If you need evidence of just how weird the U.S. economy is these days, look no further than the Commerce Department’s revision of its estimate of first-quarter GDP growth issued Tuesday, which showed the economy shrank by 2.9% during that period.

It’s not that economy shrinkage during a given quarter is especially rare. In the past 160 quarters, the U.S. economy shrank 20 times. But in all but 3 of those instances, we were in the middle of a recession. The only other times the economy shrank in a quarter that was in the middle of a period of economic expansion was during the third quarter of 2011 (-1.2% growth) and the second quarter of 1981, when the economy also shrank by 2.9%.

You might think that 1981 would be an encouraging example, as economic growth the following quarter bounced back to 4.7%. But after that, the economy fell into one of the worst recessions in memory.

So, should we expect a bounce back or are we headed for another recession?

Despite the historical evidence, most economists still expect the contraction in the first quarter to be nothing more than a bump in the road and a statistical curiosity. Ethan Harris, co-head of global economics research at Bank of America Merrill Lynch, says the report “makes no sense,” and that he is more or less looking past the data and chalking up most of the contraction to the unseasonably cold winter.

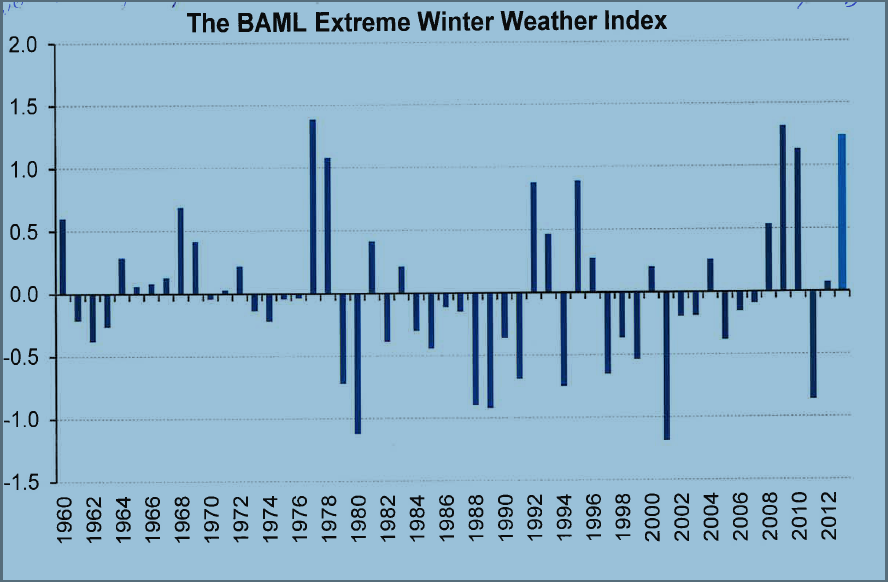

Indeed, there’s reason to believe that the weather had at least some effect on economic growth. Here’s a chart of Bank of America’s proprietary extreme weather index, which combines state-by-state data on weather to estimate how extreme the weather was during a given winter.

Looking at these figures, we can see that last winter was the third most extreme since they began compiling data in 1960.

