Can Procter & Gamble Find Its Aim Again?

It’s been a humbling decade for the consumer products giant. Now leaner and more focused, with its third CEO in three years, can the king of brands regain its relevance after years of subpar returns?

On the ninth and 10th floors of Procter & Gamble’s (PG) Cincinnati headquarters, in a secure area that few are permitted to enter, sits the company’s Retail Innovation Center. The “I,” as it’s known, is slick and highly digital. P&G’s top executives believe it contains the ingredients of the company’s coming turnaround.

The center, which existed at another location for years but was revamped and moved in 2015, aims to tell P&G’s story to its major customers. There are video case studies of disrupters, from Uber to Airbnb. There are mocked-up shelves of both P&G’s and competitors’ products and rooms set up to show P&G items in their intended habitats (such as a baby’s room with a diaper table in a suburban home and a laundry setup in an apartment). One room is being prepared for a feminine-care presentation, with lingerie, pads, and tampons demonstrating various levels of absorbency. This is serious business.

An enormous screen in the first room allows users to click on stories showing how new technologies and marketing strategies are used. It’s mesmerizing. But there’s something odd: None of the hundreds of examples are P&G’s own innovations. That’s by design, say its creators, who want visiting customers from the likes of Walmart (WMT) and Target (TGT) to be startled by the pace of change, and then move on to learn more about what P&G is doing to change the consumer business. It uses big data to create customized analytics for every customer. The goal: convince people that P&G is modern, fresh, and ready to compete in this new and uncertain world.

But the sheer number of disruptive ideas depicted from outfits other than P&G underscores the fact that the $78.8-billion-in-sales company has had so few of them of late. It’s unexpected, considering the unparalleled innovation history of P&G. Scroll through the timeline on its website, and you’ll be struck by just how many world-changing technologies (first toothpaste with fluoride! first synthetic detergent!) were hatched there.

The array of global brands is unmatched. There are Ivory Soap (1879), Crisco (1912), Tide (1946), Crest (1955), Pampers (1961), Bounce (1972), Dawn (1973), Always (1983), Febreze (1998), and Swiffer (also 1998), as well as plenty of brands acquired by P&G (Gillette, Pantene, and others). The company claims it was the first to truly use market research (1920s). And if that’s not enough for you, P&G is responsible for conceiving the soap opera too (1933).

See Procter & Gamble’s Fortune 500 company profile here.

The past is indisputably glorious. As for the present … um, did we mention the past? The company renowned for its stable of 21 billion-dollar brands hasn’t invented a new 10-figure brand from scratch in a decade. Yes, P&G crossed the billion-dollar threshold with Tide Pods in 2012, but that was a new delivery system more than a new product.

The drought will end, insists David Taylor, P&G’s CEO since November. The company is reorganizing its R&D function and moving power to the leaders of product categories rather than leaving it to senior executives far from the marketplace. It is again focusing on breakthrough technologies that can change people’s lives, says chief technology officer Kathy Fish, or at the very least, in her words, “wow the customer” with memorable experiences. “We were doing a lot that wasn’t adding value for the consumer,” she says, “and even worse, that was making it hard for the consumer to shop our shelves.”

There are, Taylor contends, promising signs: new products like Tide purclean, a “greener” laundry detergent; Downy Unstopables (sic), which are scented beads for the washer; and Febreze Car freshener. Sure, they’re brand extensions, but they all use new technologies—and the latter two have sold some $300 million each in their first year. Those are notable achievements, even at a behemoth like P&G.

Taylor, who is quick to say the transition will take time, says he wants P&G to regain its “mastery” after years of management turmoil, poor strategic decisions, and a series of unhelpful macroeconomic trends, including a rising dollar, which hurts P&G more than many others.

