Venture capital has been one of the investment world’s most severe asset classes, with sharp and short peaks that stand out against the public stock market’s wider waves. And there is new data suggesting that venture capital has already headed into one of its long lull periods, despite the record number of “unicorn” companies that are still waiting to go public or be acquired.

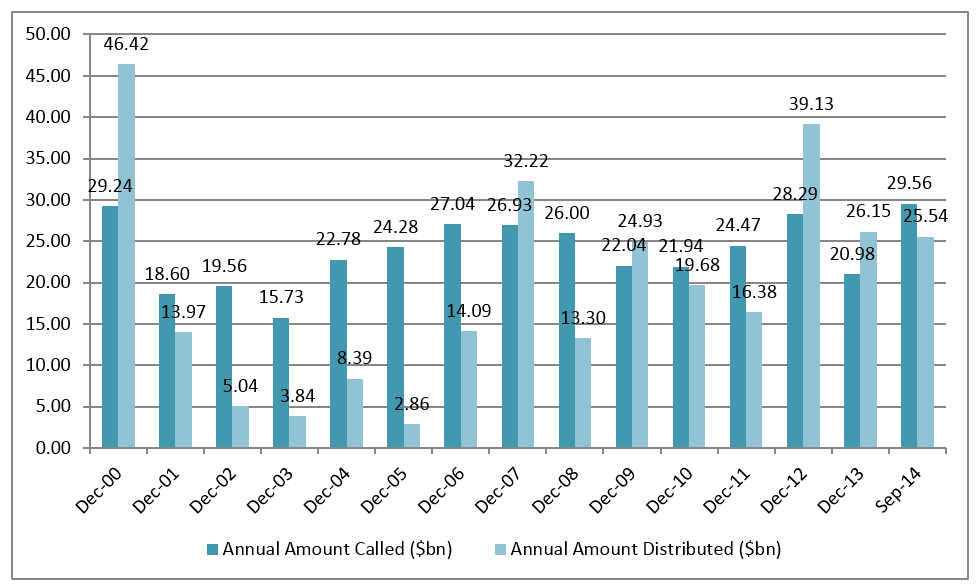

Research firm Preqin reports that global venture capital funds called down more capital than they returned to investors in both 2013 and the first nine months of 2014. In fact, it shows the distributions only outpaced call-downs in one of the prior 12 years (2012), and it’s hard to imagine the trend-line has changed much since the data set ended, given the recent lack of IPOs and acquisitions of VC-backed companies.

Here is the global VC data, courtesy of Preqin:

U.S.-focused funds also have upside down capital flows for the first three quarters of 2014, after two straight years in which distributions outpaced call-downs (the first such winning streak since 1999-2000). The data here is a bit lumpier, but once again we see how large distribution volume in 2014 is being swamped by new investments:

To be sure, not everyone agrees with this data. Cambridge Associates, for example, reports that distributions outweighed contributions in five of the seven quarters ending in Q3 2014 (compared to just four other quarters in which that had happened in the past decade). It also tells Fortune that the positive trend continued in Q4 2014. And Correlation Ventures reports an even brighter history:

Data from @Correlationvc ref the "wet" (not dry) bubble; cc @danprimack pic.twitter.com/B1b71AqilI

— Scott Kupor (@skupor) June 17, 2015

Limited partners I’ve spoken with over the past two days disagree on whether Preqin or Cambridge Associates is right, but even those taking CA’s side say that they believe the distribution delta should be much greater given the perceived quality of typical VC portfolios.

The real unknown in all of this is how the recent spate of late-stage financing rounds — typically not led by VC funds — will reconfigure the historical charts. Will they produce a monster flood of high-value IPOs that obliterate traditional VC cycles, or will their collective weight of invested capital (and/or failures) depress overall returns?

For now, all limited partners can really do is keep writing checks, hope they’re in the right funds and keep their fingers crossed…

Get Term Sheet, our daily newsletter on deals and deal-makers.