2014 has been a record year for global M&A activity in the oil and gas sector, sparked in part by the U.S. fracking boom. But what will happen to deal-making now that crude prices have dropped more than 30% since mid-June, due largely to massive oversupply that soon could cause the price of gasoline to fall below $2.50 per gallon?

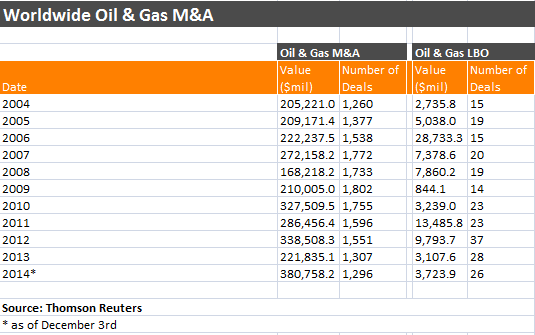

For starters, below is the data on global oil and gas deal activity, courtesy of Thomson Reuters. You’ll note the 2014 dollar volume easily outstrips any past year, while the number of deals is likely to surpass 2013 once the full month of December is included. Also important to point out that this data does not include deals in the power generation or electricity sector, as they are unlikely to be affected by oil or gas prices:

Now let’s take a look at historical crude oil prices:

The first thing that jumps out here is that there seems to be some correlation between oil prices and oil deal activity. Just look at the run-up through 2007, followed by the 2008 drop — and then the subsequent increases from 2009 through this past summer. It’s not a perfect match, but it’s close enough to suggest that the M&A market is not divorced from the oil market’s price cycles.

So what does this mean for future M&A in the oil and gas sector? Four thoughts, based on numerous conversations over the past day with industry deal professionals:

1. Waiting game: Despite the aforementioned correlation, it’s unlikely that we’ll see any immediate chill to new deal announcements. Almost any transaction closing during the remainder of 2014 is likely to have been in the works for several months, if not longer. Yes, securing leverage for new energy deals is pretty difficult right now, but the general rule is to expect at least a one-quarter lag when determining whether macro factors are having an impact on new deal activity. Lags do work both ways, however, which means that a present-day slowdown in new deal formation would likely show up in Q1 and Q2 2015, even if there is an intervening oil price lift.

2. Overall deal activity will decrease: The big impediment to new deals right now is price. Not oil price, but how falling oil prices affect valuations. Many owners, assuming they’re not distressed, will not be satisfied with 20% or 30% haircuts to what they could have gotten for their assets just five months ago. Oil prices will rebound, they’ll believe, and selling at a bottom is foolhardy. Buyers, on the other hand, see valuation from the exact opposite side. Not only should they be paying 20% or 30% less than back in June, but possibly even deeper discounts given that oil prices have been falling steadily for several months. This sort of buyside/sellside disconnect happens almost whenever there is major downward macro pressure — regardless of industry — and it chills new deal activity.

3. We’ll see less investment from big oil: A lot of big exploration and production companies are panicking right now, trying to pinch every penny in order to hit some semblance of quarterly earnings projections. One of the first things to go is new spend. Not only on R&D investments — both internal and external via venture capital — that could help save the companies money in the long-term, but also on M&A that isn’t immediately accretive. Given that much of the big-money M&A activity has been for non-producing assets, it’s hard to see a lot of new activity in that space. It’s possible that there could be some oilfield services consolidation but that gets hampered by the aforementioned valuation disagreements (exacerbated by the fact that some strategic buyers don’t want to “sell” their stock on the cheap to acquired companies).

4. Where we will see increased M&A: There have been countless new E&P companies formed over the past few years focused on fracking, largely following the same model: A team of E&P veterans get private equity backing to acquire undrilled land on a shale formation, and then get to work. In many of these cases, however, only some of the acquired acreage is considered primary. The rest is fringe and, at current prices, is unlikely to get drilled. It’s this land that could soon hit the open market, particularly given that many of the PE-backed platforms also have serious debt to service. It’s the one case where asset owners will swallow hard, and then accept discounted offers.

Sign up for Dan’s daily newsletter on deals & dealmakers: Get Term Sheet