boom, which is exacerbated by the largest cohort of millennials starting to hit their peak homebuying years, is drying up existing home inventory and sending buyers in search of new construction. As of March, new housing starts are at their highest level since 2006. And those new homes require lots of softwood lumber.

Why can’t sawmills just make more?

Lambert asked this question recently: “Why can’t sawmills—enticed by sky-high prices—just start producing more? Well, lumber producers only have so much capacity—and increasing it requires both time and confidence that future sales will remain high. That means the best chance for lumber prices to correct in the short term, Little says, would have to come from slowing demand. However, despite all-time-high lumber prices, neither home construction nor home renovations have showed signs of cooling off.”

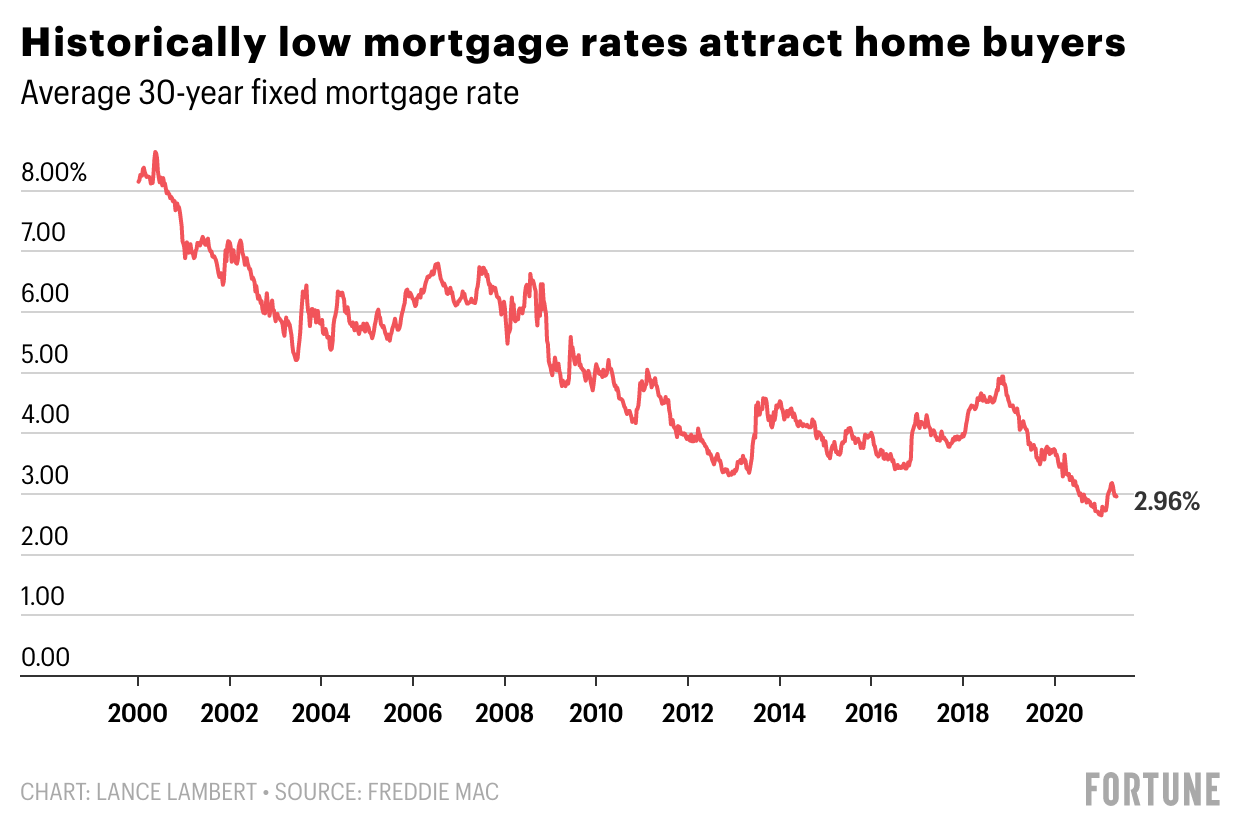

Where are mortgage rates headed?

Up.

According to the National Association of Realtors, “as a result of soaring home prices, the average national monthly mortgage payment rose to $1,067, up from $995 one year ago. This increase exists even as the effective 30-year fixed mortgage rate decreased to 2.93% in the first quarter of 2021 (3.57% one year ago).”

But now some analysts predict mortgage rates may be heading higher too.

Over the past year median home prices are up 16%, however, much of that cost was offset by historically low rates. But as rates rise and tight inventory pushes homes prices higher, monthly mortgage payments will shoot up fast. Ali Wolf, chief economist at Zonda, estimates that by 2022 mortgage prices will be 26% higher than they are now.

Will housing prices keep going up?

As Tully writes, “The big question is whether increasing mortgage rates will flatten the HPA (home price appreciation) curve or send it downward. The 30-year benchmark has already vaulted from 2.65% in early January to 3.25%. Pinto believes that if rates reach 4%, national prices will keep rising in the high single digits. ‘It would take over 5% to end the party,’ he says. ‘We’re nowhere near that now.’

“The spike in the 30-year, he says, will show no effect in April and May, because those deals are already done. So for those months, prices should keep rising in the 13% to 14% range. But the higher rates will start to bite in late May and June. By then, appreciation should slow to 9% to 10%, says Pinto. ‘That’s still a very fast pace, much faster than at any time in the last 10 years, except for the recent increase in rates,’ he adds.”

Bottom line? It’s still a seller’s market, but there could be some relief for buyers within sight.