Beijing and Washington are both closing the doors on Chinese companies’ U.S. listings, a move that is likely to shift those firms’ initial public offerings from American exchanges to Hong Kong.

Two weeks ago, Chinese ride-hailing giant Didi Chuxing debuted in New York and raised $4.4 billion. But Didi’s listing is likely the “last major IPO by a Chinese firm in the U.S.,” says Paul Krake, founder of View from the Peak, an investment research firm. Moving forward, Hong Kong will be the “premier exchange” for Chinese firms in search of foreign capital, he says.

After Didi’s blockbuster IPO, Beijing expanded its regulatory remit over Chinese Internet firms. The Cyberspace Administration of China (CAC) announced a cybersecurity investigation into Didi and two other recently U.S.-listed companies, citing data and national security concerns.

Then, the CAC released a sweeping directive to tighten the rules for overseas listings, particularly related to cross-border data flow. On July 10, the CAC dropped another hammer: all companies with over 1 million users must undergo a cybersecurity review before listing overseas, meaning Beijing will now effectively sign off on any company raising capital on foreign exchanges.

China’s tightening grip, alongside tougher rules from Washington, will not only cool Chinese listings in the U.S. IPO pipeline, but force companies to “rethink strategy and instead focus on listing in Hong Kong,” says Ramiz Chelat, portfolio manager at investment firm Vontobel. “This is all part of China’s ‘homecoming’ strategy.’”

China isn’t being subtle about its preference for Chinese companies to go public in Hong Kong. According to a Friday report from Bloomberg, Beijing will exempt companies that list in Hong Kong from the cybersecurity review it introduced earlier this month.

The question now is if Hong Kong can handle what may be a tsunami of new listings headed its way.

Hong Kong homecoming

Even before Beijing introduced its new rules, ‘homecoming listings’—a secondary listing in Hong Kong for Chinese firms that trade in the U.S.—were gaining popularity as a hedge against the U.S. delisting such firms as U.S.-China tensions soured and as American regulators imposed new disclosure laws.

Jack Ma’s Alibaba Group was the first Chinese company to complete a secondary debut in Hong Kong in November 2019, raking in $12.9 billion in IPO proceeds. In 2020, nine Chinese firms completed secondary listings on the Hong Kong Exchange or HKEX, and this year, the bourse has hosted five such listings so far, according to Refinitiv data. China’s other tech giants took part in the rush, with search engine Baidu, video platform Bilibili and Alibaba competitor JD.com all completing homecoming listings in the last two years.

On June 25, China Tourism Group Duty Free, a state-owned duty-free business, filed for a secondary listing in Hong Kong. Targeting a $7 billion raise, the firm’s secondary debut could be the largest in the city this year.

Since 2019, Chinese firms’ secondary and dual listings via the HKEX have raised approximately $44 billion.

“The homecoming listings…continue to lift the city’s capital markets and [are] the hot trend. We expect [it] to continue,” says Louis Lau, a partner in KPMG China’s capital markets advisory group.

U.S. action is also forcing Chinese firms to think twice about listing on American exchanges.

Last year, the U.S. Congress passed a bill that empowers the Securities and Exchange Commission (SEC) to delist U.S.-listed Chinese companies if the companies have not been audited by U.S. regulators for three straight years.

While the SEC hasn’t yet finalized its delisting timeline, the push for a “complete ban” on Chinese listings is gaining momentum in Washington, says Krake. The “toxic political climate between Beijing and Washington means that in the near-term, there is very little chance the [delisting] issue will be resolved,” says Paul Triolo, head of geotechnology at political risk consultancy Eurasia Group.

