We’re more than nine years into a bull market, and it’s no secret that stocks are expensive. The Shiller price/earnings ratio, which compares companies’ share prices with their inflation-adjusted 10-year earnings average, is at 31, well above the historical median of 16—a sign that future returns will be sluggish. Combine that with simmering worries about trade wars and inflation, and you get a climate in which fewer investors are clicking the “buy” button.

Yet there’s one group purchasing company shares with gusto: the companies themselves. As the impact of new tax cuts circulates through corporate balance sheets, businesses are getting an infusion of cash, and much of the windfall is going toward buying back stock. J.P. Morgan estimates that repurchases in 2018 will jump 51% from last year’s mark, to $800 billion, which would be a single-

year record.

Historically, buyback announcements have attracted investors like a plate of snickerdoodles does a kindergartner. Repurchases reduce the number of shares outstanding, giving each remaining shareholder a bigger share of future earnings—and thus making price appreciation more likely.

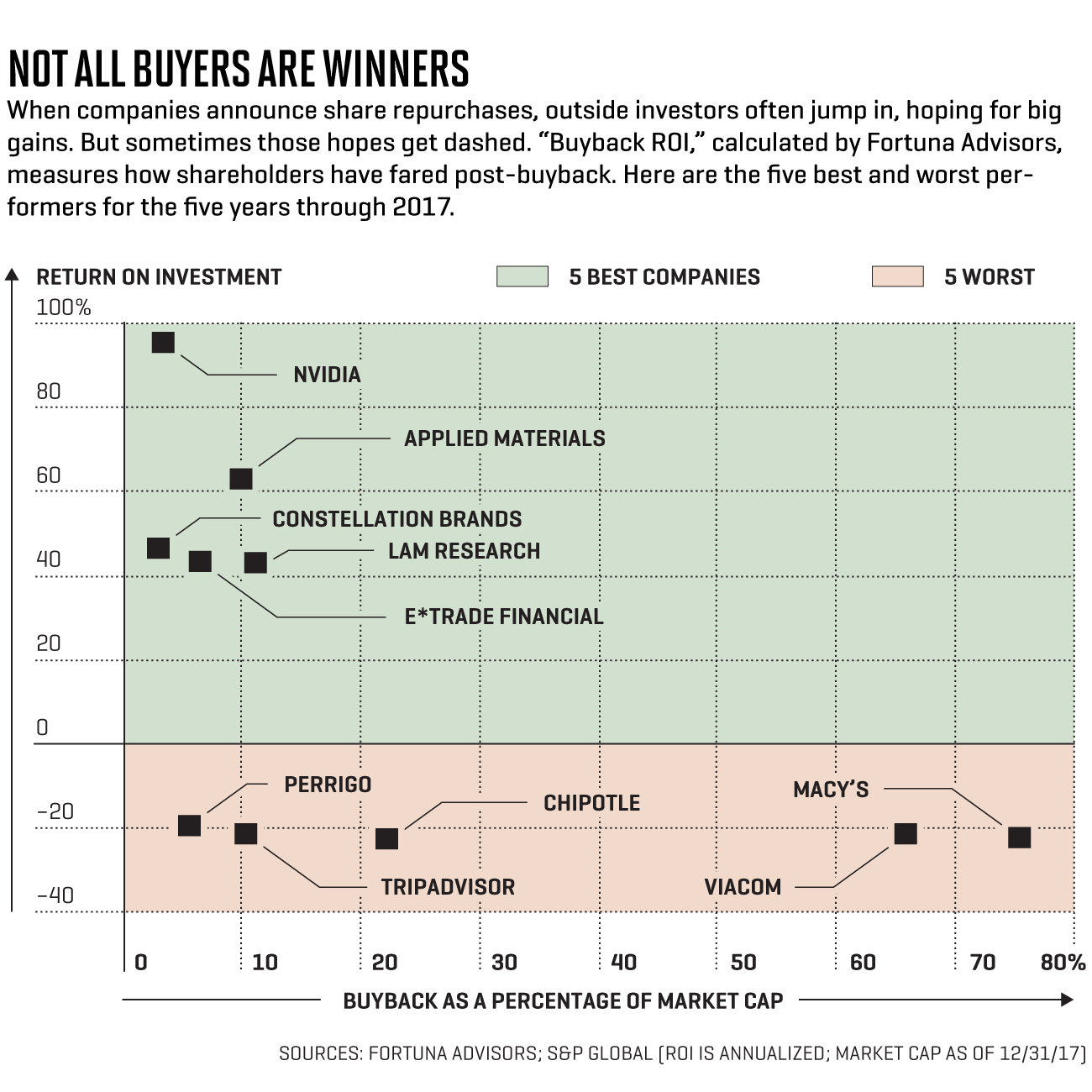

That’s the theory, anyway. But for many companies, it hasn’t quite worked out that way, says Gregory Milano, CEO of financial consultancy Fortuna Advisors. Since 2011, Fortuna has calculated a “buyback ROI,” or return on investment, which tracks post-buyback stock prices and other data points to measure the effectiveness of corporate repurchases. And over the five years through 2017, the 353 companies that spent significantly on buybacks underperformed the market on average. Their median ROI was 13.8% annually, including dividends, while the S&P 500’s return was 15.8%.

Fortuna Advisors, a financial consulting firm that compiles a buyback scorecard, has a particularly sobering assessment of the strategy’s effectiveness. (To see one of Fortuna’s most recent buyback reports, click here.)

Why the meh results? Critics point to a misallocation of capital: Money spent on buybacks is money that isn’t invested in projects that fuel longer-term success. For his part, Milano notes that the main factor in an effective buyback is simply good timing—and low ROIs often signal that the company bought at an expensive markup. Case in point: Chipotle, which landed dead last on Fortuna’s list. The company spent heavily on share repurchases in the first quarter of 2016, at the height of the fallout from its E. coli scare. But even then, the stock had a sky-high valuation, and shares have fallen further in the interim, giving the company an ROI of minus 23%.

How to confront this conundrum?

