Three and a half years ago, Emma Heathcote-James was looking to expand her business beyond Britain.

Her 11-year-old Little Soap Company was selling bath products through major supermarkets and pharmacies across the U.K. The next step was obvious. Using neighboring Ireland as a starting point, the company would enter the rest of Europe.

The vote for Britain to leave the European Union in June 2016 brought those plans to a screeching halt. As the value of the pound plummeted after the referendum, imported products—including essential oils—became more expensive, pushing up costs by 5% in the first week.

The Little Soap Company managed to absorb the added expense, but its export expansion plans evaporated.

“Everyone we’d been chatting to went quite quiet,” she says.

Heathcote-James considers Little Soap lucky compared to others, however. In the years since, the business, headquartered in the idyllic Cotswolds region, has expanded into new stores domestically; and its customers and manufacturing are both based in the U.K., which insulates it from the bigger risk that products won’t be able to cross borders to reach end users if there’s no U.K.-EU trade deal after Brexit.

But the lack of clarity and communication from the government on how to prepare for a post-Brexit Britain is frustrating.

“Small businesses need certainty, and we’ve just been hanging in limbo,” Heathcote-James says.

Political paralysis over an exit from the EU has gripped the world’s fifth-largest economy for three years and counting; the U.K. is still figuring out whether it will leave the EU on October 31, and if it will do so with or without a deal.

That is only the most recent deadline; the first of March 29 was extended, as Parliament repeatedly failed to agree on a plan for the country’s departure. After those setbacks, former Prime Minister Theresa May resigned and was replaced by Boris Johnson, who has vowed to take Britain out of the EU by the end of October—even if that means the country crashes out with ‘no deal’, reverting to World Trade Organization trade rules.

But under Johnson, Parliament has only fallen further into chaos, as Members of Parliament ruled out a ‘no deal’ scenario, and Johnson suspended Parliament—a move the U.K. Supreme Court later declared illegal.

All the while, the prospect of Brexit has jammed the gears of British businesses—large and small—as its many unknowns have smothered investment growth, hampered productivity, and sidetracked valuable executive time, all for a vision of post-bloc Britain that’s nearly as unclear as it was immediately following the vote.

“Nobody’s doing anything, because nobody knows what to do,” Heathcote-James says.

‘Brexit hasn’t helped’