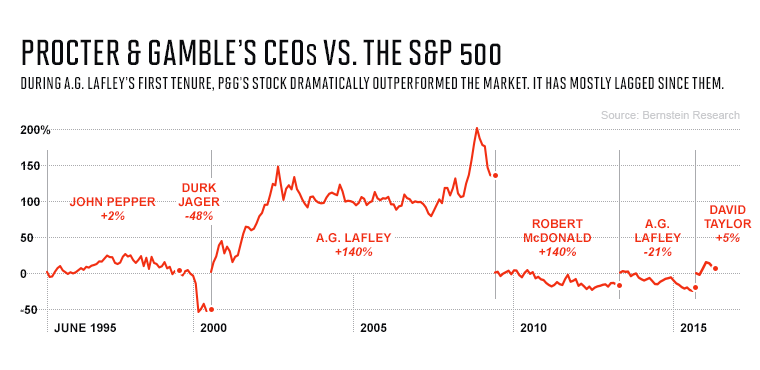

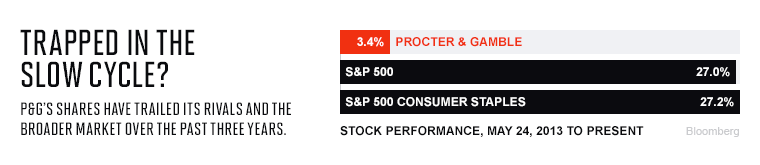

It is no easy task. P&G sales peaked at $83.7 billion in 2012 before stagnating and then declining as the company began offloading brands. For 14 of the past 17 quarters, P&G has been losing market share in half or more of its products. Its revenues have lagged analysts’ expectations for four of the past five quarters. The company’s stock has barely moved, inching up a cumulative 6.5% over the past two years, vs. 23% for rival Colgate and 29% for the S&P 500.

Talent has streamed out. Even the return of P&G’s prodigal son, A.G. Lafley, as CEO, didn’t fix that. Lafley had to come back in 2013 after his handpicked successor, Robert McDonald, left amid intense criticism. The squabbling that led to his ouster has subsided, but so, too, has optimism that the company has finally turned the corner. Taylor, 58, a 36-year P&G vet who hasn’t granted a formal interview until now, acknowledges this. “Until we put up numbers,” he says, “I don’t expect anyone to believe anything.”

Once a global giant stumbles, it’s hard to recover. Just look at HP (HPE), which lost its way and continues to deconstruct itself, or Kodak, Yahoo (YHOO), Sony (SNE), or Sears (SHLD). P&G certainly faces no mortal threat; it made $7 billion in profits last year, and it’s still a pivotal consumer goods company. But it’s struggling to regain its dominance, its fire, the magic that long attracted the brightest marketing, branding, and scientific minds.

Taylor is honest about P&G’s challenges and has the trust and support of his team. “There’s not a single person on the leadership team that says we need to maintain the status quo,” he says. But it is an immense task. Can a lifer—or anyone, for that matter—rekindle that P&G spark?

CEO succession is a complex, often messy endeavor. Just ask the board at Disney, (DIS) which has struggled to identify a future replacement for CEO Bob Iger, or those duking it out with 93-year-old Sumner Redstone for control of Viacom (read more about that in our feature “Here’s What’s Really Going on Inside the Fractious Battle for Viacom“). That was not the case at P&G back in 2009, when Lafley, who had presided over a decade of dramatic innovation and renewal, as well as the company-doubling $57 billion acquisition of Gillette in 2005, prepared to step down.

Talent management and succession planning was something that P&G, the ultimate promote-from-within company, considered among its greatest competitive advantages. One of its biggest trade secrets wasn’t a clothes-cleaning technology or diaper formulation, but its Talent Portfolio, a blue binder that listed pertinent data on every candidate for the top 120 jobs—as well as their potential replacements several levels down. In 2009 I got a peek inside that binder as I reported extensively on the carefully calibrated process that elevated then-COO McDonald to succeed Lafley.

