SABMiller took the fight back to AB Inbev Friday, promising to find another $500 million a year in cost savings in an effort to persuade shareholders that they can do a better job of delivering value.

That’s a tough ask right now, given that ABI’s offer was around 44% above where SABMiller’s stock had been trading before news of its intention to bid leaked out. ABI, the world’s biggest brewer and the company behind Budweiser and Stella Artois, had gone public on Wednesday with a third offer valuing the company at up to $104 billion, after having two earlier bids rejected by SABMiller’s management.

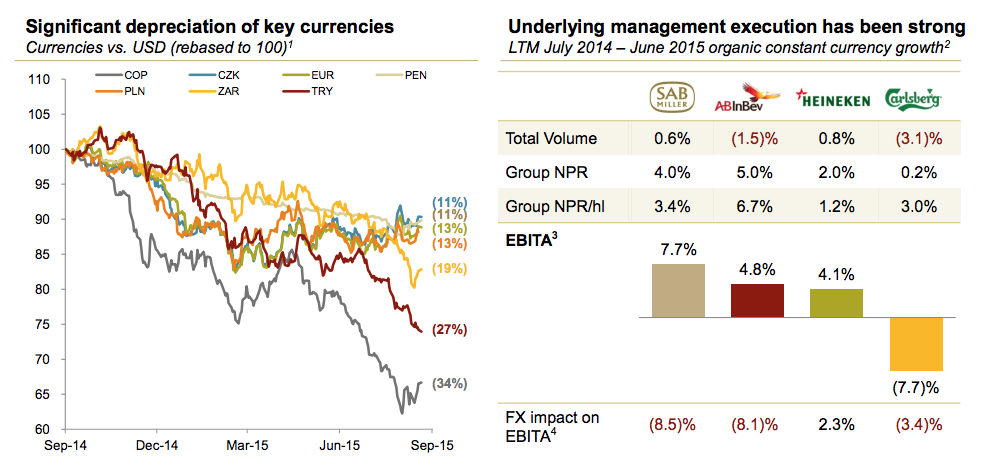

SABMiller argues that even the latest offer, at 42.15 pounds a share, “substantially undervalues” the world’s number two beer company, and that ABI is just being opportunistic by making a move at a time when emerging market-themed assets are cheap. SABMiller gets over half of its operating profit from Africa, Latin America and other developing economies, most of which have fallen sharply out of favor with investors this year: growth rates have slowed and currencies such as the South African rand, Turkish lira and Colombian peso have crumbled, depressing the dollar value of the profits the company makes there. With the U.S. about to start raising interest rates, a cycle that will keep the dollar supported against other currencies over more than just the short term, it’s not clear that the old assumptions about SABMiller’s outlook can hold.

In a letter to shareholders Friday, SABMiller’s management did its best to knock back ABI’s claim that its defense “lacks credibility”. It said it could strip over $1 billion a year out of its cost base by 2020. Last year, it had targeted $550 million in savings by 2018, so the new target is a lot more ambitious (even if the management is giving itself two more years to meet it).

Trevor Stirling, an analyst with Sanford C. Bernstein in London, argues that the new cuts announced today are credible enough, given the extra efficiencies it can squeeze out of its supply chain by rolling out the use of SAP enterprise software across the group. The new target implies that it ‘only’ has to find an extra $250 million a year in 2019 and 2020, compared to the $430 million it expects to wring out of the cost base in its fiscal 2016 year. (SABMiller, like AB InBev, is the creation of many past acquisitions, meaning that its internal machinery is a Frankenstein-like patchwork of systems and contractual arrangements begging for optimization.) SABMiller reckons it will get 70% of the proposed savings from procurement, and the remaining 30% from manufacturing and distribution. It all adds up to a 10% cut in major operating costs over 6 years.

All well and good, you might think. But the uncomfortable truth for SABMiller’s management is that its argument about the effect of temporary emerging market weakness only goes so far. The 42.15 pounds offered by ABI is more than 12% above the all-time high for SABMiller’s stock. And despite the very real achievements of the management in recent years, that all-time high was driven, as much as anything, by hopes for the kind of merger that ABI is now proposing: a deal that would create, in ABI’s phrase, “the first truly global beer company.”

If the headwinds from the currency markets abate (and the Colombian peso, for one, has already reclaimed half of what it lost against the dollar during the summer rout of EMFX), then SABMiller might still persuade its investors to stay loyal. But if the new U.S. interest rate cycle and the slowdown in China end up hurting SABMiller’s core growth markets in Africa more than ABI’s in Latin America and Asia, then it still has a mountain to climb.