I’ve been wondering if it would actually happen. For the first time in more than seven years, the Shiller price/earnings ratio, or P/E, is flirting with its long-term average. This could be a signal that, at long last, the overall market—in its coronavirus-driven collapse––is now a good buy.

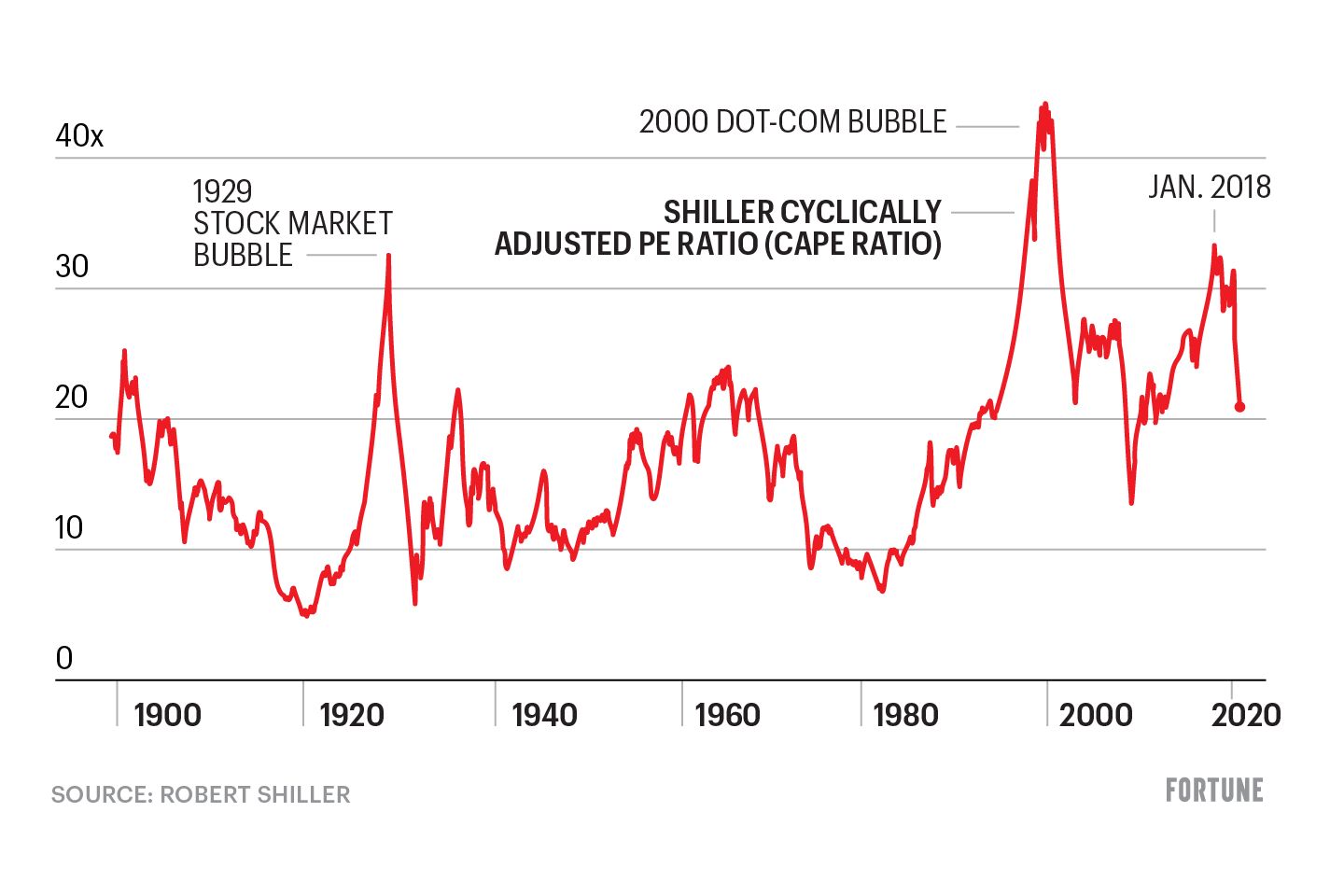

This event could prove a landmark, because Robert Shiller, the Nobel Prize winner and Yale professor, offers what’s arguably the best yardstick for measuring whether stocks are cheap, expensive, or sit somewhere in the reasonable range. Shiller calls his famed metric the CAPE, for cyclically adjusted price/earnings ratio. The CAPE’s beauty is that unlike the standard P/E, it doesn’t rely on the most recent annualized earnings numbers reported over the past four quarters. Using current profits as the denominator is highly misleading, because that formula inflates the P/E in an earnings recession, when stocks are actually bargains, and understates how rich they really are when profits hit unsustainable lofty levels.

Instead, Shiller calculates an average of inflation-adjusted earnings over the past 10 years. That provides a truer reading of value because it takes out the careening swings that distort P/Es based on current earnings.

Recently, corporate profits reached an unsustainable bubble, making stocks look like pricey but not excessively so, when in reality they were really, really expensive. As we’ll see, the CAPE didn’t make that mistake.

Over the past 50 years, the median multiple on the CAPE is 20.3. Based on Shiller’s adjusted earnings number of $107 per share, the S&P would reach 2172 at its normal long-term valuation ($107 in EPS multiplied by 20.3). On Monday, March 23, the S&P closed at 2237. At that point, the index sat within less than 3% of what might be termed a key benchmark for the CAPE. At midday, the difference was less than 1%. Remarkably, the S&P was 1.5% higher at the close on the day Trump was elected, Nov. 8, 2016, than what could be considered today’s fair value.

It’s instructive that two things occur when the CAPE soars over 25, which is almost 20% above the half-century median. First, it always falls back through that 20-plus mark at some point in the future, and second, that fall may take a long, long time. For example, the CAPE neared 25 in January of 1966, and stayed in the low-20s until mid-1969.

The CAPE then languished in the low-double and single digits until 1995, when it finally climbed back to 25. It stayed above that level until it collapsed during the financial crisis starting in 2008. It wasn’t until August 2014 that the CAPE hit 25 again, and it remained at rarefied heights in the high-20s and low-30s until early this year. At the end of February, it stood at 30.8, 52% above its historic reading of 20.3.

The coronavirus pandemic unleashed the deepest, quickest drop in the CAPE’s history, bringing it back to that 50-year benchmark on March 23. That the selloff led markets to what could be called a “normal” level, based on the CAPE, casts doubt on the view that shares are now radically underpriced. You never know how long it will take for an elevated CAPE to wend its way back to 20.3. But it always gets there. It may well be that this historic plunge simply got us back to a place where we should have been all along: fair value.

More must-read stories from Fortune:

—Why the extraordinary dollar surge spells more trouble for the global economy

—These estimates of how much COVID-19 will hurt the economy are terrifying

—The NYSE is closed because of the coronavirus. What that means for investors

—How thinking like a golfer can help you ride out market mayhem

—Listen to Leadership Next, a Fortune podcast examining the evolving role of CEOs

—WATCH: The U.S. tax deadline has moved from April 15 to July 15

Subscribe to Fortune’s Bull Sheet for no-nonsense finance news and analysis daily.