But as impressive as the method was, the result was a bust. In fairness, McDonald had the misfortune of taking over during the punishing global recession that followed the financial crisis. But he proved to be a divisive leader. And he set out so many goals that few could grasp the real priorities. He also lacked a strong chairman, a P&G hallmark. Lafley served as chairman for just six months before resigning and leaving McDonald to his own devices.

Too many of the decisions during Lafley’s first tour as CEO—heralded at the time—turned out to have complicated aftereffects. The company’s emphasis on premium products in North America, such as Olay’s higher-end skin creams, left it exposed when purchasing power dropped during the financial crisis. Lafley’s decision to consolidate more power in “global business units” left long-powerful brand and country managers struggling to apply local insights.

“Innovation” came to mean modest twists on existing items (think Pantene for curly hair, medium-thick hair, Heat Shield, and Ice Shine) rather than new ideas. Says Werner Geissler, P&G’s former vice chairman: “R&D people were working too much on cosmetic upgrades as opposed to game-resetting innovations. Head & Shoulders with Apple? Seaweed?” (In case you’re wondering, P&G did sell both versions.)

And the seemingly logical move into developing markets—where the rising middle class meant billions in new consumer spending—proved more volatile than anticipated. It was this move that defined McDonald’s tenure: In 2011 he announced that P&G would have 800 million new customers by 2015, primarily in China, Russia, and other newer markets. “The move of the center of gravity is critical,” he said at the time.

It never happened. Instead, P&G posted a string of sales and earnings disappointments. The result: a falling stock and unhappy pensioners (whose retirement was paid in stock) who actively campaigned for McDonald’s removal. That occurred as activist investor Bill Ackman took a stake and publicly denounced McDonald’s leadership. A slow-moving political bureaucracy, it seemed, had lost its way.

On May 23, 2013, McDonald suddenly “retired” from P&G. Back came Lafley, then nearly 66. Having remarried and moved to Florida to pursue triathlons and a part-time private equity gig, he found himself again at the company he had left so triumphantly. P&G’s board believed he was the only person who could dig the company out of its hole. Apparently, P&G’s blue binder didn’t have as much top talent as its heft had implied.

But A.G. 2.0 turned out to be more of a brand extension than a breakthrough innovation. This version of the CEO was older and less energetic, one who defined his job more narrowly than he had the first time around. Once an indefatigable traveler who evangelized about the customer’s “first and second moments of truth,” Lafley stayed behind the scenes this time, using his newfound private equity skills to figure out which brands and categories deserved focus and which should be jettisoned. He announced he would no longer speak on quarterly earnings calls, refused to interact with the press, and, despite the fact that China was one of the company’s biggest trouble spots, visited there only twice in his 2½ years at the helm. He wasn’t even willing to move back to Cincinnati. That meant a P&G jet flew him back to Florida every weekend, at a cost of $512,000 in 2015 alone.

Once driven by passion, Lafley now seemed motivated by obligation—as well as, perhaps, a desire to preserve his legacy. As he told an audience at UCLA’s Anderson School of Management in December when asked why he came back: “The short answer was duty and unfinished business.”

Lafley set about, in some cases, undoing actions he himself had taken years before. In 2014, P&G announced it would sell what turned out to be 116 of its 166 brands—a housecleaning that included several acquisitions championed by Lafley himself, such as Wella, bought for $7 billion in 2003, and Clairol, for $5 billion in 2001. In 2015, Coty agreed to buy the two, along with 40-odd others, for $12.5 billion. Duracell, which came with the Gillette purchase in 2005, was sold to Warren Buffett this year. (The Oracle of Omaha traded his 52 million P&G shares for the battery business, a seeming vote of no confidence in P&G’s overall prospects.)

Lafley, and later Taylor, began recalibrating the company’s strategy in China. P&G had entered early, in 1988. But it underestimated the growth of China’s upper class, focusing instead on the lower- to middle-class market. Its diapers, for example, proved vulnerable to higher-end offerings from Japanese competitors; P&G’s market share has fallen nearly five percentage points since 2010, to 37%, according to Euromonitor & Citi Research. Explained Taylor at a recent conference: “We looked at it too much like a developing market as opposed to the most discerning customers in the world.” P&G is now trying to move upmarket in China.

