Don’t look now, but something truly scary is creeping up on you this Halloween: the bond market.

Bond yields have been creeping higher for the last three months, but quickened their pace to a trot and then a gallop in the last week, as the remaining obstacles to another interest rate rise by the Federal Reserve drop away.

The bond market is important because it’s market interest rates, rather than the Fed, that determines whether businesses invest or not, and whether individuals spend their spare cash or save it. That quickly feeds through into broader economic activity and growth. Thus, an angry bond market as Bill Clinton’s former adviser James Carvell famously said, “can scare everyone.”

The release of third-quarter gross domestic product figures earlier Friday, showing year-on-year growth rising to its fastest rate in 9 quarters, arguably removed the last major obstacle to another 0.25 point increase in the Fed Funds rate. Markets now imply a probability of over 75% in a move when the Fed’s Open Markets Committee meets in December.

The yield on the benchmark 10-year Treasury bond hit a six-month high of 1.88% on the news. Although it came back a little later, it’s still 12 basis points higher than it was at the start of the week, one of its worst weeks of the year. (Yields move inversely to prices. A basis point is one-hundredth of a percentage point.)

But the U.S. market isn’t moving in isolation. The main factors behind the move are global.

“The more pessimistic views about the global economy that were expressed in the early part of the year have proved to be unfounded,” said Chris Iggo, chief investment officer for AXA Investment Managers in London, in a note Friday.

He pointed to steady Chinese growth (6.7% year-on-year in the third quarter), which some question the accuracy of. Other indicators, too, are far from apocalyptic. The U.K. economy, which was forecast by some to drag itself and its neighbors into recession after the Brexit vote in June, grew a decent 0.5% in the third quarter. The Eurozone’s GDP probably grew 0.3%, according to research firm Markit’s business surveys. Oil prices bottomed in the first quarter. The Dow Jones Index for Industrial Metals bottomed in January (it’s risen 20% since then and hit a 15-month high Friday), the Bloomberg Softs index for agricultural commodities is up 51% from its low point last year. Sooner or later, such increases in input prices are bound to show in higher consumer prices.

This doesn’t mean that inflation is out of control. At 1.5%, inflation is still clearly below the Fed’s target of 2%. In the Eurozone, the gap is even starker. Germany’s headline inflation rate hit a two-year high of (gasp!) 0.8% on Friday. In Japan, the inflation rate has turned negative again this year and hit a three-year low of -0.5% in September.

But what it does mean is that prices will struggle to fall from their current levels. If inflation is rising, then the European Central Bank will find it easier to dial back its quantitative easing program after its scheduled end in March next year. In the case of the U.K., where currency depreciation is one of the factors driving inflation, and bond yields, higher, the scope for looser monetary policy to help the economy is even narrower.

It’s considerations like this that are making bond investors sweat right now. Low inflation and central bank activism have driven bond yields down to all-time lows across the developed world, lulling participants into a false sense of security. Even though the current sell-off is only a small correction in that context, if inflation continues to rise, everyone knows that all cycles must turn sometime.

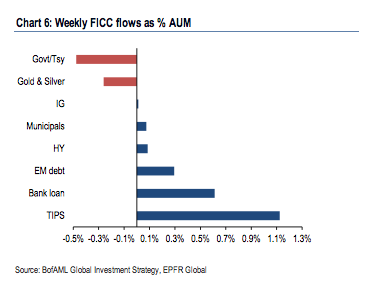

Bank of America Merrill Lynch analysts pointed out Friday that investors are already seeking protection by switching out of fixed-coupon bonds into those that offer embedded protection against inflation. The graphic below show how investors shifted into ‘Treasury Inflation Protected Securities’ at the expense of plain vanilla Treasurys last week.

The investors facing the greatest risks are those who have bought longer-dated bonds in their “hunt for yield,” because the volatility of a bond’s price increases, the longer its duration. This wonderful graphic by The Wall Street Journal shows how ap 1% rise in yields across the board would only drive a five-year bond down 4% in price, but would wipe 27% off the value of the 50-year humdinger issued by France in May this year.

And that’s before you take any other risk factors into account. Falling bond prices would force banks to mark down the value of bonds on their books. That’s a problem in the Eurozone, where debt securities represent 13% of all bank assets. And in the Eurozone in particular, rising debt burdens for governments raise existential questions for the survival of the currency union. It’s no accident that Italy’s 20-year yield has risen 68 basis points since September, while Germany’s has only risen 28. The “redenomation risk”—i.e. the risk that you will be repaid in lira rather than the currency Germany uses—rises sharply in a world of rising interest rates.

Now that’s something to scare anyone.