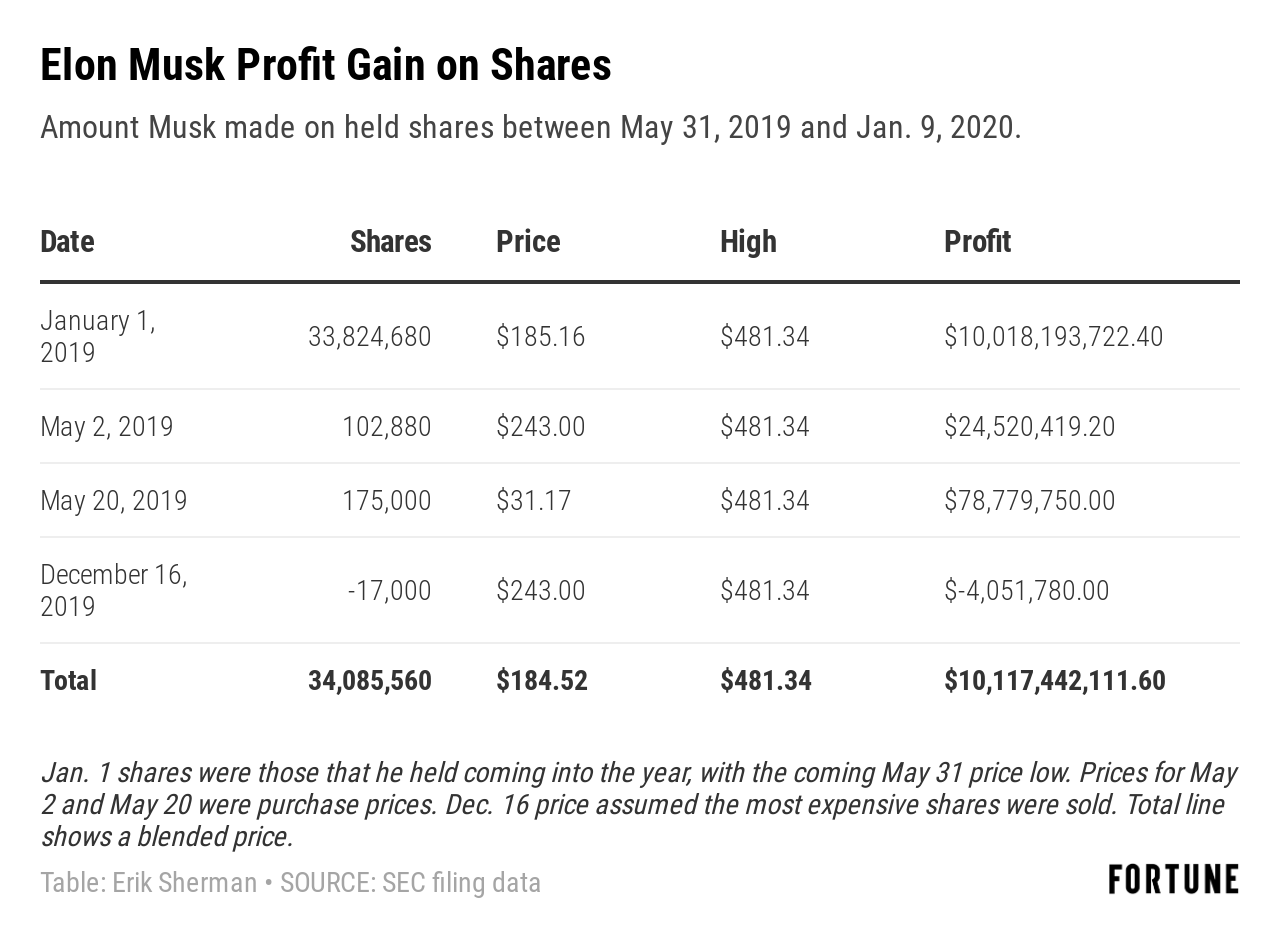

By the summer of 2019, some Tesla insiders had spent the previous 18 months selling off parts of their holdings to pocket millions. The stock, battered, sunk to a low of $185.16 on May 31.

But that was then. Shares have been consistently hitting new highs because of record vehicle deliveries last quarter and the start of production at the company’s factor in China. The stock closed on Thursday at $481.34, and those who held on made a boatload. CEO Elon Musk himself saw his paper profits hit $10.1 billion.

On the flip side are the short sellers—Musk’s nemeses who reaped profits during troubled periods for the car company, like when Musk got in trouble in 2018 for talking about taking the company private on Twitter and when he gave a revealing interview in the New York Times. The ensuing share slide netted the shorts a $1.2 billion gain. What has driven their zeal is a belief that Tesla lacks the production capability, cash flow, and profitability to sustain the massive valuations it’s been bestowed by the markets.