P&G has also shifted more resources back to North America, where it has a more dominant share. And it has become leaner and less bureaucratic, in part through huge job cuts—35,000 by the end of 2016. P&G has slashed product categories from 15 to 10 to improve focus. Says Jon Moeller, its longtime CFO: “The businesses we are keeping are those where we have a product technology that makes a consumer difference—and, almost to a one, daily use items.”

When asked about reversing his own much-lauded strategy, Lafley was unapologetic: Different times require different measures. As he told the audience at the Anderson School (Lafley declined to be interviewed for this article): “I had two incredibly interesting opportunities, and they were 180 degrees different. In 2000 the job was to grow. It was an extension and expansion strategy. When I came back,” he said, “I looked at a company that was overextended and overexpanded … It was a totally different situation.” Left unsaid was the question of whether one strategy might have had anything to do with the other.

After just over two years, Lafley concluded he was done, again. He hadn’t revived top-line growth, but he had made tough decisions and, he felt, refocused the company. Lafley announced he would move to executive chairman in November 2015—to be replaced as CEO by Taylor, then the group president for global beauty, grooming, and health care. The board conducted a search but ended up choosing—again—a lifer carefully groomed by Lafley. (In another Groundhog Day moment, Lafley announced on June 1 that he will resign as chairman again on July 1. This time he stayed eight months rather than six.)

Internally, there was a collective sigh of relief. Taylor, many thought, could provide both stability and a higher level of engagement than the company had experienced of late. Taylor is known as a good guy—the type who trusts his lieutenants, inspires people, and bleeds P&G blue and white.

He began as a plant engineer. But 12 years in, he decided he wanted to work with the brands and started over again from the bottom as an assistant brand manager for Pampers—an unusual move and one that required humility. Says Gary Martin, P&G’s former head of family care, who ran product supply when Taylor was a plant manager: “He was always a star. I managed 65,000 people, and every time we rated the most promising people, he was always No. 1.”

Taylor is white, North Carolinian, basketball-loving, churchgoing—straight out of central casting for the P&G executive suite, if not exactly an improvement on the diversity front. He has worked in beauty, grooming, and fabric care on multiple continents, but spent most of his time in the baby-care business. An operations guy rather than a marketer, Taylor won kudos for successfully expanding the paper business into Europe and, later, advocating the sale of the pet-care business.

Unlike some predecessors, Taylor is said to make people feel comfortable. But is feeling comfortable what P&G needs right now? “I find [Taylor] to be absolutely lovely,” says veteran Citigroup (C) analyst Wendy Nicholson. “But when you talk to him he talks a lot about the high level: ‘We care about the consumer and culture.’ You wonder if that makes folks feel better, but maybe it’s not the right approach.”

Taylor says he understands such criticism, but responds, “I’m in a great position because I understand that culture.” There have, of course, been secret rebels who entered as seemingly rote company men only to smash the china. Intel’s (INTC) Andy Grove was the clear exemplar, and GM’s (GM) Mary Barra and Microsoft’s (MSFT) Satya Nardella are attempting similar transformations. But so far, it’s hard to imagine that this earnest red-haired guy with 36 years at the company is a secret revolutionary in a plaid jacket.

One thing that’s clear is that Taylor is obsessively committed to Procter & Gamble. He does not sit on any other boards (he resigned from TRW’s in 2015), does not speak to graduation classes, doesn’t give interviews (this was his first sit-down with a reporter, and he agreed to it only after it became clear that the article would be published whether he cooperated or not), and doesn’t go to Davos. He devotes himself to one company. “You can’t imagine how many people want to see you,” he says when asked what’s different about being the chief executive. “But unless they say it’s important to Procter & Gamble, it’s not important to me.”