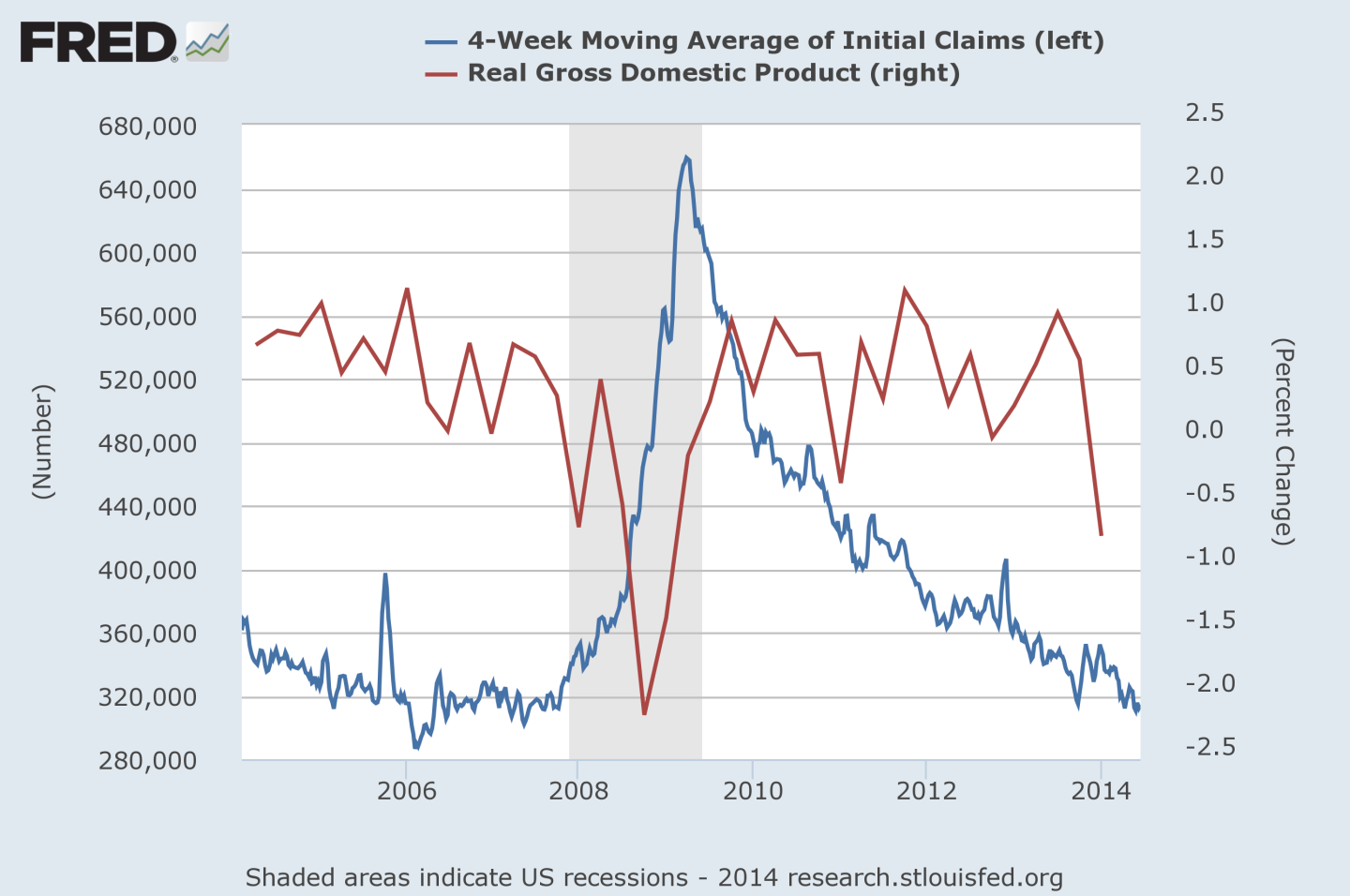

Another reason to discount GDP data is the fact that weekly unemployment claims—the measure of how many new people have filed for unemployment benefits—have been falling. Unemployment claims are what is known as a “leading indicator,” meaning that they tend to go up before we see GDP fall, and they tend to fall before we see increases in economic growth. Below is a chart showing the four-week moving average in unemployment claims and quarterly growth in GDP.

During the 2008 recession, unemployment claims began to rise well before we saw large, recessionary contractions in the economy. Right now, we’re seeing a steady decline in the number of people filing for unemployment insurance.

In other words, history is sending us two conflicting messages about today’s economy. One is that you tend not to have the sort of contraction we had in the first quarter of this year without a recession on the horizon; the other is that we don’t usually see the sort of declines in unemployment claims we’re seeing now without subsequent strong economic growth.

Either way, the first quarter of 2014 is going to go down as one of the strangest in economic history.