Right now, they’re wincing at their losses. But there’s a showdown still to come.

First, Musk. A Fortune analysis of Securities and Exchange Commission filings show he personally came into 2019 with 33,824,680 Tesla shares. He then purchased multiple times that amount in May as shares were falling in price and heading to a low. The purchases included a bundle of 102,880 shares at $243 each (buying at market rates as Musk likely tried to show confidence as share prices were slipping) and another 175,000 shares at a $31.17 option price. In December, Musk gave 17,000 shares to a charity, although the filing didn’t indicate the recipient. (Tesla did not respond to a request for the name of the charity before publication.)

To figure out how much Musk made since that 2019 low point, Fortune took each block of shares and multiplied the number by the share price appreciation between purchase date and January 9. For the bulk of the shares he came into 2019 with, the initial price, for the sake of consistency, was set to the low on May 31, 2019. The two sets of shares purchases in May were valued at their purchase prices, of course. Then Fortune subtracted the gift of 17,000 shares from the number of highest-priced shares. The table below shows the data.

The results showed Musk with a gain of $10.1 billion—$10,117,442,111.60 to be exact. It put his total “paper” wealth, based only on shares of Tesla and ignoring any other assets, at roughly $18.6 billion.

One potential drawback for Musk is that, according to the 2019 proxy statement, he has pledged 13,394,056 shares as “collateral to secure certain personal indebtedness,” or something under $6.4 billion. Still, quite the bump for the auto executive.

Selling Tesla short

Then there are the short-sellers.

The idea behind shorting stock is that investors can potentially make money through a speculation or hedge that the share prices will fall. The individual or institutional investor borrows shares, sells them, and watches the price. If it drops significantly, they purchase replacement shares for less money, returns the borrowed shares (with additional payment to the lender, who also wants a profit), and pockets the difference.

When share prices go up, however, the shorts lose money because it costs more to replace the shares. As the price keeps climbing, so do the losses. In theory, the amount of loss is unlimited.

