The bromance at the heart of the Valeant disaster.

When, in April 2014, Bill Ackman and Michael Pearson came on stage together at the Equitable Center in midtown Manhattan to unveil their unorthodox bid to buy drug company Allergan, the two men couldn’t have appeared more different. Pearson, the CEO of Valeant Pharmaceuticals, was frumpy, overweight, and gruff. Hedge fund billionaire Ackman was, as always, impeccably groomed, trim, and silver-tongued. What brought them together was their joint love of big deals—and big profits. Ackman seemed in awe of Pearson’s dealmaking and his legendary thriftiness. In his remarks, Ackman pointed out admiringly that Pearson wouldn’t allow Valeant shareholders to be on the hook for half of what it had cost to rent the auditorium they were using to announce the deal. Ackman had to pick up the tab himself.

At least for a while the partnership worked. In Ackman, Pearson got a willing wingman on a controversial deal that other long-time Valeant (VRX) investors advised the drug executive against. Pershing Square Capital Management had bought up a near 10% stake, investing more than $3 billion, in Allergan (AGN) and pledged to vote those shares in favor of a Valeant deal. In return, Ackman collected billions for himself and his investors, putting him once again at the top of the hedge fund heap, and in the spotlight of glowing magazine profiles, in which he bragged about buying one of the most expensive apartments in New York City—a penthouse duplex with a commanding Central Park view in the new residential mega tower on 57th Street—even though he had no plans to ever live in it. (It was an investment with friends.)

Even after the bid for Allergan failed in November 2014, the relationship endured. In early 2015, Ackman doubled down on his partnership with Pearson, buying a huge stake in Valeant. That blunted criticism of Valeant that had emerged during and hung over the company after the failed Allergan deal. It also led other hedge funds to continue to load up on Valeant’s shares. Ackman became the drug company’s biggest cheerleader. He once famously compared Valeant to Berkshire Hathaway, even though the drug company had almost nothing in common with Warren Buffett’s massively successful conglomerate, other than the fact that both companies were active acquirers. Ackman’s outspoken public enthusiasm for the company helped drive Valeant’s market cap up another $23 billion after Ackman bought in.

The collaboration would eventually lead, as anyone who has heard of Valeant now knows, to a colossal, career-altering stock bust for both men. The relationship entered a new tension-filled stage, last week, with Ackman playing a central role in the ousting of Pearson from Valeant—the company Pearson built nearly from scratch over a decade based on his singular vision of the pharmaceutical industry as essentially a glorified marketing and distribution business.

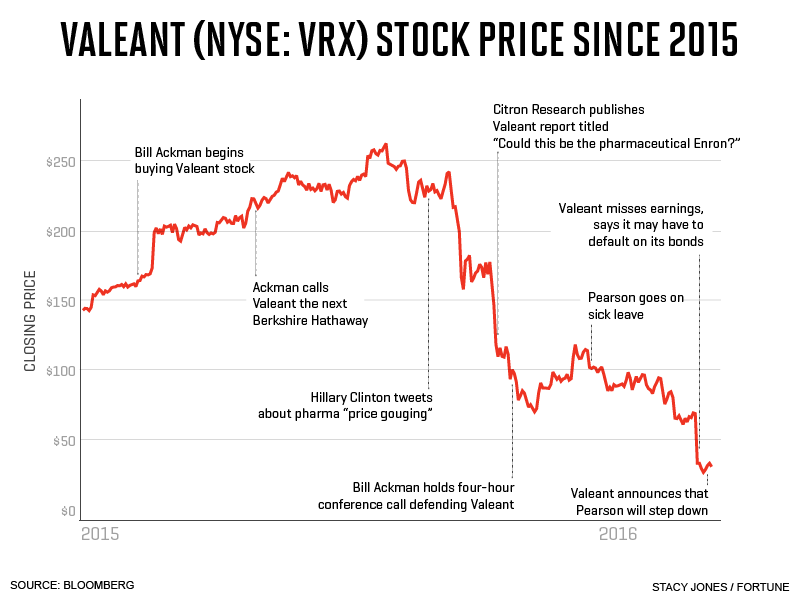

(For more on Valeant read: Valeant: A Timeline of the Pharma Scandal)

