Our mission to make business better is fueled by readers like you. To enjoy unlimited access to our journalism, subscribe today.

Just over a decade ago, Uber cleverly combined existing technologies into an on-demand taxi service. Without a confluence of necessary building blocks—such as app stores, geolocation tools, digital payments, and smartphone-wielding masses, to name a few basics—ride-hailing would never have been a viable business.

Similarly, a raft of new technologies springing from the cryptocurrency world is coinciding with a peculiar set of macroeconomic conditions, like rock-bottom interest rates and mounting inflation fears, to create a moment ripe for—in this case, financial rather than logistical—innovation. One company that’s seizing upon the situation is Eco, a startup that’s building a personal finance app for saving and spending money.

The Uber comparison is apt. Garrett Camp, the Uber cofounder and board member who came up with the idea for that business, advises Eco as a board member, and his startup studio, Expa, is an investor. While Camp earlier dreamed up Eco as a global cryptocurrency project in 2018, his team later abandoned that vision and offered up the brand to another company in which it invested, called Beam.

Like other fintech startups, Eco aims to lure people to its mobile app by offering high-yield savings and cash-back rewards, among other perks. The “streamlined approach to payment and savings” using a single digital wallet offers people an option “that is more functional and fair[er]” than the status quo, Camp told Fortune in a statement.

Camp, apparently undimmed by the big pivot, said the Eco app “has incredible potential.”

Beam me up, Scotty

That view is shared by others. Eco, né Beam, said Friday it raised $26 million in new funding spearheaded by a16z Crypto, the cryptocurrency-focused investment fund of Silicon Valley venture capital firm Andreessen Horowitz. Other investors in the latest round include Founders Fund, Activant Capital, Slow Ventures, Coinbase Ventures, Tribe Capital, Valor Capital Group, and an assortment of 100 other funds and angel investors.

“People are tired of janky apps for financial products,” says Kathryn Haun, the Andreessen partner who led the deal. She compared the appetite for new fintech products today to the reception that Uber received when it launched. “People didn’t want to have to go call a number to hail a cab and go stand on the street corner,” Haun adds, saying there’s a similarly “hungry market” that Eco will tap.

“The parallel I draw is to the 1970s,” says Andy Bromberg, who went from advising Eco to becoming its chief executive in October. In response to the so-called stagflation fears of the ’70s, an abundance of financial alternatives that offered better yields and rewards flourished, including the development of money-market funds, cash management accounts, and a boom in credit card adoption.

“All these products started to emerge because people needed alternatives to passbook checking accounts, and I think we’re at that kind of generational moment right now,” says Bromberg, who previously helmed CoinList, a fundraising platform that specializes in “initial coin offerings.”

Snipping the safety net

While the national average interest rate on savings accounts is 0.07%, according to Bankrate, a personal finance firm known for its industrywide surveys, Eco is offering yields of 2.5%, or up to 5% with friend referrals, on deposits. For comparison, the highest yield savings accounts available among top challenger banks tracked by Bankrate, like Goldman Sachs’ Marcus, come in under 0.6% today.

Eco can offer much higher returns because it isn’t a traditional bank. The service keeps people’s money stashed in either U.S. dollars or USDC, a U.S. dollar-backed “stablecoin,” meaning a cryptocurrency that’s designed to maintain a fixed price, unlike highly volatile Bitcoin. Then Eco lends those funds to over-the-counter cryptocurrency trading desks, like Genesis, and lending platforms, like BlockFi, to reap high yields.

