Untangling Dividend Stocks

Finding strong income in equities is getting trickier. Here are the top ideas from five of the best fund managers in the business.

Up until a few months ago, dividend investing seemed a bit like a child’s first soccer game: Every player was a star, the spectators were happy and supportive, and the whole team got a participation sticker.

But as every parent knows, the mood starts to change after that forgiving period. The competition gets stiffer, the observers a lot more critical, and the system rewards only those rare talents who can deliver in important moments.

These days it’s feeling more like the Olympics if you’re an investor seeking income. That’s because the contest to find winning dividend payers is intense, raising the degree of difficulty to its highest level in recent memory. Stock valuations in the category are lofty after years of outperforming the broader market. The forward price/earnings ratio of the top 25% of S&P 500 stocks by dividend yield is 17, vs. a 36-year average of 12, according to Ned Davis Research. Indeed, stocks of all varieties are suffering a case of altitude sickness these days: P/E ratios are in the 97th percentile relative to levels over multiple decades.

Meanwhile, actual dividends, as piddling as they have been since the 1990s, aren’t likely to soar. The average payout ratio—the percentage of profits that companies hand to shareholders as dividends—has risen to 40%, well above where it has been over the past 10 years (except for during the financial crisis and recession, when earnings plummeted, making the ratio spike upward). Dividend increases are shrinking, and the number of decreases is accelerating.

Then there’s the monster that rarely seems to leave the closet: potential interest rate hikes. Of course, historically low rates made dividend stocks attractive in the first place, as retirees abandoned Treasury bonds in favor of dividend-paying stocks. (Even today, the yield on a 10-year Treasury, 2.3%, is only a few ticks above the 2.0% average yield of an S&P 500 stock.)

If rates rise, as is expected, investors could flee the sector and send stocks careening downward. “It is a difficult time for fund managers,” says Howard Silverblatt, senior index analyst for S&P Dow Jones Indices. “No doubt they are all looking with nervousness at interest rates.”

Okay, there are plenty of ominous clouds on the horizon. But there’s also a lot of evidence for a sunnier scenario. For starters, dividend payers actually outperform nonpayers even when interest rates are rising, Ned Davis Research points out.

And that P/E ratio of 17 for top dividend stocks, though elevated, is only slightly higher than the overall S&P’s 16.7. If you’re going to tolerate a lofty price, you might as well get a healthy dividend with it. As Warren Buffett is fond of pointing out, equities tend to outperform bonds over long periods.

Still, between the threat of rate hikes and the potential dislocations stemming not only from an epochal transition between presidential administrations, but also from Brexit and economic and political change around the world, uncertainty abounds.

It’s a particularly appropriate moment to seek the wisdom and experience of a sage expert, one who can look beyond just yield levels and make sense of the numbers. A dividend whisperer, if you will. We asked five of the best in the business to assess what’s happening in the dividend world and where they see opportunity and safety.

The Contrarian

Ramona Persaud

Fidelity Dividend Growth and Fidelity Global Equity Income

In the world of income-oriented stock investing, there is one horrifying event akin to a skunk wandering into a garden party: the dividend cut. When cash-strapped companies slash their payouts, most income-loving investors react with horror.

Then there is Ramona Persaud. The manager of Fidelity’s Global Equity Income Fund, whose three-year returns of 5% have almost doubled its world-stock benchmark, might actually perk up at a dividend cut. The reason? A cut most likely means a company’s share price is swooning. It might be an occasion to pick up a quality name on the cheap. “At the point when everyone feels like they want to throw up, that is exactly the point when I might be willing to look at a company,” says Persaud. “A cut clears the decks, takes the pressure off the balance sheet, and takes the pay- out ratio to sustainable levels.”

The contrarian-minded manager also has a soft spot for stocks she thinks have been excessively punished. One example: clothing retailers, many of which have been battered owing to the fear they will be crushed by the Amazon.com (AMZN) juggernaut.

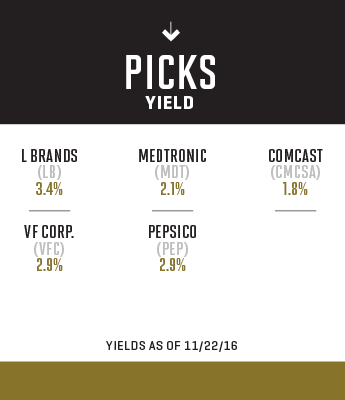

That is why Persaud picked up shares of L Brands (LB), which owns the likes of Victoria’s Secret and Bath & Body Works. She likes the company’s “shrewd” instincts and its knack for delivering a return on capital “far superior to the market,” an average of about 27% over the past five years. Despite that, L Brands shares trade at a valuation roughly equal to the overall market’s. To Persaud that “just didn’t make any sense.” The stock’s yield is 3.4%, and the payout has been growing at a 25% annual clip since 2011. Throw in management’s track record of reducing share count, and L Brands shares look alluring indeed.

