Was the United Kingdom’s decision to leave the European Union a success? Were the warnings of swift and terrible vengeance from the implacable gods of economics all wrong? These are reasonable questions for reasonable people to be asking after a few encouraging reports on the U.K. economy.

This week, the U.K. has been processing the first hard economic data since the June 23rd referendum. The 11% trade-weighted drop in sterling has had an immediate impact on manufacturers, whose input prices rose 3.3% from June. However, they largely absorbed that shock themselves, as factory gate prices—or the wholesale prices of goods paid by retailers and distributors—rose only 0.3% on the month. That price shock will almost certainly feed its way through the price chain to the consumer within a couple of months. Inflation will tick up.

At this point, Brexit supporters argue that inflation picking up is a good thing—assuming it stops the Bank of England from following the European Central Bank and Bank of Japan down a path of negative interest rates, which is arguably doing those economies more harm than good. But for the moment, let’s concentrate on the fact that real prices will be going up, leaving ordinary people worse off, if only by a little for now.

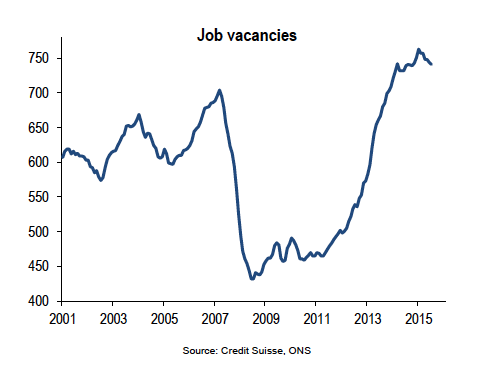

The Office for National Statistics’ (ONS) second pitch this week was its Labor Force Survey, which showed that the number of people claiming jobless benefit fell by 8,600 in July, compared to expectations of an immediate knee-jerk increase in response to the Brexit vote. But as analysts from Credit Suisse point out, the only other part of the report to include data for July was job openings, which fell by 3,000 to 741,000. Unemployment is a lagging indicator, vacancies a leading one, so it is clear that, as far as the jobs market goes, the worst is still to come.

But how bad will that ‘worst’ be?

Yes, Credit Suisse is right in saying that vacancies fell to their lowest in 10 months, but the chart above also shows that they are still running at a higher level than at the height of the pre-crisis boom. The U.K. economy went into the Brexit vote with significant momentum.

The third hard datapoint of the week came Thursday morning, with a surge in retail sales in July. Sales rose 1.4% on the month, compared to expectations for a 0.2% improvement. That more than wiped out the 0.9% drop in June, and left sales up 5.9% on the year (or 5.4% when the more volatile seasonal elements are stripped out).

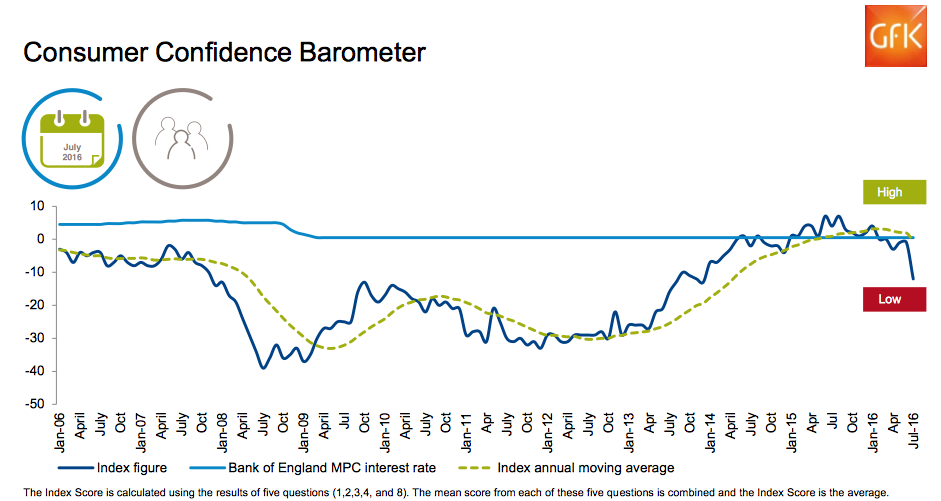

The interesting thing here is not so much the actual swing—retail sales are notoriously volatile in the short term—but how much the reality differed from the sentiment indicators that preceded it. The GfK consumer confidence barometer had had its biggest drop in over 26 years in July. Reality bore no resemblance.

But at the risk of sounding too much like a “that’s-alright-in-practice-but-how-does-it-work-in-theory?” economist, there is a risk of over-interpreting reality here. The ONS noted that good weather had boosted clothing sales, while anecdotal evidence suggests that tourists had taken advantage of the drop in sterling to enjoy themselves a little more while on vacation. Neither the English weather nor one of those fleeting periods when London is just “outrageously expensive” as opposed to “insanely expensive” is a solid basis for long-term prosperity.

The risk that consumers’ actual behavior catches up with the sentiment indicators as their incomes are squeezed is clear, as is the transmission mechanism: consumption in the U.K. is closely correlated to house prices, and those fell 1.2% in the month after Brexit. The chance of business investment—which is in the hands of a far smaller number of people who are generally much more fearful about the risks of Brexit—following the sentiment indicators down seems just as real.

But the government and the Bank of England (BOE) have both taken steps to cushion the shock: the BOE has cut interest rates and added to its quantitative easing program. Even if monetary policy is losing traction after years of ultra-low interest rates, the BOE has looked pro-active and engaged, without looking panicky.

At the same time, the new government under Theresa May has all but abandoned its plan for balancing the budget, heading off fears that an ideologically driven austerity would compound the effects of Brexit.

What May’s government hasn’t done yet, however, is to send a clear signal on its own willingness to sustain investment through the coming weak patch. Its signals have been decidedly mixed: May slammed the brakes on the massively expensive new, part-Chinese owned Hinkley Point nuclear power station, potentially jeopardizing other inward Chinese investment. But this week she waved through the world’s biggest offshore wind farm project, and retreated from her predecessor’s plans to assail the food and drink industry in the cause of tackling obesity.

As the Confederation of British Industry wrote Thursday, some crucial weeks lie ahead. What business most wants is a clear timetable for leaving the EU, and as clear an idea as possible on what the negotiating strategy will be—will the U.K. be willing to pay to stay in the Single Market or not?

That question may take months to answer. In the meantime, May has a chance to send a strong signal about investment by taking a final decision on where and how to build extra runway capacity at London’s airports this fall, something that could be wrapped into an investment heavy “Autumn Statement”, where the government traditionally lays out its spending plans for the year ahead.

For all the data and surveys out so far, it is still wait-and-see mode until there is more clarity on the policy front.