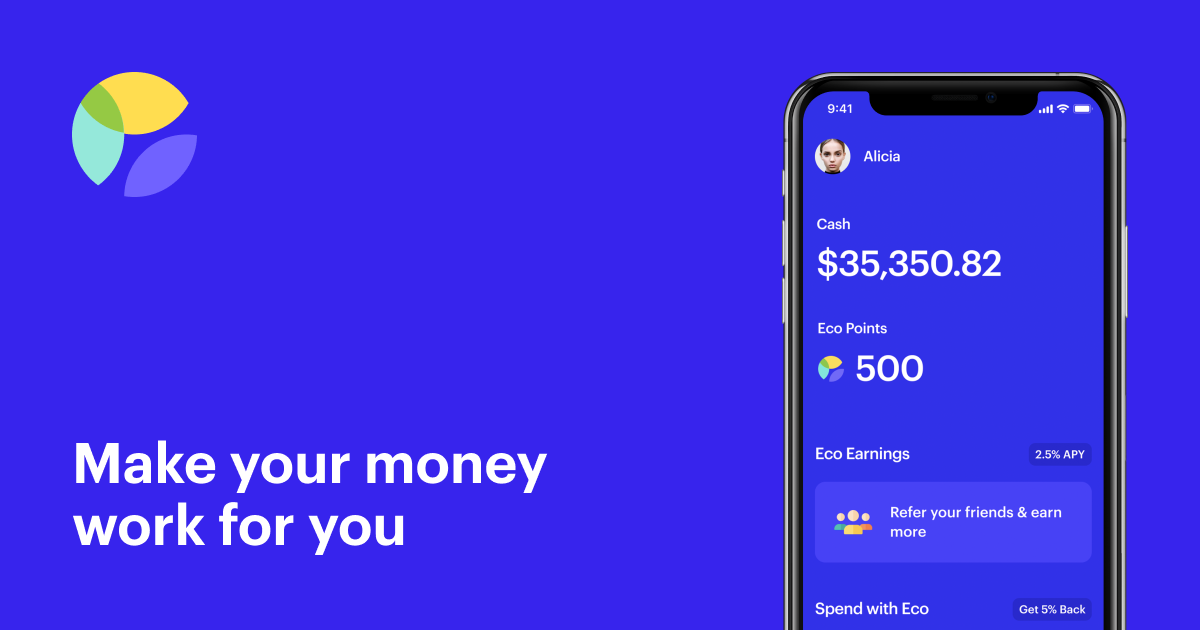

A view of the Eco app on a phone screen that shows an example of cash balance and loyalty points. Courtesy of Eco

The returns are “not subsidized by us,” Bromberg says, meaning the company isn’t spending all its new venture capital money on customer-luring handouts. Nor is Eco dabbling directly in the high-flying world of decentralized finance, or DeFi, where many unproved cryptocurrency projects advertise big returns.

That doesn’t mean Eco is without risk. Accounts are not insured by the Federal Deposit Insurance Corporation, which backstops bank accounts up to $250,000. Some people may be uncomfortable with the tradeoff.

But Bromberg argues that FDIC insurance isn’t all it’s cracked up to be. “I think there’s a little bit of like a trick that’s been played here, playing on people’s psychology,” he says. “We’re living in a negative real yield environment, or close to it. FDIC insurance ensures that you will keep the same number of dollars in the event of a banking collapse, but it does nothing for the value of those dollars.”

In other words, rising inflation could eat away at people’s wealth, regardless of how much money people think they’ve squirreled away. Such insurance guarantees “play on people’s loss aversion,” Bromberg continues. “You’re being shut out of the upside in exchange for this kind of psychological safety net.”

Scoring loyalty points

When money-market funds first came about in the 1970s, people gravitated to them because they offered higher yields. The desire for return overrode people’s fears about lack of FDIC insurance. Eco hopes to tap that same vein.

Around the same time that money-market funds took off, money-market accounts—which are, in contrast, FDIC insured—became popular only after banks and credit unions started offering people the ability to write checks against them. To extend the analogy: Eco is again taking its cue from history by integrating payments.

As a draw, Eco is offering 5% cash-back rewards when people shop at Amazon, Uber, DoorDash, and more. In time, Eco plans to expand on the feature set. Bromberg says the company expects to add more merchant integrations and spending perks, and “soon” allow people to “pay bills, pay friends, and much more.”

Loyalty points are planned to be a major part of Eco’s, well, ecosystem, too. The app showers people with so-called Eco points for their saving, spending, and friend referrals. “They don’t do much today, but one day they will,” teases a blog post, noting that it seeks to “make these Points as useful as possible over time.”

“We’re kind of explicitly not sharing every last detail of the full vision, but all the pieces are there,” Bromberg tells Fortune. The inclusion of loyalty points can be viewed as a sort of Trojan horse that injects a cryptocurrency-like system into the app in everything but the name. It’s a rather ingenious conceit, given that loyalty points are better understood by consumers and face less regulatory pushback.

To date Eco has raised $35 million in total, including the most recent round of funding. An early version of the Eco is available in 40 or so states across the U.S., and people can sign up to join its wait-list here.

More must-read tech coverage from Fortune:

- You aren’t alone: Why Americans will receive 48 billion robocalls this year

- Instagram’s new streaming feature looks a lot like Zoom

- Can we really banish email from the workplace? Author Cal Newport says yes

- How Microsoft plans to give virtual reality apps a big boost

- PlayStation is killing its on-demand video service