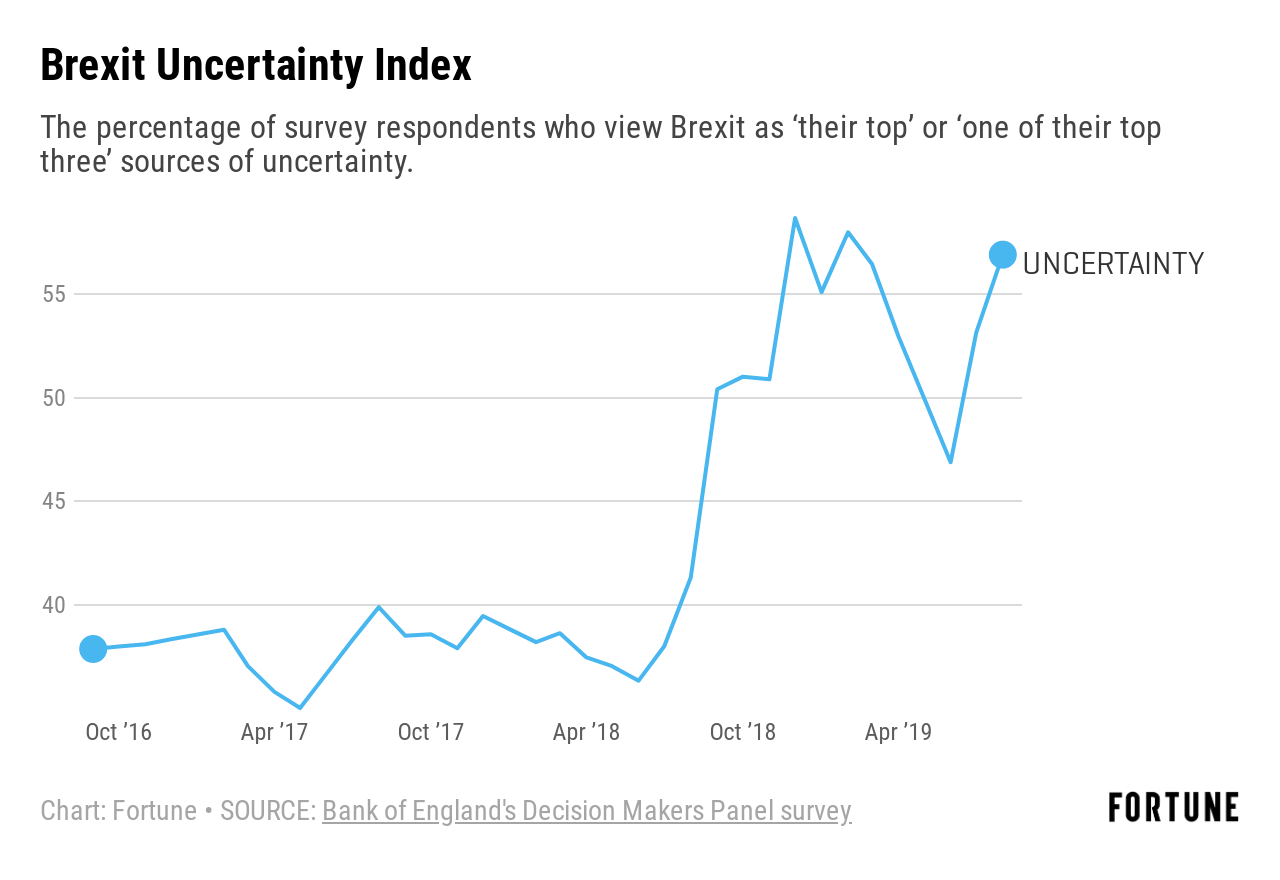

As far as shocking economic events go, the Brexit vote stands out as historic.

Not only was the vote to leave the EU largely unexpected—two-thirds of polls predicted Britain would vote to remain—but the uncertainty has lasted longer than anticipated, says Paul Mizen, a University of Nottingham professor and an author of an August 2019 study on the impact of Brexit on British businesses.

“If you look at a shock that’s parallel, the only real [comparable] shock is 1929,” says Mizen, whose study used Bank of England data collected from businesses starting in August 2016. The 1929 financial crash was quickly compounded by tariffs and protective measures ahead of the depression of the 1930s, he says.

In the three years since the Brexit vote, investment growth was 11% lower than it would have been had voters opted to remain, the study says. Meanwhile, productivity declined as much as 5%, largely due to executives diverting several hours a week to Brexit planning.

Brexit isn’t wholly to blame. The shift away from diesel cars in the U.K.’s sizable auto market, as well as pressure from e-commerce on traditional retailers have accelerated since 2016, resulting in falling revenue for companies in both sectors. But “Brexit hasn’t helped,” says Mizen.

The U.K.’s split from the EU has yet to be consummated, but it’s already spawned myriad costs for companies, like opening offices in other countries to keep a foothold in Europe, and stockpiling inventory ahead of Brexit’s initial March deadline—and again ahead of the upcoming October 31 cutoff. Plus, it’s hit businesses by way of investments not made, open jobs not filled, and expansions pared back.

“To some extent, this is something that’s affecting the firm’s ability to compete with its rivals overseas,” Mizen says.

‘The Brexit disease’

Two years ago, Lucideon—a U.K. materials consultancy with 24 million pounds in revenue—started working with the regional government near its Stoke-on-Trent headquarters to open a research center for advanced technical ceramics. The material, unlike decorative ceramics, is used to make components in everything from mobile phones to airplane engines.

The research center was to be a 40 million pound investment, and Lucideon was looking to invest up to 10 million pounds of its own money. But when the U.K. didn’t exit the EU in March 2019 as planned, the meetings started going nowhere.

It has “just not happened,” says Lucideon CEO Tony Kinsella. “That’s because almost every meeting gets changed,” as Brexit diverts the government’s attention and time, he says.

Meanwhile, Lucideon—which got 40% of its revenue from the EU ten years ago—was undergoing a shift. Since the Brexit vote, it has expanded, but mostly in the U.S. and Asia. Now, about 20% of its revenue comes from Europe, far behind the U.S.’s 35% share.

“The Brexit disease has not stopped the business investing,” Kinsella says. “It’s just shifting where we’ve chosen to put that money.”

Even so, preparing for Brexit has cost Lucideon a hundred thousand pounds so far. For instance, it’s opened a Dublin office as a gateway to the rest of the EU market. And in the case of a no-deal Brexit, it would lose its certification as a European Notified Body—a standing that allows it to declare products to be in conformity with EU rules—which would deal another blow to its revenue.

Kinsella is optimistic that the business will be fine post-Brexit. But three years of anticipation and deadline delays has been draining.

“It’s death by a thousand cuts,” he says. “For all the Westminster political shenanigans, I think the nation wants another three-, four-month extension [to EU membership] like it wants a hole in its head.”

Staying mum

While many large companies have reassured clients and shareholders that they have prepared for Brexit, few appear willing to discuss the impact it has already had.

One prominent trade association told Fortune that, in the highly polarized debate around Brexit, many of its members don’t want to run the risk of losing customers by speaking out about potential downsides. (The association asked not to be named in order to candidly express such views, which were spoken in private.)