Both Pearson and Ackman made mistakes. In doing the deal, Pearson put his company’s controversial and largely unknown strategy of rapid-fire acquisitions along with its use of favorable accounting that inflated the profits Valeant reported to investors into the limelight. He also set up Ackman to make big bucks off the deal, inviting allegations of insider trading. Ackman, the activist investor well-known for ousting execs and putting in hand-picked replacements, for his part, accepted a hands-off role, even long after the Allergan deal and Valeant’s initial troubles, putting his faith in Pearson. Ackman allowed himself to be in the uncomfortable, and ultimately unwise, position of remaining mostly in the dark and out of control of what would become his fund’s largest investment.

Ackman’s role in the dismissal of Pearson last week was a stunning reversal. Throughout criticism of the company’s acquisitions strategy, the growing investigation into its drug pricing, and the recent blow up over Valeant’s accounting related to its bizarre relationship with a specialty pharmaceutical company, Ackman had remained the company’s and Pearson’s most vocal defender. In the past few weeks, though, Ackman’s confidence in Pearson seemed to be diminishing. In early March, Ackman speaking at an investment conference, said that if Valeant’s situation didn’t stabilize soon new management might be needed. Along the way Ackman’s Pershing Square bought up a huge amount of Valeant’s shares, even increased buying more as the questions surrounding the company grew, and eventually pushed his stake up to 9% of the company, making Ackman Valeant’s second largest holder, with the position at one point as large as $5 billion.

Many people have been stunned. “This has obviously been a very humbling experience for Bill, but that will make him a better investor over time, and I have no doubt that he will recover,” said Whitney Tilson, CEO of Kase Capital and a longtime friend of Ackman.

(For more on hedge fund manager Bill Ackman read: The Siege of Herbalife)

Behind the scenes, tensions had been brewing between the two men for some time, as Valeant’s fortunes took a drastic turn for the worse. It’s clear now that Ackman miscalculated badly. Valeant’s stock, which was as high as $263 a share last summer, has plunged nearly 90% to a recent $33. At least on paper Ackman has lost billions for himself and his investors, making it the worst-ever investment in Ackman’s long career. His leveraged publicly traded investment vehicle Pershing Square Holdings is now down 40% from last summer—making it one of the worst performing hedge funds over that stretch—largely as a result of the collapse of Valeant, though there have been other missteps as well. Fixing the pharma company, which is still facing multiple federal investigations and a huge debt load, will require a herculean effort. Ackman has joined Valeant’s board and has said he will take a more active role in helping to run the company.

Ackman has already achieved some success in his first big move toward restructuring the company. Turning out Pearson was no easy task. Even after the company’s recent troubles, Valeant’s board remained committed to Pearson. The board believed Pearson was Valeant. And Valeant’s board was stacked with long-time Pearson supporters, including two members from ValueAct Capital, a similarly powerful activist hedge fund that had essentially installed Pearson as the head of Valeant eight years before and helped fashion the company’s strategy. As recently as two weeks ago, ValueAct CEO Jeff Ubben defended Pearson on CNBC. Ackman had to work for months, most of the time from the outside, to plant the seed that, if things got hard enough, Pearson would have to go, before the board eventually sided with the hedge fund manager.

What’s more, taking an active role, at least for now, for Ackman, will mean working closely with Pearson, who the company has decided will stay on until Valeant can find a replacement. Ackman insists it won’t be a problem for him. “I’ve got a good relationship with Pearson and always have,” Ackman tells Fortune. The truth is Ackman needs Pearson to help unravel the mess, while Ackman searches for a new CEO to help salvage his investment. Pearson did not return a call for comment. A spokesperson for Valeant declined to comment on this story.

