Fourteen years ago I was a cub reporter who had just been assigned to the private equity beat. Over lunch at a TGI Friday’s, my new editor explained the industry’s basic structure: Private equity firms raise funds from large institutional investors (i.e., limited partners) and then slowly use those funds to buy companies. The limited partners pay the firm a percentage of their committed capital each year as a so-called management fee to cover overhead expenses like salaries and office space. The partners also share a percentage of any eventual investment returns with the firm, so as to better align interests.

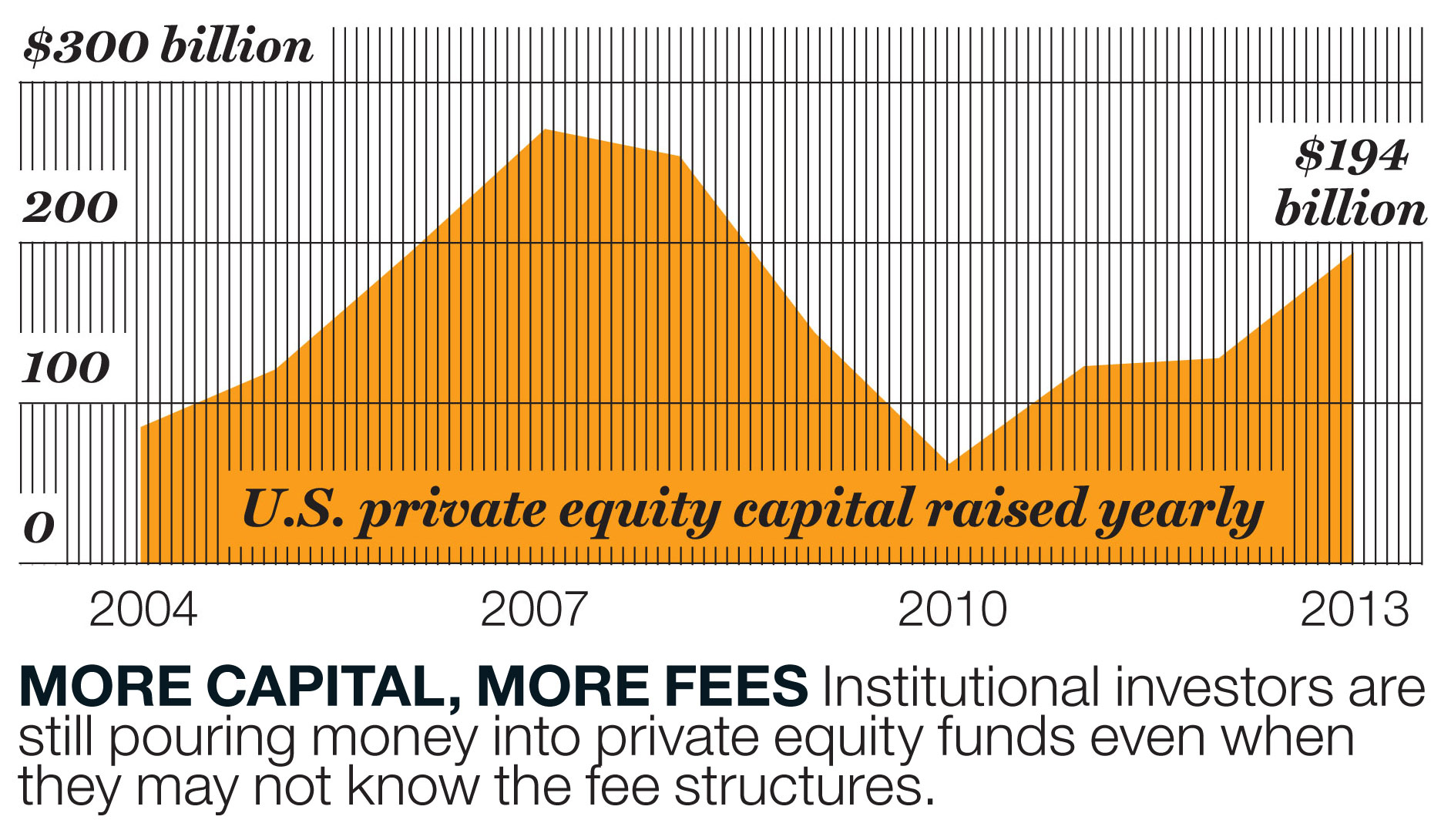

That all remains accurate today, even as the private equity industry has multiplied in terms of size and public profile. But it also glosses over a lot of the fine print, particularly in terms of additional fees and expenses that private equity firms often charge both their investors and their portfolio companies. It is that fine print that the Securities and Exchange Commission is now investigating, thanks to tools made available via the Dodd-Frank financial reform of 2010. So far the results are troubling.

“When we have examined how fees and expenses are handled by advisers to private equity funds, we have identified what we believe are violations of law or material weaknesses in controls over 50% of the time,” said Andrew Bowden, the SEC’s director of compliance inspections and examinations, during a recent speech. In a follow-up interview with the New York Times, he added, “In some instances, investors’ pockets are being picked.”

To be sure, this isn’t all about rapacious Wall Street vs. meek Main Street. Limited partners–even public pension systems–are supposed to be sophisticated investors with their own well-paid lawyers and accountants. The real problem, from my perspective, is that both sides have gotten too clever for their own good. Private equity firms long ago picked a lot of the low-hanging industrial fruit, so it is more difficult today to generate investment returns than it was a decade ago. They try to make up the difference any way they can, often writing ambiguous investor contracts that are as notable for what they don’t enumerate as for what they do. For example, if a contract says that the limited partner is entitled to 80% of nine specific types of fees charged to portfolio companies, what happens if the firm later conjures up a 10th type of fee?

On the flip side, limited partners also want to feel that they’ve gotten the best deal possible. That’s why many of them–particularly the large ones with clout–now insist on individualized “side letters” that include pet terms or clauses. No wonder Blackstone Group president Tony James recently said, “Legal and compliance is our fastest-growing part of the firm by far.”

What’s been largely lost in all this is the spirit of partnership that is supposed to underwrite the investor/firm relationship. Both sides still pay it plenty of lip service, of course, and may even have convinced themselves that it remains foundational. But it’s extremely difficult to have a true alignment of interests after negotiating such adversarial agreements. Even if investors aren’t technically being cheated, someone isn’t getting exactly what he thought he’d signed up for. And the SEC’s comments have caused even the most loyal limited partners to privately concede that they may have been bamboozled.

As with so many things, the best solution is simplicity. Private equity fund contracts needn’t be proprietary 150-page tomes whose size seems designed to mask what they didn’t include. Their language can be streamlined and standardized while still permitting differences in terms of specific percentages and fee adoptions. Side letters can be scrapped, outside of ones whose main purpose is to satisfy jurisdictional requirements.

In short, private equity should rebuild itself by using what I learned at TGI Friday’s as a goal to work toward, rather than as a starting point from which to deviate. If not, the SEC may move beyond just asking questions.

This story is from the June 30, 2014 issue of Fortune.