It was a busy and fruitful year for enterprise-software companies: Zendesk (ZEN), HortonWorks (HDP) and New Relic (NEWR) went public, while privately-held heavyweights like Box, Nutanix, Atlassian, Palantir, AppDynamics* and Cloudera pushed beyond $1 billion valuations. As we look forward to 2015, it’s clear we’ll see more enterprise action in the public and private arenas (and more cyber-terrorism, but more on that later).

Despite some froth in the market—and my feeling that some private enterprise-software valuations will soften next year–I’m still very bullish on this sector. We’re still in the early innings of a major shift in the way companies manage their IT operations and deliver core business software to customers. Here are four more in-depth predictions about how enterprise software may evolve in 2015.

1. “Customer success” will become a C-level position in many companies.

It’s been a decade since software-as-a-service (SaaS) caught on in a big way. But now that everyone’s convinced SaaS is the best way to sell and deploy enterprise software, we’re entering a new phase: Moving away from simply doing whatever it takes to acquire new customers to figuring out ways to keep them and optimize their success. In a subscription model, after all, the real money lies in keeping your customers happy over the long haul. The freemium model only works at the beginning of a new-customer relationship.

So I think 2015 will be the year companies hire C-level “customer success” executives—Chief Customer Officers, or CCOs, tasked with reducing customer churn to zero. Many large companies already have VPs of customer success, but I think up-leveling this critical function is inevitable as SaaS companies increasingly require comprehensive, data-driven programs to keep customers buying renewing expensive products and services.

2. It will be harder to break into–and stay in–the “billion-dollar club.”

Unicorn alert! At the end of 2014, there were at least 48 private U.S. companies valued at $1 billion or more by VC firms, versus 27 at the start of the year. This number includes all private companies, not just enterprise tech firms, but it’s still a telling figure since there were only ten such companies during the height of the dotcom boom in 2000.

In 2015, I predict entry into that exclusive club is going to get more difficult, as choppy public markets set the tone for less-bubbly, private-company valuations. Late this year, HortonWorks and New Relic priced IPOs below the valuations of their last private financings, putting recent investors underwater. Both companies ultimately had their market caps rise above $1 billion. But their initial decisions to price shares lower cannot be ignored. Now, other mature enterprise companies could see a softening in their valuations as late-stage investors proceed cautiously to avoid down-rounds when their portfolio companies go public.

3. Box will have a successful IPO and Wall Street will finally “get” its business model.

Despite Box’s on-hold IPO and lowered expectations for pricing, the company is still a huge success and has an extremely compelling business model. I predict Box not only will stage a successful IPO in 2015, but finally prove to investors that its “compounding renewal” model will create significant and durable equity value.

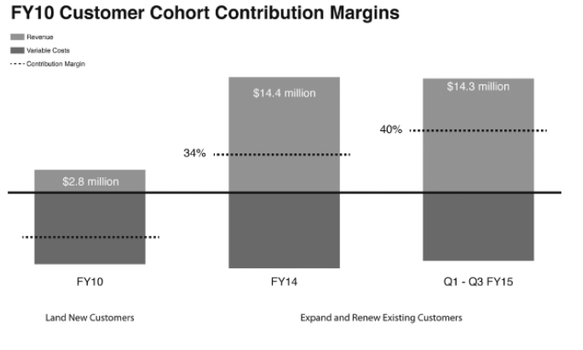

Here’s how it works: If the company signs up a group of customers paying $1,000 for Box for a year, that same cohort will pay $1,300 the next year, and $1,690 the year after that. That’s a 130% customer-renewal rate. Why? Simply put, as customers use Box, and as they grow, they store more and more files with the service, requiring them to upgrade to pricier service packages with more storage. It’s a nifty lock-in arrangement. Box’s S-1 document shows a renewal rate of 144% in fiscal 2013 and 136% in fiscal 2014.

In parallel with the compounding revenue growth is an equally important decrease in costs to support those customers over time. The below chart from the S-1 shows how decreasing customer-maintenance costs over time yield attractive operating margins for Box as customer cohorts mature.

Sure, Box is spending tons on sales and marketing, which is what has been worrying Wall Street. However, given the 30% compounding nature of the company’s revenue–coupled with declining operating costs–this spending makes sense.

4. Cyber-security takes center stage.

The recent attack on Sony has every corporate Chief Information Security Officer (CISO) on the planet scared to death. We now have nation states such as North Korea attacking private companies and releasing confidential information for political purposes. More importantly, these attacks are working. The effect in the VC and tech world? Expect even more high-profile investments in cyber-security companies, based both here and overseas, trying to fight online attacks in new ways.

Roger Lee (@rogerleevc) is a general partner with Battery Ventures in Menlo Park, Calif. His investments include Angie’s List, Blue Jeans Network, Gainsight, Groupon, Kontagent, Lotame, Narrative Science, PrimeRevenue, TrialPay, Veradocs and World Golf Tour.

* Denotes a Battery Ventures portfolio company.