A Wall Street bromance begins

The hedge-fund mogul was introduced to Pearson in 2014 by a close friend from Ackman’s days at Harvard, Bill Doyle, who had become an adviser to Pershing Square. Doyle vouched for Pearson’s acumen and character, as he had known the man since both were at McKinsey years earlier, giving Ackman confidence in Doyle’s assessment. That now appears to have been misplaced. Unbeknownst to Ackman, though, Pearson also considered Doyle to be on his side in the relationship. Pearson liked the idea of having an insider at Pershing Square, he told a longtime friend. Doyle, Pearson told the longtime friend, was “loyal” to him. “He has my back,” Pearson said.

A story Ackman told on April 22, 2014, the day the partnership with Pearson was announced, is revealing. When Ackman and Pearson announced their bid for Allergan, the hedge fund manager told what he called a “little anecdote” that was meant to show Pearson’s “extreme culture of cost discipline”—which investors naturally think is a good thing. Ackman was at Valeant’s New Jersey office, working on the presentation, and didn’t like the chicken and salad lunch that was on offer. “They had a Chipotle around the corner and I actually asked if I could get a Chipotle burrito and Mike’s assistant very nicely got me one,” Ackman said. “And then Mike walked into the conference room and asked me for twenty bucks.”

But while Ackman went out of his way publicly to make Pearson look good, Pearson rarely returned the favor. In January of 2015, after the Allergan deal collapsed, Pearson told Canada’s Financial Post that it wasn’t likely Valeant would do another deal with Ackman. “We have nothing in the works. You can never say never, but if I was ever going to say never, it would probably be on something like this,” he said. That same day Pearson told the Financial Times that Ackman was a “very good partner who kept his word.” But when asked about the status of their relationship, Pearson said bluntly, “It’s over.”

Undaunted by the public brushoff, Ackman took a 5% stake in Valeant in March of 2015. What’s more, in a further sign of confidence in Pearson, Ackman said in his 13D securities filing that he didn’t plan on taking his normal role of agitating for change in the C-suite, because there was already a shareholder activist on the board, and Pearson had a great track record. Ackman thought he would work with Pearson to help Valeant continue its string of acquisitions. But it turned out Ackman and Pearson weren’t on the same page.

For instance, Ackman hoped Valeant would acquire Zoetis (ZTS), the pet treatment company in which Ackman had a large investment and where Doyle was a board member. Valeant did hold talks with Zoetis, but walked away from a deal.

Other times Ackman found himself caught off guard. Ackman told Fortune he had not known Valeant had significantly hiked the price of two heart drugs until he read it in the Wall Street Journal in the spring of 2015. The article created a lot of controversy. Ackman quickly called Pearson, who explained that the drugs were sold to hospitals to be used in heart operations that cost tens of thousands of dollars and Valeant’s drugs represented a very small percentage of the actual cost to the patient. Ackman accepted Pearson’s rationale. When, on Oct. 21, Citron Research, run by short seller Andrew Left, released a report saying the drug company was using a specialty pharmacy division Philidor to perpetrate an Enron-like accounting fraud, Ackman says he called Pearson immediately. The Valeant CEO assured Ackman there was no fraud at the company. Ackman says he knew about Philidor, but not how much the controversial special pharmacy was contributing to Valeant’s bottom line.

By that time, Pearson was growing nervous that Ackman would push for his ouster. Five days later, on a conference call with investors to announce that the company was launching an investigation into Philidor, Valeant announced that Mason Morfit, the ValueAct partner who had originally helped recruit Pearson, was rejoining the board. At the time, the company said Morfit was returning to help with the investigation. But according to someone familiar with Pearson’s actions, the CEO wanted Morfit on the board to help Pearson “block” Ackman from turning the board against him. Ackman was unaware of Pearson’s fears and applauded the Morfit appointment. After all, he had been on the board since 2007, except for a brief hiatus.

The next morning Ackman shot off an email to the board warning that the situation could become a “death spiral” if more action wasn’t taken. Later that afternoon, Ackman called into a hastily convened board meeting, telling the board Valeant needed to have another call with investors laying out exactly what the company currently knew, instead of waiting for the full investigation to come back. But Ackman didn’t have a board seat, nor the power to sway the group. The board decided against forcing Pearson to hold any other call with investors. Ackman followed that decision with an email to Robert Ingram, Valeant’s lead director, questioning whether Pearson was the right person for the job.