With stocks in general still trading so high, investors are best off ignoring the short-term hype around buyback announcements and instead taking a closer look at companies on repurchasing binges to see if their share prices have more room to run. Here are three that fit the bill.

As part of a three-year, $1.2 billion campaign, Foot Locker bought back $300 million worth of shares in the third quarter of 2017. The company got them cheap, because the stock was near the bottom of a fall of more than 60%. The cause? Nike, which accounts for about 65% of Foot Locker’s inventory, had a number of underperforming product lines in 2017. But analysts predict a comeback for the retailer. “Foot Locker should certainly benefit” from better-selling Nike footwear and clothing lines hitting the market this year, says Wedbush’s Christopher Svezia. And it’s a savvy way for investors to tap Nike’s growth, too, since its stock trades at a discount of more than 40% to the athletic giant’s.

Boeing has been feeling turbulence from the tariff battle between President Trump and China: About 25% of Boeing’s airplanes go to Chinese buyers. But the benefits of recent tax cuts may more than offset any trade damage. One vignette of the tax impact: When developing the 787, Boeing wrote off the expense at the then-prevailing 35% tax rate; now that it’s selling the planes, it owes tax of only 21% on the profits. Boeing recently announced an $18 billion repurchase program, and thanks to a thriving airplane market, there’s a “buying environment” for the stock, says Cowen analyst Cai von Rumohr.

Digital-memory specialist Micron Technology was one of Fortuna’s better buyback ROI performers—and though its most recent repurchasing campaign tailed off at the end of 2016, it’s still worth a look. Its performance has long been tied to Apple’s iPhone, which uses its chips for short-term memory. But last year, Micron began reaping more revenue from cloud computing. And the arrival of the faster wireless protocol known as 5G is expected to create even more demand for its products. “5G could move Micron out of the Apple cycle,” says SIG analyst Mehdi Hosseini.

At today’s prices, investors may want to simply stay out of the repurchasing game. One company that has done the same: Charles Schwab, which hasn’t done a buyback since the Great Recession. As its balance sheet recovered, Schwab reinvested heavily in technology and in its consumer bank, Schwab Bank—which has gone from $49 billion in assets in 2010 to $199 billion today. It now accounts for nearly half the company’s revenue, and it generates income more predictably than Schwab’s commission-heavy businesses, like its self-directed brokerage, says Steven Chubak, an analyst at Nomura Instinet. The financial sector paid out $124 billion in repurchases in 2017, but Schwab has no plans to join that parade this year.