Persaud is also a fan of VF Corp. (VFC), the $23-billion-in-sales parent company of brands ranging from the North Face to Timberland to Lee jeans. The retailer’s stock has slipped 10% so far this year, lowering its forward P/E to 16.4. Now could be a handy moment to buy VF shares and profit from their 2.9% yield.

She also sees intriguing potential abroad, where many markets boast average yields higher than the S&P 500. For instance, the prevalence of public pensions in the U.K., which require ongoing cash streams to service their obligations, has led to a market culture that values higher yields. (Among her global fund’s top holdings: Ireland-based Medtronic, which is yielding 2.1%.)

The Seeker of Growth

Tom Huber

T.Rowe Price Dividend Growth

T. Rowe Price’s Tom Huber is feeling cautious these days. With valuations lofty, profits being squeezed, and payout ratios having risen for years, the gems are rarer and harder to uncover. But Huber has a track record of locating them, with five-year average annual returns of 13.2%. He focuses nearly as much on potential growth—either in the dividend itself or in the stock price—as he does on the dividend.

One Huber favorite, which will be familiar to fans of the Dividend Aristocrats (those companies that have raised their payouts for 25 straight years or more) is PepsiCo (PEP). A strong mix of beverages and snacks means plenty of free cash flow and 10% annual dividend bumps for the past 10 years, making for a 2.9% current yield. Huber foresees high-single-digit earnings-per-share growth, and 15% share-price upside in the next couple of years, even before factoring in yield.

In some cases Huber is willing to accept a below-market yield because he anticipates above- market growth. Exhibit A for such an approach: Comcast (CMCSA). The cable giant pays a modest 1.8%. But with its best-in-class balance sheet, savvy management under CEO Brian Roberts, and “underappreciated” performance—including improving the profits of its NBC unit—Huber loves its steady, subscription-based cash flow. More- over, Comcast has been increasing its dividend at a healthy 20% clip for the past five years and has room to bolster it further. Combine that with stock buybacks and share-price increases, and Huber foresees double-digit annual returns.

The Steady Hand

Don Kilbride

Vanguard Dividend Growth

For all the interest rate Cassandras out there, Don Kilbride of Wellington Management, who oversees Vanguard’s Dividend Growth Fund, has a word of advice: “Relax.”

For one thing, a rate hike is a signifier of a strong economy, which suggests that most stocks should be doing well. Second, any elevation in rates is likely to be extremely gradual and not shocking to the market.

Lastly, Kilbride’s eyes aren’t on this quarter’s share-price shifts, or next quarter’s. He’s looking five or 10 years away, so the minutes of the Fed’s next meeting interest him very little indeed. “We think the best way to make money is over a long period of time,” he says. “Compounding is a very powerful metric, and the way you take advantage is to let time be your friend. We like low turnover and eliminate expenses by buying high-quality stocks and holding them for many years.”

Kilbride’s approach has led his fund to 7.9% average annual returns over the past decade, vs. 6.8% for the S&P 500. He avoids so-called dividend traps by steering clear of stocks with suspiciously high yields, which may indicate problems ahead, he says. As a result he is underweight in classic equity-income sectors like utilities and telecom, while overweight in health care.

Nike (NKE) is an excellent representative of the two factors Kilbride looks for: companies that are creating value and making a habit of distributing that value to shareholders. Fat margins and plenty of free cash flow are both “top of class,” and earnings per share have been growing at a double-digit rate for years. That operating wizardry has allowed the sports- apparel Goliath to push its dividend up steadily, at 18% a year over the past decade, an “astonishingly good number,” says Kilbride. (Current yield: 1.3%.) And yet the payout ratio remains a modest 22%, which indicates Nike can easily afford more share- holder raises in the future. Since the stock has dropped from $67 to $50 in the past year, it could be an attractive time to pick up an established dividend grower at a modest discount.

Another favorite: retailer Costco (COST). The big-box chain has a yield in line with its frugal prices—a bargain-basement 1.2%—but that dividend has been rising 24% a year over the past 10 years. The company’s “terrific” management (for more, see our feature on Costco in this issue) and history of earnings growth has Kilbride swooning: “I could talk forever about Costco.”

The Purist

Michael Reckmeyer

Hartford Equity Income

If you crave a bracing dose of pessimism about the markets, talk to Michael Reckmeyer. A portfolio manager of Hartford Equity Income, he sees not just a single head-wind, but a swirling maelstrom that investors will have to withstand. “It’s a challenging

time right now,” says Reckmeyer, whose fund boasts five-year average annual returns of 14.8%. “There is political and economic uncertainty. There are questions about what the central banks are doing, about Brexit, about the sustainability of China. And we are seven years into a bullish economic cycle, which is very long by historical standards.”