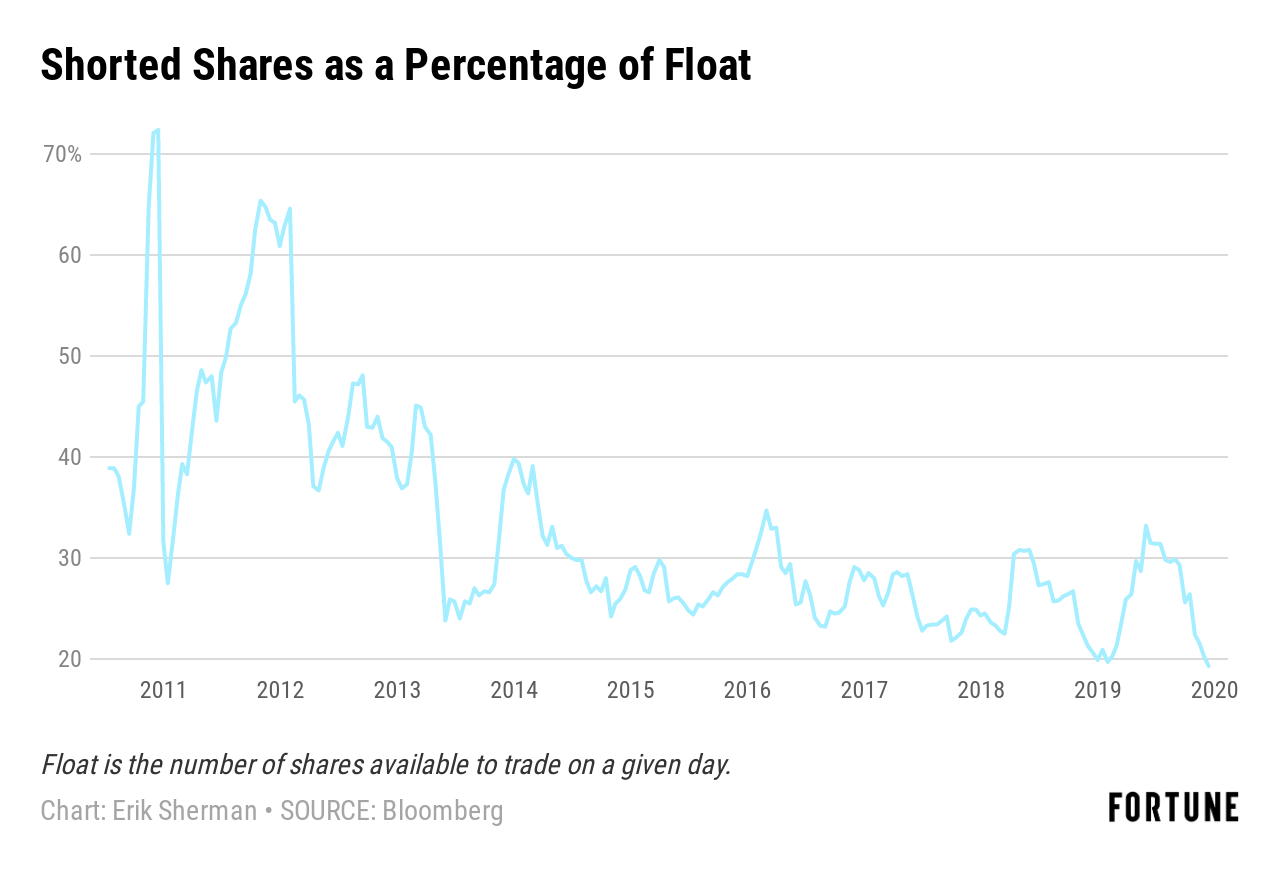

Early in Tesla’s history as a company, shorting was more popular than today. The graph below shows the number of shorted shares (called the short interest) as a percentage of shares outstanding (the number of shares available for trading).

For those who have been shorting Tesla lately, losses have piled up as shares have climbed since early December 2019. According to the most current data from Bloomberg, the short interest are at 27.5 million, or 15.3% of total shares outstanding. (Data is released every two weeks.) That was down nearly 1.2 million from the previous two-week period.

Every dollar over the price at which investors shorted costs short sellers a dollar a share, or $27.5 million given the number of shares shorted. For example, between Monday’s close of $451.54 and Wednesday’s record high of $492.14, shorts collectively lost more than $1.1 billion.

“I put on a small short condition [Wednesday] that for an investment firm my sons and I run,” Brad Cornell, emeritus professor of finance at UCLA and managing director at global consulting firm BRG, tells Fortune. “We thought at $488 it was so wildly overvalued, how long could it go on?”

Given that his short position was on 1,000 shares and Wednesday closed at $492.14, that was a loss of $4,140. By the end of Thursday, however, Cornell and his sons were instead up $6,570 because the share price dropped to $481.34, which was below their purchase price at $488.

For a person or organization with a large portfolio, the shifts may not matter practically. However, it’s always possible to get a margin call, which means whoever has the short position must make up the difference between it and the current state of the shares. Call it a hedge on a hedge.

Cornell took a $500,000 short position on Tesla with a $25 million portfolio. “There’s cash in there and other things that cover the margin,” he says. “Even if this went to $750 [a share], we wouldn’t get a margin call but we’d have a very unpleasant loss of $260,000.”

The irony is that covering margin calls and closing short positions means buying stock, which increases demand and can help push share prices higher. Some of the pressure has likely come off over time. On October 15, 2019 the short interest was almost 37.2 million, according to Steve Sosnick, chief strategist at Interactive Brokers. The share price was $257.89.

“If those shorts hadn’t covered, they would be looking at a … loss of over $8 billion today,” Sosnick said in a message to Fortune. “Obviously many of those shorts covered, bringing the short interest down to 27.5 million only two months later.”

“Remember, there’s got to be a buyer for every seller,” Cornell says. “Musk owns a lot of stock and he’s not selling. You have a bunch of investor fans and they’re not selling. You’ve got to induce people to sell. That takes a bit of a run up in price.”

Sosnick thinks that pressure is limited. “The net buying of about 10 million shares is a drop in the bucket for a stock with average daily volume of about 6 million shares per day,” he says. “The real trigger for Tesla’s rally was a set of market friendly announcements that turned into a massive momentum rally.”

Despite the current highs, fueled by devoted investor-fans of the brand, the stock has seen big swings and the company has some critical fundamental weaknesses, making Tesla attractive to shorting. But as Cornell asked, how long can that go on?

That brings everyone back to the big question of how long the rally can last. Between Wednesday and Thursday, shares dropped 2.2% even though the Nasdaq, where Tesla is listed, was up about 0.8% over the same period.

Cornell, for one, is not giving up. At a current market cap of $95 billion, Tesla has to grow insanely to gain the revenues and profits its market size would seem to promise. “This company has to be as profitable as Porsche and as big [in sales] as VW in ten years so it has the huge cash flows in the future to justify the [current] market cap,” he points out.

The shorts may need the nerves of a race car driver to see that reality play out. And Musk? He’s got a lot of reason to break into dance.

More must-read stories from Fortune:

—Nissan-Renault became a ‘masquerade of an alliance,’ according to Ghosn

—Investors see a 2020 recession coming—but think they’ll make money

—Investors shrug off Iran concerns, analysts find the complacency ‘disconcerting’

—Laws meant to close down tax havens and shut loopholes could have opposite effect

—What a $1,000 investment in 10 top stocks a decade ago would be worth today

Subscribe to Fortune’s forthcoming Bull Sheet for no-nonsense finance news and analysis daily.