Taylor knows that changing the culture requires injecting a new sense of urgency. To show he’s serious, he holds frequent webcasts and town halls and has visited 20 different countries in the past 12 months, including China three times. He doesn’t proselytize for a new vision. Instead, he says, he offers “straight talk” about what’s happening and encourages underlings to use the same approach with him. He has said that nothing is off the table when it comes to fixing P&G. (Taylor wouldn’t comment on suggestions that P&G be split up or the rumored acquisition of Church & Dwight, whose brands include Trojan, Arm & Hammer, and Nair; that would be a surprise after so much divestiture.)

His initiatives so far have all been sensible—but they are not exactly barn burners. Many involve shedding layers of bureaucracy and empowering people who are closer to their market rather than to headquarters. Taylor is also changing the compensation system to take into account employees’ local unit and country performance as well as global results.

The CEO hates PowerPoint presentations. He uses a simple scorecard: Each product is marked green (good progress), yellow (some issues), or red (trouble) compared with its competitors, accompanied by a plan to fix the problems or expand. “I don’t want to see fabric care say it’s winning against other [P&G] categories,” he says. “I want to see what we did against the best competitor.”

On the innovation front, CTO Fish, who has been in place since 2014, is reorganizing R&D. Initiatives that cannibalize brands without expanding the overall market are being deemphasized. She points to offerings like the new Oral-B Bluetooth toothbrush, which records your time brushed and the parts you’ve missed, or SK-II’s Magic Ring, which measures your skin’s age, as examples of the return to P&G’s technical superiority.

But some outsiders are concerned that may not be as relevant in an era when millennials are enthralled more by value than by top-of-the-line science, by sustainability as much as performance. Case in point: Dollar Shave Club, which since its 2011 founding has sliced out 8% of the razor market with a cheap but reliable online offering that took P&G by surprise. Says Ali Dibadj, an analyst at Sanford Bernstein: P&G is “creating the best technical product, but the consumer wants something emotionally bonding, niche, and customized. The Honest Co. has a message. Do people argue that it works better than Tide? No. Do people find it attractive to be attached to that brand? That’s what these guys don’t get.”

In response to Dollar Shave Club, P&G’s Gillette unit launched its own online offering in 2015—and sued the company for allegedly stealing its intellectual property. (A Dollar Shave spokesperson denies any patent infringement and adds, “We are not intimidated by Gillette’s attempts to thwart competition with litigation.”)

Where P&G is making undeniable progress is in cutting costs—which began under McDonald but continues to accelerate. Amazingly, the company was working with 6,000 creative agencies until 2014: By reducing the number by nearly 40%, it has cut its marketing and production spending by $500 million, with more to come.

Now the company has another $10 billion cost-reduction plan underway. Much of it will come from an overhaul of the supply chain in North America and Europe. Global product supply officer Yannis Skoufalos says he is reworking the system as if he is building it from scratch—a monumental task for a company of P&G’s size.

Parsimony helps, but nobody, as the old line goes, ever cut their way to greatness. “I don’t believe his focus on cutting costs was sufficient,” says Melanie Healey, who headed P&G’s North America business until 2015. She’s speaking about Lafley, but the point applies to Taylor too. “It needed to be more balanced, early on, with also investing in growing the top line. Both are critical to driving shareholder value.”

Needless to say, constant budget pruning doesn’t do a whole lot for morale; either you are cut, or you work more. That may be why people continue to leave P&G. Says one former top executive who is in touch with many P&G execs: “They’re very frightened. They’ve lost their swagger, their confidence.”

Perhaps P&G needed to lose some swagger. The sense of infallibility that comes with success can be precisely what allows disrupters to sneak in. And the company—most of all Taylor—understands this is what happened. But will that knowledge make a difference? Says a former top P&G executive: “P&G knows how to solve these problems. It has more consumer data than anyone on the planet. It has the tools. It has the ideas. But culture gets in the way of allowing those ideas to move forward quickly.”

A version of this article appears in the June 15, 2016 issue of Fortune.