Here’s the good news: In difficult times dividend-oriented strategies tend to outperform the broader market, as investors flee to relative safety. In downturns such as 2000–02 and 2008, for instance, that strategy outperformed stocks as a whole by large margins. (By the same token, the approach can lag during a rollicking bull market.)

So what sets Reckmeyer apart from other man- agers? Some dividend seekers opt for the so-called barbell approach, with some of their holdings offering weighty payouts and others hardly any. Not for Reckmeyer. If a company doesn’t offer a meaningful dividend, he’s not interested. More- over, he likes to “stress-test” holdings to make sure dividends are sustainable in the event of an inevitable market downturn.

One of his favorites: Microsoft (MSFT). Reckmeyer keeps his eyes peeled for management changes, which can be “catalysts for change,” and CEO Satya Nadella certainly fits the bill. The company’s enterprise business, which accounts for the vast majority of its revenues and profits, has locked in gushers of ongoing revenue. It’s a sticky business—big companies don’t change their tech setups easily—and Microsoft’s cloud and database businesses are driving growth, helping mitigate the secular decline of desktop software.

To be sure, Microsoft’s price/earnings ratio has surged, to 18.3, after a nice run. But even at that level the shares offer a substantial yield (2.6%), and the dividend has been raised for 12 years running. A cash hoard of $60 billion and annuity-like revenue streams from subscription businesses portend a safe dividend that should continue to mount.

Another name on Reckmeyer’s “nice” list: Union Pacific (UNP), the largest railroad operator in the U.S. He likes to pounce on market “misunderstanding and overreactions,” he says. So when the carrier’s 2015 volumes fell because of external forces, such as collapsing oil prices, Reckmeyer saw an opportunity.

Rebounding oil prices, lower coal and grain inventories, and a cost-cutting regimen have all begun working in Union Pacific’s favor since then, with the stock having risen 17.5% in the past year. Despite that comeback, its valuation isn’t yet out of reach, with a forward P/E of 17.8. Perhaps best of all: The nature of the business means the firm essentially has a number of regional monopolies around the country, and hence the pricing power to generate some impressive margins. Its yield: 2.3%.

The Hot Hand

Phil Davidson

American Century Equity Income

If you’re searching for dividend investors on a sizzling streak, look no further than American Century’s Phil Davidson. The company’s chief investment officer and manager of its Equity Income offering is riding one-year returns of 12.6%, roughly double that of its

Russell 3000 benchmark. The fund has averaged 10.6% annual returns over its almost 20 years.

So what is Davidson’s playbook? For one, not trying to, as the axiom goes, catch any falling knives. He prefers a conservative philosophy of picking up high-quality, low-debt names that aren’t facing existential problems, like a vanishing market or disruptive competitors.

Look at the fund’s top holdings: big, cozy names like Johnson & Johnson (JNJ), General Mills (GIS), Exxon Mobil (XOM), and Walmart (WMT). A common trait: dominant positions that offer investors steady and sustain- able dividend streams, providing what he calls “a layer of protection.”

A preference for big names doesn’t mean Davidson is afraid of volatility, though. In fact he’s okay with a gyrating stock price as long as it’s caused by cyclical or temporary external forces rather than structural internal problems.

It’s getting tougher to buy companies on terms we like.”

—Phil Davidson, American Century

One stock he favors is oil and gas services giant Schlumberger. It has a dominant market share and stable underlying businesses, but its relationship to volatile oil prices buffets the stock quite a bit. What Davidson likes: Schlumberger shrewdly uses the periodic downturns to improve its competitive position, buying companies on the cheap and gaining market share against weaker players that have to retrench. Combine that with a sparkling balance sheet and its history of never cutting its dividend—the yield is now 2.5%—and its beaten-down share price (down by a third over the past two years as oil prices collapsed and the company’s profits were pounded) looks like an opportunity to pick up a high-quality bargain.

Another name to watch is Air Products & Chemicals (APD), an industrial gas company. As you might expect, it’s a realm with a high barrier to entry; just a handful of operators control almost all the market. But in the past the company owned some unwieldy noncore businesses and was dragged down by margins that lagged those of its industry peers. The proof of a righted ship: AP&C has raised its Ebitda margins by seven percentage points over the past three years, dramatically closing the gap with Praxair (PX), its primary competitor.

Recent asset sales have helped the firm focus on high-quality core assets, fire up its return on capital, and pay down debt at the same time. The shares have sold off because of macro issues, like worries about a global slowdown, but Davidson views that as a transitory blip.

Nothing is permanent, of course, and Davidson worries that the dividend stock romp of recent years could soon be coming to an end, in large part because the category has become so popular. “It’s getting tougher to buy companies on terms that we like,” he laments. Still, if you’re disciplined and have a judicious eye, these dividend picks could stand you in good stead, even after the crowd departs.

This is part of Fortune’s 2017 Investor’s Guide, which features experts’ picks of 21 stocks and two funds to buy for next year.