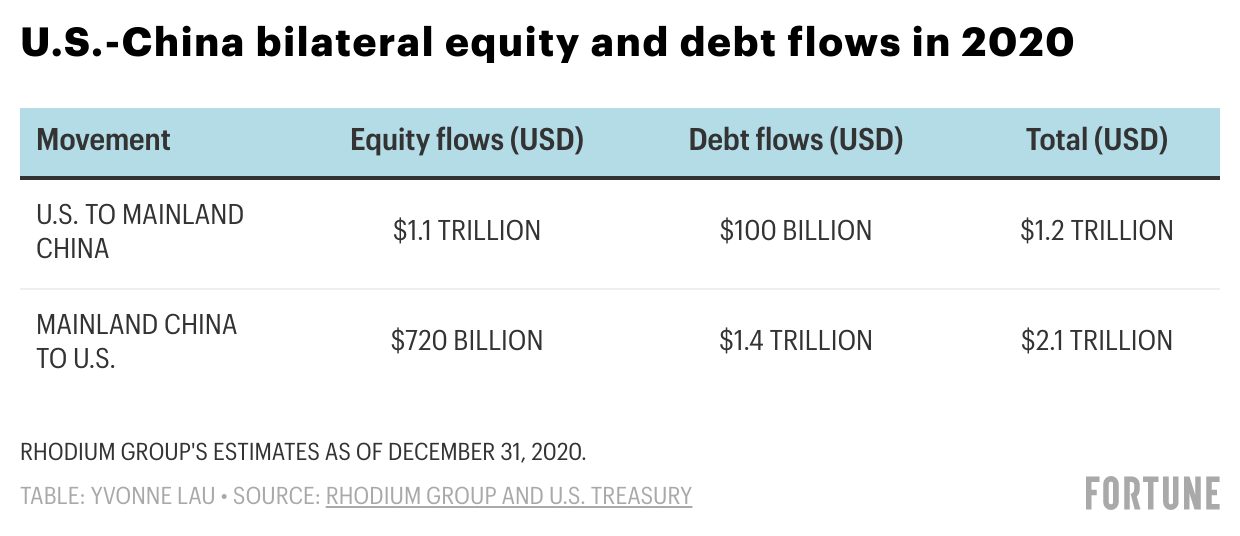

As of May 2021, 248 Chinese companies traded on U.S. exchanges, with a total market capitalization of $2.1 trillion, according to the U.S.-China Economic and Security Review Commission. Chinese firms have issued $19 billion in stock to American investors as of December 2020.

Lorraine Tan, director of equity research in Asia at Morningstar, predicts the remaining companies will “start to flow back into Hong Kong for sure.” That trend, of Chinese companies delisting from the U.S. and relisting in Hong Kong, in addition to brand new debuts and secondary listings in Hong Kong, could inundate the city’s bourse with a flood of offerings.

The obvious choice

Hong Kong is the obvious venue for Chinese firms going forward because of its capital market maturity and proximity to mainland China.

Mainland Chinese exchanges are another option, but they are generally viewed as lower-tier venues, lacking the prestige and liquidity of U.S. and Hong Kong exchanges. It’s more difficult for foreign investors to trade on Chinese exchanges, given China’s stricter capital market controls. Chinese A-shares, the stocks of Chinese firms that trade on mainland exchanges, for instance, are only available to foreign investors via certain programs such as China’s Qualified Foreign Institutional Investor (QFII).

While China launched its own Nasdaq-like STAR Market in 2019 to let tech firms list more easily, market regulators have since tightened requirements for STAR listings, prolonging the approval process and banning fintech firms from the bourse.

If the U.S. is off-limits, firms see Hong Kong as the next best thing.

In 2020, the HKEX generated $51.3 billion in IPO proceeds, trailing only the Nasdaq and New York Stock Exchange. It allows for much greater foreign investor participation than mainland bourses.

The HKEX has averaged 171 new listings per year over the last five years and now hosts 2,550 listed companies. Adding all or even a portion of the Chinese firms currently listed in the U.S.—plus listings already in the pipeline—could reshape the Hong Kong bourse considerably, but Stephanie Tang, head of private equity, greater China at law firm Hogan Lovells, doesn’t expect the relistings to happen all at once.

“In reality, it’s not going to happen over a short period of time. I’d be very surprised if companies delisted [from the U.S.] in, say, the same six-month time span,” she says.

Still, a new influx of IPO applications doesn’t mean Hong Kong will “roll out a red carpet treatment” for all companies, says Lyndon Chao, managing director of equities at the Asia Securities Industry & Financial Markets Association. The exchange is selective in its IPOs; in fact, Didi reportedly dropped plans to list in Hong Kong and opted for New York instead because the company was concerned it would run into stricter scrutiny over its business practices, like the use of part-time drivers and unlicensed cars.

Another issue is Variable Interest Entities (VIE). The structure is essentially a loophole that allows Chinese tech firms in sensitive industries, like the Internet, to raise foreign capital. Beijing may soon require all firms that use VIEs to seek its approval prior to going public overseas. The Hong Kong bourse currently allows companies that use VIEs to list. How Beijing’s new rules may change VIE listings in Hong Kong remains to be seen, Tang says.

The HKEX is the process of making its listing rules even tighter. It will raise the profit requirements for listing companies by 60%, to roughly $10 million in 2022—the first increase since 1994. The new threshold may be too high for some of the smaller firms among the 248 U.S.-listed Chinese companies, Wu says.

Still, it appears the bourse is preparing for a new rush of listings. By the end of 2022, it will implement FINI—the ‘Fast Interface for New Issuance’—a new digital platform set to cut the IPO process from two days from five.

An HKEX spokesperson said the exchange is “well-placed to welcome new listings.”

“We have a deep liquid market, a highly-respected regulatory framework and the right resources and technologies to support our continued development as a premier IPO venue.”

A senior executive at a Chinese securities firm, who asked for anonymity because he was not authorized to speak, says Hong Kong’s tougher listing requirements may disqualify some smaller Chinese companies from listing, but large-cap companies should have no problem—and they’re the ones that matter, he says.