Of the 17 U.K.-based companies on Fortune’s Global 500 list, all but one either declined to comment or did not respond to Fortune‘s inquiries. Several companies said they had decided not to speak about Brexit at all. (The one company that did comment—mining giant Rio Tinto Group—said its operations are all outside the U.K. and so didn’t expect to be affected.)

However, some hints of Brexit paralysis are evident. When HSBC—No. 90 on the Global 500—launched a billion-dollar buyback in August, Chief Financial Officer Ewen Stevenson said the move was “appropriately conservative given Brexit uncertainties”—meaning it might have been bigger if the environment wasn’t so shaky. And in February, Barclays—No. 336—said it had set aside $195 million to cover potential problems arising from a “hard” Brexit, in which the U.K. would lose easy access to the EU’s single market.

One trickle-down effect of Brexit uncertainty that’s likely to hit firms of all sizes is the shift in consumer sentiment. Though surprisingly robust immediately after the 2016 vote, British demand for products and services has waned in subsequent months.

In September, market researcher YouGov said consumer sentiment in the U.K. was at a six-year low; IHS Markit reported a six-year high in household concern over personal finances; and the Confederation of British Industry said retail sales remained weak, after dropping in August at the fastest pace since 2008.

‘Is it really worth it?’

When Britain voted for Brexit in June 2016, John Davidson, the finance director of London-based Tom Brown Wholesale Florists, knew it would be a major threat to the flower business.

With about 15 million pounds in revenue and four locations countrywide, Tom Brown imports almost all of its flowers through the EU—mostly through the Netherlands, Europe’s flower hub, including flowers originally imported from South America and Africa.

After the vote, costs immediately jumped as the pound weakened, pushing up the price of flowers—measured in industry parlance by the stem—by as much as 20% by the end of the year. In the first half of 2016—before the Brexit vote—Tom Brown had seen customers buy 6.5% more stems compared to the same period in 2015. Sales in the second half, after the Brexit vote, went in the opposite direction, falling 7.3%.

In the following years, flower sales fluctuated alongside British politics: picking up in late 2017 as a Brexit deal seemed imminent, getting stronger in 2018, and then flattening out in 2019.

In his key London store location, Davidson says he’s paused hiring for now: in recent months, he says the warehouse feels quieter and deliveries have slowed down.

Currently, Tom Brown can order fresh flowers from the Netherlands by 11 a.m. and receive them about 12 hours later—and that’s what customers expect, Davidson says. Brexit could cause delays and additional costs, largely due to reams of paperwork required to import flowers that previously needed only a simple order request.

“The newer generation of florists are fewer and far between,” he says. “And some of that uncertainty is making the older generation of florists think, ‘Is it really worth it?’”

Fighting off ‘Brexit fatigue’

There are other signs that the last three years have taken a toll, across hiring, recruiting, construction, and real estate.

In September, specialist recruiter SThree reported a 7% drop in quarterly net fees—the fees recruiters collect for successful placements—for its U.K. and Ireland unit, after reporting a 12% drop in the previous quarter. Meanwhile Staffline, a major contract-worker agency, issued a profit warning due to reduced demand, noting that its customers were reducing their exposure to temporary labor from the EU.

Some companies—especially in tech—simply can’t attract applicants when they want to hire.

Neil Ross, the lead on Brexit policy at industry association techUK, said one member of the organization, a data center operator, recently told him it had attracted no job applicants from mainland Europe in the last two years.

“Being able to recruit talent is fundamental to companies’ ability to expand,” says Ross.

Meanwhile, construction and infrastructure services company Keir Group warned in September of flat revenue due to clients putting off key decisions on projects until they know what’s happening with Brexit.

And real estate services company CBRE estimates the value of commercial real estate will fall by 3.8% in 2019 due to investors’ wariness over when Britain will leave the bloc and what the departure will look like.

Still, the lengthy duration of the Brexit uncertainty has prompted some companies to move forward regardless, says Miles Gibson, executive director of the U.K. research team at CBRE.

“There is no doubt that people are getting a bit of Brexit fatigue, and making decisions anyways, because they can’t wait,” he says.

For Heathcote-James of the Little Soap Company, refocusing the business on its existing U.K. market has pushed her once-ambitious export plans into the unknowable future.

“That’s on pause for the moment,” she says. Still, she remains hopeful. Even in Brexit Britain, “everyone needs a bar of soap.”

More must-read stories from Fortune:

—10,000 jobs on the line as HSBC mulls its future in Europe

—Hong Kong’s mask ban pits anonymity against the surveillance state—The world’s biggest turbines and no subsidies: how offshore wind is entering a new era

—The global phenomenon of “American Sriracha”

—Plant-based meats have huge potential in China, but Beijing wants a homegrown champion

Catch up with Data Sheet, Fortune’s daily digest on the business of tech.