Three days later, on the morning of October 30, Valeant announced it was shutting down Philidor. But the timing was awkward for Ackman. That same morning Ackman had scheduled a conference call with investors to explain the situation at Valeant, and why he was sticking with the company. But things were moving rapidly, and it was clear from the presentation slides he used during the call, which were prepared the night before, that Ackman had no idea Valeant was going to close Philidor, making Ackman look out of touch. During the rambling four-hour call, in which Ackman took each and every question, he even mentioned the possibility of Valeant putting itself up for sale. Shortly after, Valeant’s shares seemed to stabilize.

Now Ackman says there are no plans to sell Valeant.

The end of the affair

When the Wall Street Journal revealed the existence of Ackman’s email to Ingram, questioning Pearson, Valeant’s stock tanked anew. Ackman tried to downplay the story in a widely publicized email on Nov. 5. “You are one of the most shareholder-oriented CEOs I know,” he wrote Pearson, saying he was sure Pearson would do whatever was necessary to maximize shareholder value.

On December 15, Valeant announced a deal with Walgreen’s to replace the controversial specialty pharmacy as a sales channel for Valeant’s drugs, and Ackman thought it would right the ship. The stock soared on the news. But Pearson fell ill, and Ackman was even more in the dark. Because he was selling stock at yearend for tax purposes, he says he didn’t even call the company.

[fortune-brightcove videoid=4802294288001]

On Feb. 23, the company gave an interim report, saying that it would likely be forced to redo $58 million in revenue inappropriately booked with Philidor in 2014, before it was consolidated into Valeant’s books, which would delay its financial reporting. Ackman says he wasn’t concerned. He still considers the Philidor-related restatement a minor irregularity given the size of the company.

Six days later, Pearson returned from sick leave. The board had decided he should resume his role as CEO, taking over from interim CEO Howard Schiller. Ackman met with Pearson and said he would endorse the appointment, but quickly moved to put Pershing Square vice chairman Stephen Fraidan on the board, giving the hedge fund Valeant board representation for the first time.

One of Ackman’s biggest concerns was the board’s seeming unwillingness to act more quickly to cure Valeant’s problems. On March 15, the company reported earnings that missed analysts’ expectations. Worse, the company said its loan covenants required it to file its delayed financial statements by the end of April. Valeant said it could not guarantee it would meet that deadline, which raised the possibility that the company could default on its bonds, or even be forced into bankruptcy. According to a person close to members of the board, the problem was that the board was “freaked out” about its potential liability if it signed off on its internal investigation into the alleged improprieties surrounding Philidor. And the board had to sign off on the internal investigation before Valeant could get audited financial statements.

The announcement of a possible default was a disaster. The stock collapsed, falling 50% and wiping out $12 billion of market value in one day. For Ackman, it was the final straw. Letting the company slide into bankruptcy was dangerous for a shareholder like Ackman. On March 16, he vowed publicly to “take a more proactive role,” and said “We know how to fix this.”

Since that day, two members of Pershing Square’s investment team have been embedded at Valeant headquarters, Ackman revealed in Pershing Square Holding’s annual report, which was released Thursday. They’ve been given full access to the company’s financial information. Ackman also attended Valeant board meetings “as an observer” late last week, and through the weekend of March 19-20. Although he only officially joined on Monday, Pershing’s annual report, said the “new board worked collaboratively over the weekend to understand the conclusions to date of the Ad Hoc Committee’s investigation of Valeant’s accounting and to discuss CEO Mike Pearson’s continued candidacy as CEO.” The Wall Street Journal reported that Ackman played a “central” role in those discussions, and by Monday morning the company announced that Pearson would be leaving. The company also agreed to admit errors and committed to getting the audited financials done in time to avoid a default.

Ackman still thinks Valeant’s core businesses are worth multiples of the current stock price, which has climbed nearly 20% off its lows since he joined the board. “I look forward to working with the board to identify new leadership for Valeant,” he said.